Picture this: you’re six months into your Series A process, a term sheet is on the table, and the lead partner asks why your co-founder owns 22% of the company but hasn’t shown up to the office since March. You have thirty seconds to explain something that took eighteen months to become a problem.

This is not a hypothetical. Co-founder departures happen to a large proportion of early-stage startups, and the fallout lands hardest not in the emotional aftermath but on the cap table, in the data room, and in the heads of investors who are trying to figure out whether your company has a governance time bomb buried inside it.

My position is simple: the cap table consequences of a co-founder leaving are more serious than most founders understand, and the decisions made in the first 90 days after a departure will shape the company’s financing trajectory for years. Get it wrong and you will pay, repeatedly.

The Dead Equity Problem Is Real and Investors Know It

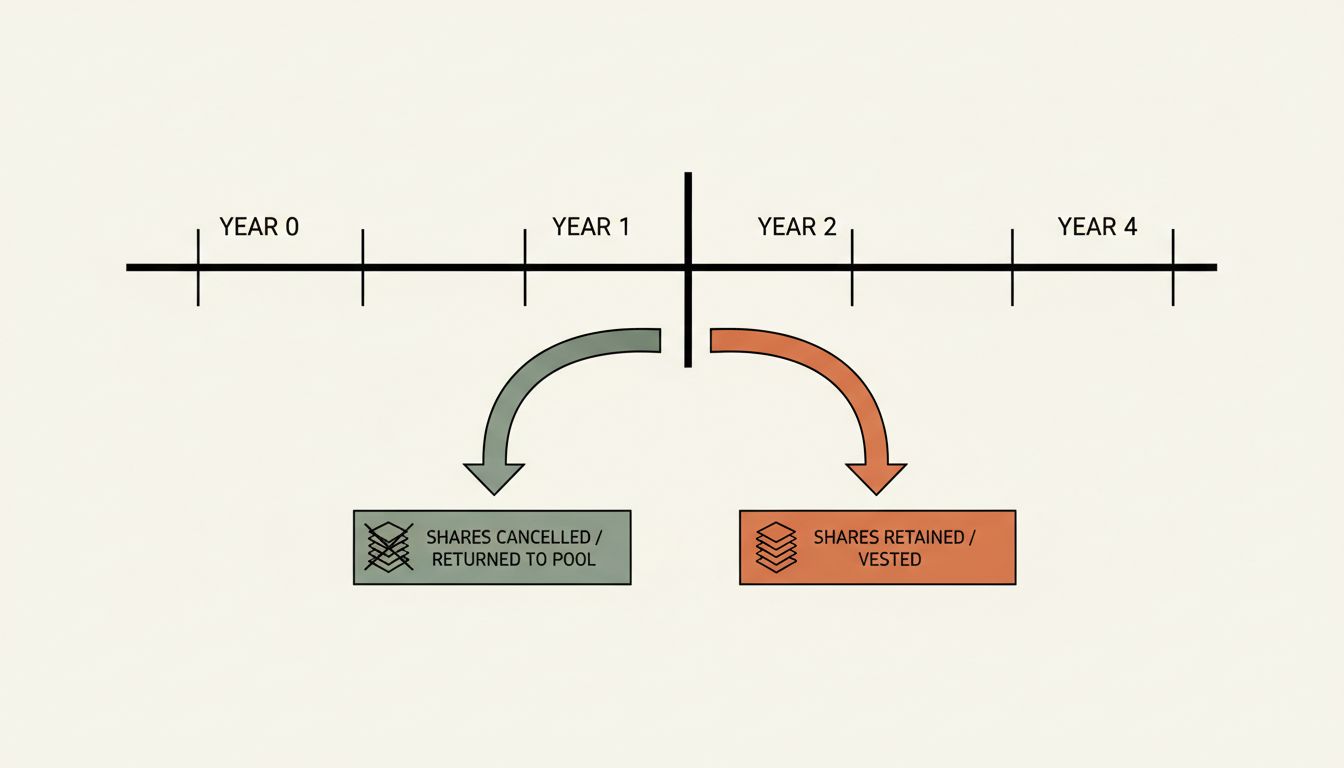

When a co-founder walks out the door, their unvested shares typically get cancelled back to the company’s option pool (assuming you had a vesting schedule in place, which you absolutely should). The vested portion is theirs. Full stop.

This is where founders make the first mistake. They let the departing co-founder keep a large block of fully-vested equity, assume it won’t come up again, and move on. But every investor doing diligence will notice a significant shareholder who has no role, no information rights obligation, and no incentive to make decisions in the company’s interest. That person can complicate consent processes, create friction in future financing rounds, and in a worst case, become a nuisance vote on actions requiring shareholder approval.

The cleaner outcome is a repurchase. Many co-founder agreements include a repurchase right at original cost for vested shares upon departure, especially when the departure happens early. If yours doesn’t, you can still negotiate one, and it’s worth the awkward conversation. Companies that clean this up early raise cleaner rounds. It is not a coincidence.

Vesting Cliffs Are Your Best Friend, Until You Ignore Them

A four-year vest with a one-year cliff exists precisely for this scenario. If your co-founder leaves before the cliff, nothing vests and the cap table stays clean. But a surprising number of early co-founder agreements are looser than this, particularly when founders know each other well and trust feels like a substitute for structure.

The cliff is not a statement of distrust. It is a mechanism that protects both parties. A departing co-founder who hits the cliff owns equity proportional to their actual contribution window. A founder who stays doesn’t spend the next five years watching a former colleague collect proceeds from work they didn’t do.

If you skipped the cliff, or set a shorter one as a goodwill gesture, and the departure happens anyway, you’re now in a negotiation instead of a formula. Some of those negotiations go fine. Many do not.

The Hiring Signal You Aren’t Thinking About

Cap table cleanup after a departure matters for investors. It matters at least as much for senior hires.

The VP of Engineering you’re trying to recruit in month eighteen will ask about the founding team. When they find out a co-founder left and owns a substantial chunk of equity with no ongoing relationship to the company, their next question (often unasked) is: what happened, and could it happen to me? Dead equity on a cap table reads as unresolved conflict to anyone who has seen this before. It signals that the founding relationship broke down and that the legal paperwork may not have caught up.

Senior candidates who have options will factor this into their decision. The best ones usually have options.

Get the Paperwork Right Before the Emotions Cool

There is a narrow window after a co-founder departure when everyone is still operating in relative good faith, the situation is fresh, and the departing person is still motivated to resolve things cleanly. That window closes. Sometimes it closes fast.

Use it. Get a termination agreement signed that addresses: the final vested share count, any repurchase rights the company is exercising, IP assignment (critical, do not skip this), and a standard release. If the departing co-founder is going to remain on the cap table with a meaningful stake, formalize what that means for information rights and consent obligations.

Founders who delay this process because the conversation is uncomfortable routinely find themselves a year later trying to get signatures from someone who now has a lawyer and different priorities. That is an expensive lesson.

The Counterargument

The reasonable pushback here is that being aggressive about repurchases or strict about vesting creates animosity that isn’t worth it, especially in a small startup community where reputations matter. Some founders argue that treating a departing co-founder generously, even at some cap table cost, buys goodwill that pays off in referrals, in community perception, and in the co-founder’s willingness to be a constructive shareholder.

This is true in some cases. If the departure is genuinely amicable, the equity stake is small, and the former co-founder is likely to be a positive ambassador, letting some vested equity walk out the door may be the right call.

But this argument gets stretched to cover situations where it doesn’t apply. Founders use “keeping the relationship clean” as a reason to avoid difficult paperwork when the real reason is that they hate conflict. Clean relationships and clean paperwork are not mutually exclusive. The companies I’ve seen handle departures best do both.

The position stands: the cap table consequences of a co-founder departure are serious, the decisions are time-sensitive, and most founders underestimate both. Handle the paperwork in the good-faith window, repurchase where you can, and don’t let sentiment become a structural liability that shows up in your Series A data room. The investor across the table has seen this before. Make sure your story is the clean version.