The Simple Version

Pricing is not about what something costs to make. It’s about what it’s worth to the buyer, and those two numbers have almost nothing to do with each other.

The Story Most Founders Tell Themselves

A founder I know spent three months building a compliance tool for HR teams. Solid product. Saved companies real hours every week. When it came time to price it, he added up his hosting costs, estimated his time, thought about what felt “reasonable,” and landed on $29 per month.

His first customer signed up in under ten minutes, said it was exactly what they needed, and then mentioned offhand that they’d been paying a consultant $2,000 a month to do the same thing manually.

He had priced a $2,000 solution at $29 because he was thinking about his costs, not his customer’s problem. He eventually repriced, but he spent almost a year at the wrong number. That’s a year of signaling to the market that his product was a minor utility, attracting customers who’d churn the moment a cheaper alternative appeared, and leaving serious money on the table that he needed to hire and grow.

This is not an unusual story. It’s the default story.

Why Cost-Plus Pricing Is a Trap

Cost-plus pricing is the method most founders default to. You add up what it costs to deliver the product, add a margin, and call that the price. It feels principled. It feels fair.

It is also, in most cases, useless as a strategic tool.

The problem is that your costs are irrelevant to your buyer. They don’t care what your AWS bill is. They care whether your product solves a problem that matters to them, and how much that problem is costing them right now, in time, in risk, or in money they’re spending somewhere else.

When you price from costs, you’re essentially pricing from the inside out. You’re answering a question nobody asked.

The Framework That Actually Works

Value-based pricing flips the question. Instead of “what does this cost me to build?”, you ask “what is this worth to the customer?”

That sounds simple but it requires actually talking to customers, which many founders avoid because they’re afraid of what they’ll hear. The conversation you need to have is uncomfortable: What are you doing today instead of using my product? What does that cost you? What would it be worth if that problem went away?

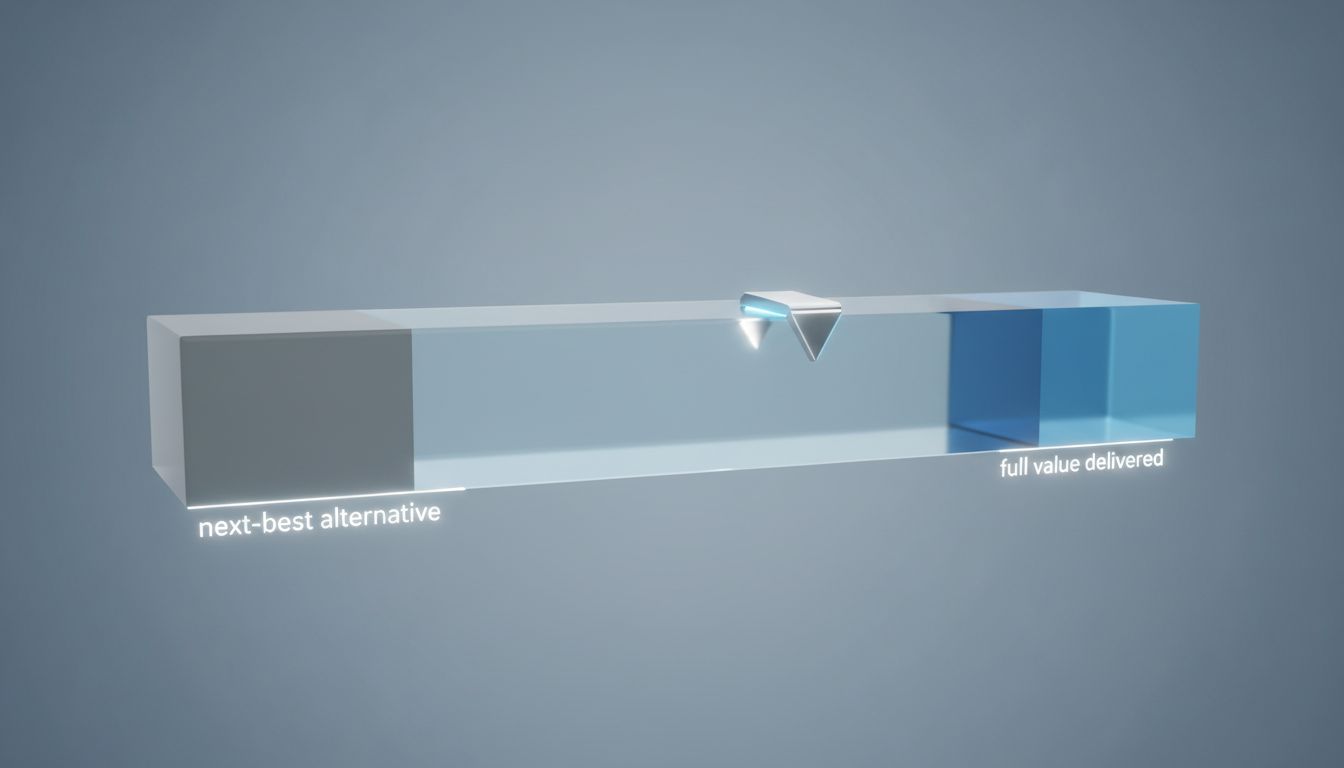

Those answers give you a pricing ceiling. The buyer’s next-best alternative gives you a floor. Your actual price lives somewhere in that range, calibrated by how differentiated you are and how easy it is for the buyer to quantify the value.

Figma is a clean example of this working in practice. They launched at roughly three times the price of Sketch and framed it around what design collaboration was actually worth to product teams, not what it cost to build a browser-based design tool. That pricing decision shaped their positioning, their customer profile, and ultimately how they were perceived in the market.

Higher price signals higher value. That’s not cynical, it’s just how buyers think.

The Psychological Layer Founders Usually Skip

Pricing has a second job beyond capturing value. It communicates something about what you are.

A low price says: this is a commodity, a utility, something you use and forget about. A high price, justified by real value, says: this is a serious tool for serious problems.

Buyers, especially business buyers, use price as a proxy for quality when they don’t have enough information to evaluate quality directly. In the early days of a product, they almost never have enough information. They’re making a bet, and the price tells them what kind of bet this is.

The startup that charges too little is usually dying faster than the one that charges too much, not because low prices kill margin (though they do), but because low prices attract customers who are price-sensitive by nature. Those customers churn faster, negotiate harder, and refer other price-sensitive customers. You end up in a market segment you can’t escape from.

The customers who would have paid more, and stayed longer, and grown with you, took one look at your price and assumed you weren’t serious enough for them.

How to Actually Figure Out What to Charge

There’s no formula that spits out the right number. But there’s a process that gets you close.

First, identify the specific, painful thing your product fixes. Vague value is unpriceable. “Saves time” is not a number. “Eliminates the three hours your ops team spends every Monday reconciling invoices” is a number, because that time has a cost.

Second, find your buyer’s alternative. Not their ideal alternative, their actual current alternative. Usually it’s a spreadsheet, a consultant, a legacy tool, or doing nothing and eating the cost. Price relative to that.

Third, segment your customers. Different buyers get different value from the same product. A freelancer using your tool and a 500-person company using the same tool are not the same buyer. Charging them the same price means one of them is getting a wildly good deal at your expense. This is why seat-based and usage-based pricing exist: they let you capture value proportionally.

Fourth, test higher before you test lower. Founders almost always assume their instinct on price is too high. It’s usually too low. Going upmarket is harder than you think, and many companies that try to move from a cheap positioning to a premium one find the market won’t let them. The wrong customer at the wrong price is a gravity well. It’s genuinely hard to escape.

Finally, remember that pricing is not a one-time decision. It’s something you revisit as you learn more about where your value actually concentrates. The goal in the early days is not to find the perfect price, it’s to find a price that attracts the customers who will help you understand what the product is really worth.

The founders who figure this out early build companies with better margins, better customers, and better odds. The ones who don’t spend years working hard for a number that was never big enough to matter.