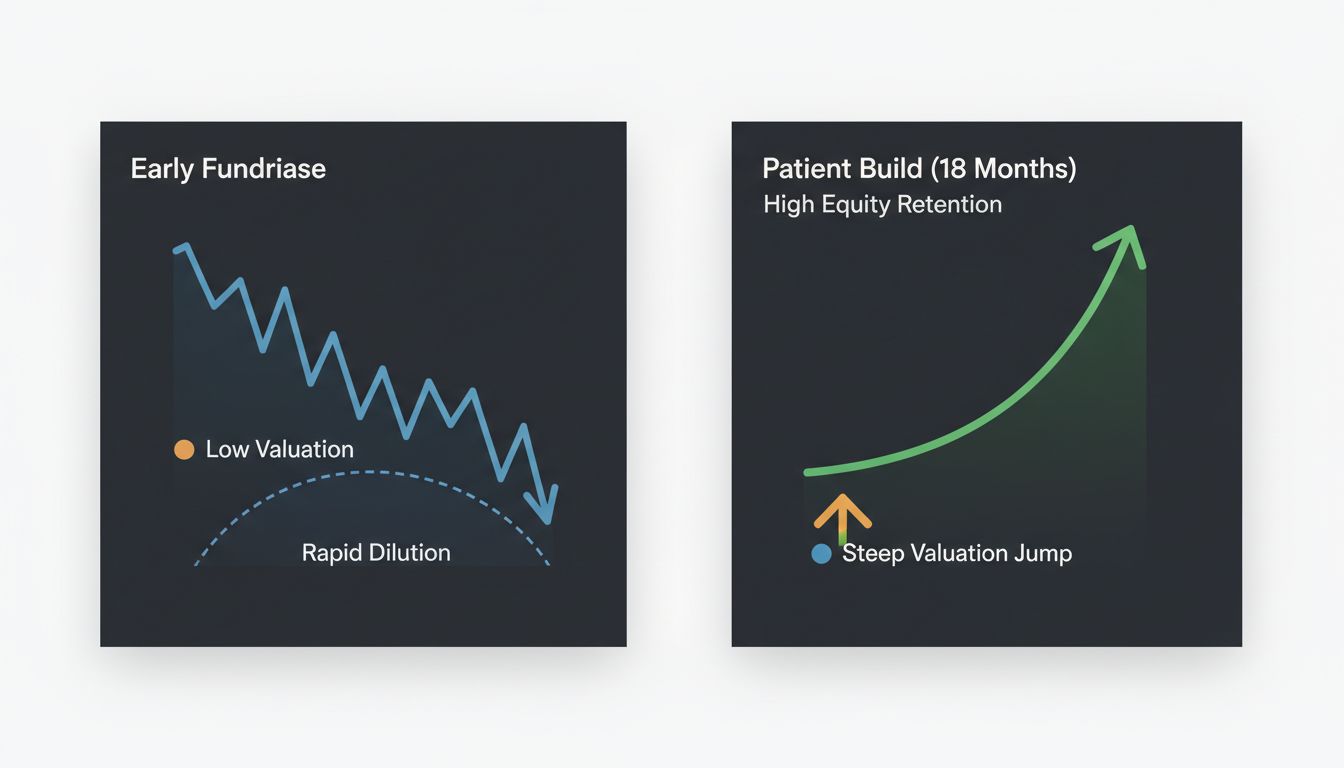

Picture two founders. Both have solid products, paying customers, and warm intros to the same tier of venture firms. One raises their Series A at month nine. The other waits until month eighteen. Three years later, the founder who waited owns significantly more of their company, set a higher valuation, and has a board that largely stays out of the way. The founder who moved fast is still technically “winning,” but they’re doing it with a smaller slice of the pie and a lot more pressure from people who got in cheap.

This pattern shows up constantly, and yet the startup mythology machine keeps pushing speed as the ultimate virtue. Move fast. Raise early. Capture the market. What that advice leaves out is that venture capitalists decide in 30 minutes using pattern recognition most founders don’t know exists, and the patterns they’re looking for are built from data. The founders who wait eighteen months almost always have more of that data.

The Numbers Look Different at Month Eighteen

Here’s the basic math that most early-stage founders miss. At month nine, you might have three months of revenue data, a handful of churned customers, and a growth rate that looks impressive but could be noise. At month eighteen, you have enough data to tell a real story: cohort retention, payback periods, gross margin trends, and at least one or two hard pivots behind you that proved you could adapt.

VCs aren’t being charitable when they reward that patience. They’re being rational. A company with eighteen months of operating history is simply a less risky bet, and less risk commands better terms. The founders who understand this stop thinking about fundraising as a finish line and start treating it as a negotiation where time is their most undervalued asset.

Slack is the clearest example of this in practice. The team spent years building tools internally before they had anything that looked like a fundable SaaS company. What eventually became one of the most successful enterprise software products in history started as something nobody planned to sell. That pattern, of companies emerging from deep operational experience rather than pure fundraising momentum, is more common than the press cycle suggests. Most successful apps that went on to dominate their categories started as internal tools nobody meant to sell.

What You Actually Learn in Those Extra Nine Months

The eighteen-month window isn’t arbitrary. It’s roughly how long it takes to find out if your initial assumptions were wrong in ways that matter.

Most early-stage founders have a theory about their customer. That theory is almost always partially incorrect. The features you built for the customer you imagined will not perfectly serve the customer who actually shows up and pays you. That gap, between imagined user and real user, is the most expensive thing in startup-land, and the only way to close it is time.

Founders who wait learn which customer complaints are noise and which ones are the product roadmap. They discover that winning startups treat customer complaints as a product roadmap not because it sounds good in a pitch deck, but because it’s the fastest path to product-market fit. Every churned customer who told you why they left is worth more than any market research report.

They also learn something harder: whether their initial market was the right one. The counterintuitive truth is that some of the most successful companies found their real market by deliberately starting in the wrong one, using a small, weird beachhead market to sharpen the product before moving into the category they actually wanted to own. Successful startups deliberately choose the wrong market first not out of confusion, but out of strategy.

The Leverage Argument

There’s a negotiating dynamic that first-time founders almost never talk about openly. When you raise early, you are negotiating from curiosity. When you raise after eighteen months of solid metrics, you are negotiating from proof. These are fundamentally different conversations.

A VC who’s been watching your numbers for six months, who knows your competitors have started circling you, and who understands that another firm is running a parallel process, will move faster and compromise more on terms. The same VC pitching a nine-month-old company with three months of revenue is in control of that conversation, and they know it.

Founders who wait also show up with something money genuinely cannot buy: the knowledge of what they don’t know. They’ve been rejected by customers. They’ve weaponized that rejection into product decisions. They’ve watched assumptions fail in real time and updated accordingly. That kind of intellectual honesty is extremely legible to experienced investors, even if founders underestimate how much it matters.

The Risk That Actually Gets You

The obvious counterargument is that waiting exposes you to runway risk. If you burn through your seed before demonstrating enough traction, waiting became permanent.

This is real, and it deserves a serious answer. The founders who execute the eighteen-month strategy successfully are almost always ruthlessly conservative with burn from day one. They hire slowly. They default to doing things manually before building automation. They treat every dollar of seed capital as a month of learning budget, not a month of headcount budget.

This discipline, the kind that keeps your burn low enough to actually reach month eighteen, turns out to be the same discipline that makes you a credible operator in a Series A conversation. Investors aren’t just funding your product. They’re funding your judgment. A founder who reached month eighteen on a lean budget has already demonstrated better judgment than most.

The Meta-Lesson

The eighteen-month rule isn’t really about fundraising timing. It’s about something more fundamental: the willingness to let reality update your beliefs before you lock in the terms under which you’ll operate for the next several years.

The fastest-moving founders often raise quickly precisely because they want external validation that their thesis is correct. The money is secondary. The problem is that a VC check is not actually validation. It’s a bet. And bets placed before the data is in are just expensive guesses.

The founders who wait aren’t being timid. They’re being precise. They’re collecting the evidence they need to show up to the table knowing exactly what they have, who needs it, and why now is the right moment. That posture, confident, data-backed, and unhurried, is exactly what sophisticated investors recognize as the pattern worth backing.

Waiting eighteen months doesn’t mean moving slowly. It means moving deliberately. And in a fundraising environment where VCs pattern-match in under thirty minutes, showing up as the deliberate founder is the single highest-leverage thing you can do before you walk in the door.