A few years ago, a partner at a well-known accelerator walked me through their evaluation rubric. There was a section for market size, one for team composition, one for what they called “founder-market fit.” It was thorough. It was also, I realized as he talked, a nearly perfect description of every company they had already funded that worked out. They weren’t predicting the future. They were describing the past and calling it a model.

This is the central problem with how accelerators use pattern recognition to pick winners: the patterns are real, but the conclusions drawn from them are systematically overconfident. Accelerators have convinced themselves, and convinced a lot of founders, that they possess a kind of predictive science. They don’t. What they have is a sorting mechanism that occasionally produces the right outcome for the wrong reasons.

The Patterns Are Real But They Prove Less Than Anyone Admits

Y Combinator has funded companies that went on to become publicly traded, and there are genuine commonalities across that cohort. Founders who had worked deeply inside the problem they were solving. Products with early retention that looked strange, almost fanatical. Revenue that was small but growing in ways that compounded. These are real signals.

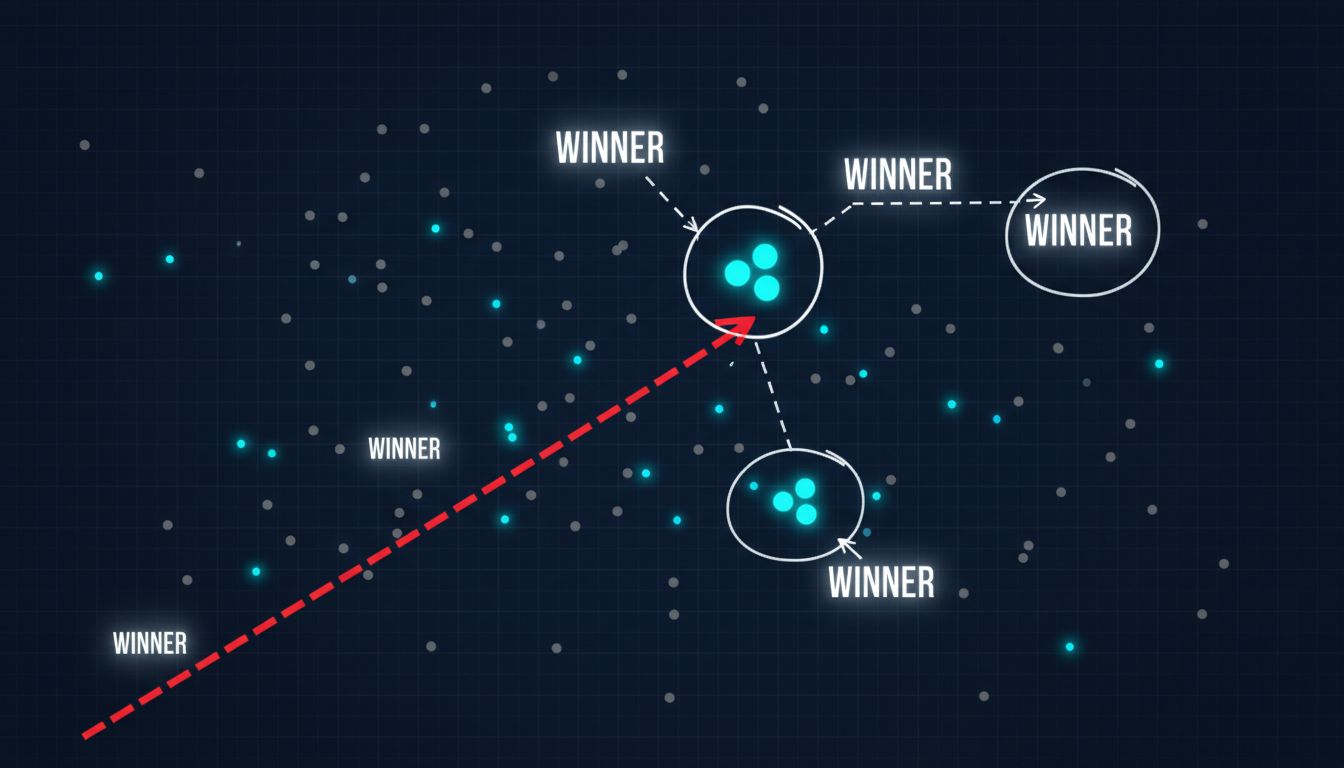

But here’s what gets glossed over: the same patterns appear in hundreds of companies that never made it anywhere near an IPO. The pattern recognition tools accelerators have developed are good at filtering out obvious failures. They are mediocre at identifying future successes. The true positive rate sounds impressive until you account for how many things matched the pattern and still died quietly in a Series B somewhere.

The signal-to-noise problem is severe because the sample sizes are small and the feedback loops are long. A fund that backs companies today won’t know if its pattern recognition was any good for seven to ten years. By then, partners have moved, market conditions have shifted, and everyone has retrofitted a tidy narrative onto whatever happened.

Accelerators Optimize for the Pattern, Not the Company

Once you accept that accelerators are running a pattern-matching operation, the incentive structure becomes clear. Founders learn what the pattern looks like and shape their pitches accordingly. The result is a generation of founders who are very good at resembling the type of company that gets funded, which is not the same thing as building a company that will eventually go public.

This is a selection effect with real costs. The founders who don’t fit the pattern cleanly, who are building something genuinely strange or attacking a market that looks small before it explodes, often don’t make it through the filter. Smart founders collect rejection letters the way scientists collect data because they understand that the rejection is information about the filter, not necessarily about the company.

The accelerators most confident in their models are often the ones most blind to this. They see a high hit rate among their portfolio companies and interpret that as validation of their pattern recognition. But they’re not accounting for what they systematically refused to fund.

The IPO Prediction Claim Is Particularly Shaky

Predicting which companies will IPO is a substantially harder problem than predicting which companies will grow. An IPO is a liquidity event shaped by market conditions, investor appetite, regulatory timing, and decisions made by boards and bankers years after the company was founded. The fundamentals of the business are one input among many.

When accelerators claim their frameworks help identify future IPO candidates, they’re often conflating “built a large and durable business” with “achieved a specific exit outcome.” Many large, durable businesses never go public and never intended to. Many companies that did go public probably shouldn’t have, at least not when they did. The IPO is a downstream outcome that pattern recognition at the seed stage has very limited ability to predict.

The accelerators making this claim loudest tend to point to a handful of marquee exits and work backward. That’s not analysis. It’s a highlight reel.

The Counterargument

The honest version of the counterargument goes like this: even imperfect pattern recognition is better than nothing. Investing is probabilistic, not deterministic. If a framework improves the hit rate from two percent to six percent, it’s worth using, even if it’s wrong most of the time. The accelerators aren’t claiming to predict individual outcomes with certainty. They’re trying to tilt the odds.

That’s fair, and I don’t dismiss it. The problem isn’t that accelerators use pattern recognition. It’s that they’ve started believing their own marketing about how good it is. When the framework gets packaged into blog posts and sold to founders as a rubric for building IPO-worthy companies, the imprecision gets stripped away and what’s left is a kind of false certainty that does real damage.

The framework is a tool. It’s being sold as a telescope.

What Actually Predicts IPO Outcomes

The companies that go public tend to share a few things that are genuinely hard to pattern-match at the seed stage: they found a way to grow that got cheaper over time, not more expensive; they built something competitors found too structurally weird to copy; and they had leadership that could survive the transition from scrappy builder to institutional company without losing the thing that made them grow in the first place.

None of those things are easily visible at demo day. Most of them aren’t visible until years later. Accelerators who are honest about this run better programs. They stop pretending they’re running a prediction engine and start admitting they’re running a development environment, one that improves the odds without controlling the outcome.

That’s a more defensible position. It also happens to be true.