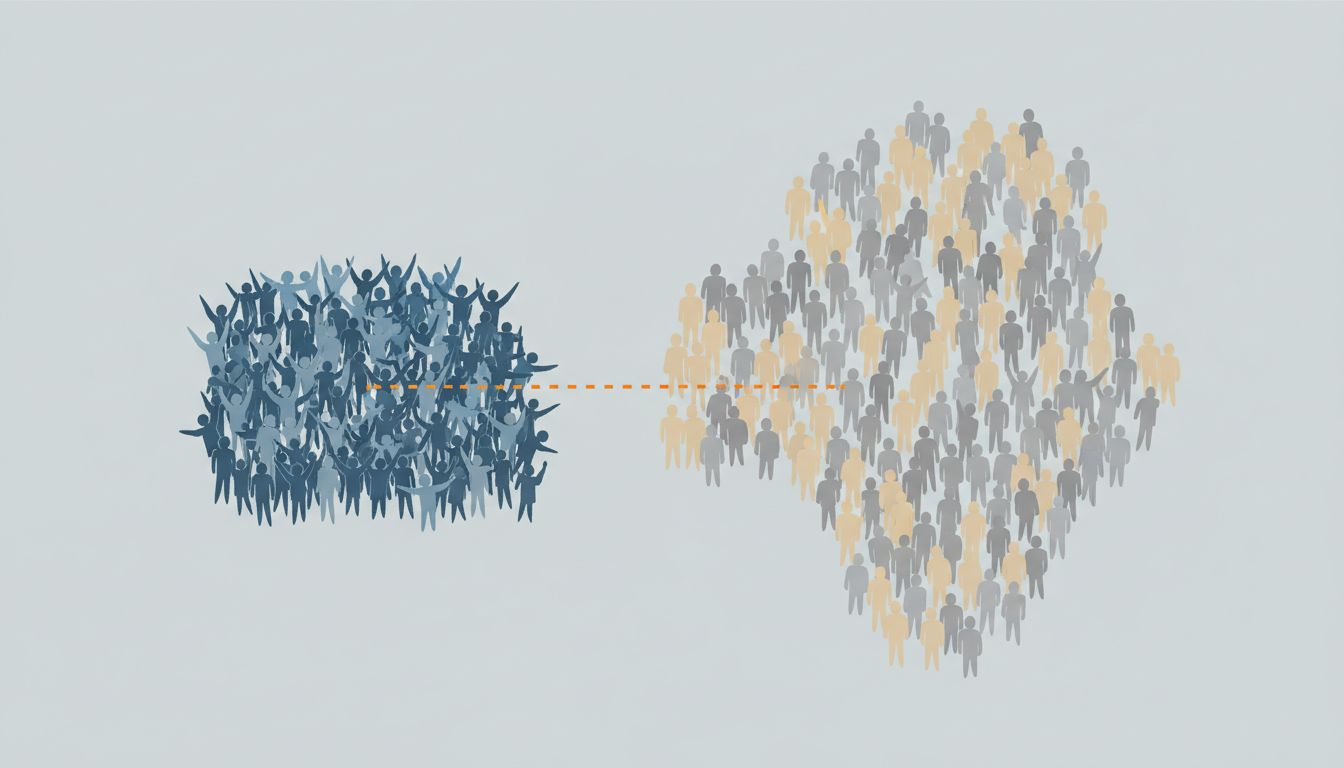

A founder I know spent his first year closing 200 customers at $50 a month. He had growth charts that looked great in pitch decks. His co-founder at a competing company spent the same year closing 8 customers at $4,000 a month. Three years later, the first founder was grinding through churn, support tickets, and a product roadmap that tried to serve everyone. The second company had raised a Series B and was expanding upmarket. Same category, same starting year, very different trajectories.

This isn’t a story about price points. It’s about what happens to a company’s learning, product, and culture when you optimize for volume before you understand value.

The Signal-to-Noise Problem With Too Many Early Customers

When you have 200 customers in year one, you have 200 opinions about what the product should do. Some of them conflict. Some of them are wrong. All of them feel urgent because each one represents a small slice of the revenue you desperately need. You end up building features that satisfy a vocal minority, patching edge cases, and writing support documentation for workflows your best customers would never use.

With eight customers, you can actually talk to all of them. You know their names. You know which problems are shared and which are idiosyncratic. You build the thing that matters and ignore everything else. That selective pressure on the product is worth more than any market research report.

The irony is that founders often race to accumulate customers as proof that the product works. But early customer count is a weak signal at best, and a misleading one at worst. A product with 200 customers at $50 might be marginally useful to a large, diffuse population. A product with 8 customers at $4,000 has proven it solves something painful enough to write a real check for.

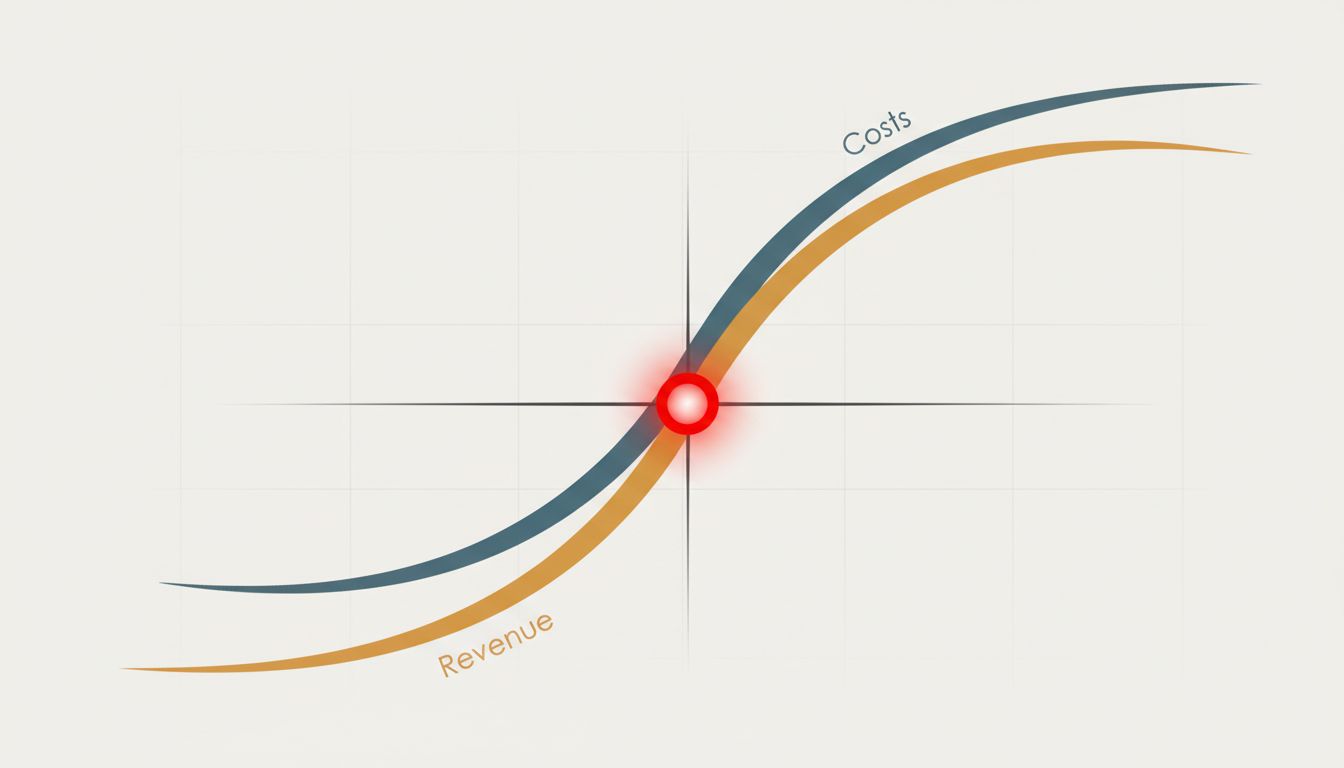

Churn Kills Compound Growth Before It Starts

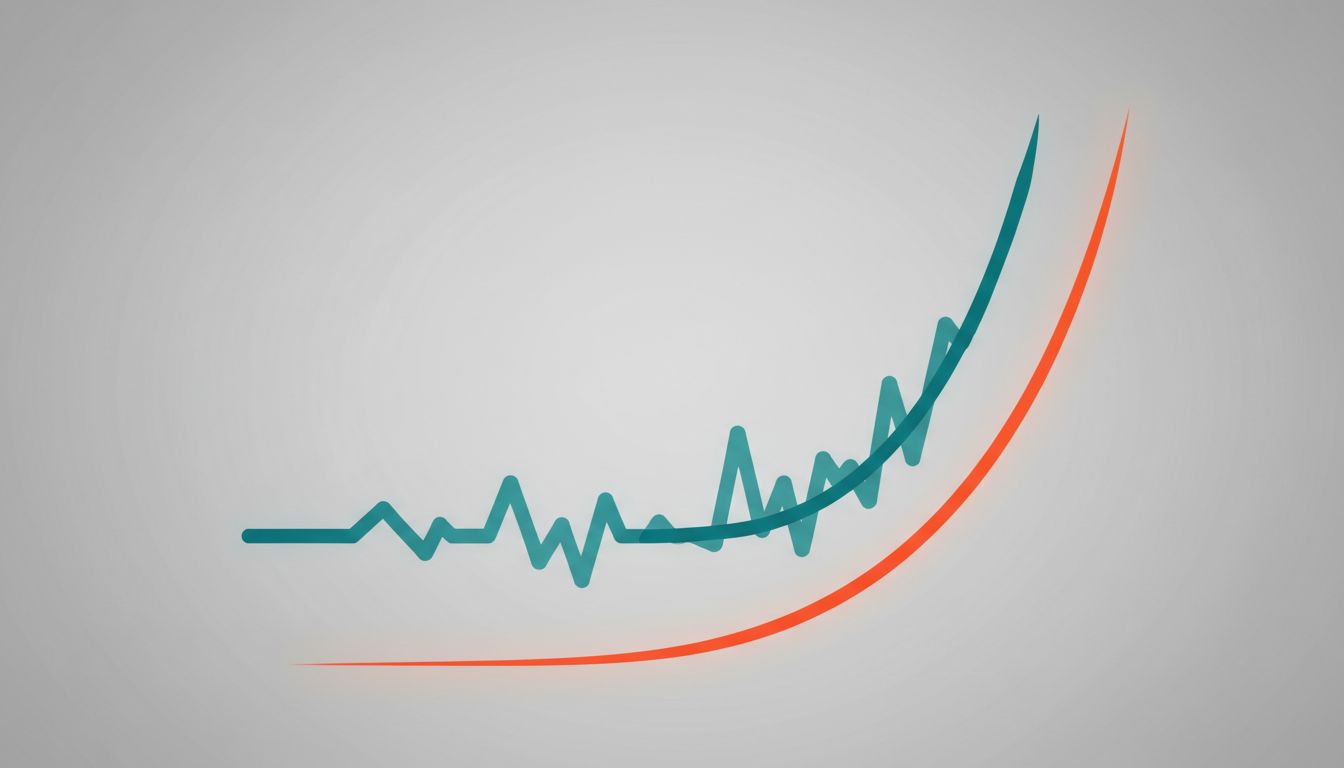

Compounding works in your favor when retention is high. It works catastrophically against you when it isn’t. A company with 30% annual churn isn’t growing, it’s running on a treadmill, replacing lost customers as fast as it adds new ones.

Low-value customers churn faster. This isn’t speculation, it’s a pattern that shows up consistently across SaaS businesses. Customers who paid less, were harder to close, or were a bad fit from the start are the first to cancel when budgets tighten or when a competitor appears. The customers who felt the pain acutely, and paid accordingly, are the ones who stay and expand.

Startups that spend year one accumulating the wrong customers often find themselves in a brutal position by year two: high gross churn, a support team stretched thin, and a product vision distorted by the loudest voices in the customer base. The solution, at that point, is to essentially restart the go-to-market motion while keeping the lights on. Some companies survive it. Many don’t.

Depth of Relationship Is a Competitive Moat

There’s something that happens when you have a small number of customers who genuinely rely on your product. They tell you things they wouldn’t tell a company with a support ticket system. They flag problems before those problems become visible in the data. They introduce you to other buyers who have the same problem. They become references, case studies, and the foundation of your go-to-market playbook.

This is related to the idea that your most demanding customer can become your most valuable one, not in spite of the friction but because of it. The company that fights through hard problems with a demanding early customer often ends up with a more robust product and a deeper understanding of the market than any competitor who grew faster on easier accounts.

Covid-era SaaS companies that chased growth-at-all-costs metrics learned this the hard way. Many of them had impressive logo counts and thin revenue per customer. When market conditions tightened in 2022 and 2023, those customers didn’t fight to keep the subscription. There was no switching cost, no deep integration, no pain associated with leaving. Switching costs are invisible until you try to leave, and the only way to build them is through genuine depth with the right customers.

How This Plays Out in Fundraising

Investors have gotten better at seeing through vanity metrics, at least the good ones have. A founder who can point to eight customers with strong retention, genuine engagement, and clear expansion potential often tells a more compelling story than a founder with 200 customers and a retention curve that looks like a ski slope.

The question sophisticated investors are asking isn’t “how many customers do you have?” It’s “do you know why customers buy, why they stay, and what makes you defensible?” A founder with a small, high-quality customer base usually has sharper answers to those questions because they’ve had the time and the density of relationship to actually figure them out.

This matters when you’re trying to raise capital on forward-looking projections. An investor who believes you deeply understand your buyer and your product-market fit will accept a lower current revenue number than one who sees scale without signal. The story of a company that knows exactly what it’s building and for whom is more fundable than one that’s still experimenting with positioning while managing 200 accounts.

The Discipline This Requires

None of this is easy to execute. Saying no to a customer who wants to pay you money in year one takes a particular kind of confidence that most founders haven’t earned yet. It feels counterintuitive when runway is short and every deal feels like survival.

The practical version of this isn’t “find fewer customers.” It’s “be clear about which customers create the kind of learning and leverage that compounds.” It means setting a price that filters out low-intent buyers. It means disqualifying accounts that don’t match the problem you actually solve. It means treating your early customer list as a strategic asset rather than a vanity metric.

The founders who do this well aren’t being precious about their product. They’re making a bet that the signal from the right ten customers is worth more than the noise from the wrong hundred. Over and over again, in the companies that actually scale, that bet pays off.