The simple version

Burn rate tells you how fast you’re spending money. What it doesn’t tell you is whether that spending is moving you toward a business that can sustain itself, which is the only question that actually matters.

Why burn rate became the metric everyone watches

Picture a founder in a board meeting, 18 months post-seed. The deck has a burn rate slide. Everyone nods. Someone asks if the team has considered “rightsizing.” The founder defends the number. The meeting ends. Nobody asks the harder question: what are we getting for it?

Burn rate became the default metric because it’s easy to calculate and easy to compare. Tell a VC you’re burning $150K a month and they immediately have a frame of reference. Runway math is simple arithmetic. And in the zero-interest-rate years, when capital was cheap and the priority was growth at any cost, tracking burn was mostly about making sure the checking account didn’t hit zero before the next round.

That environment is gone. But the fixation on burn rate stuck around, and it’s leading a lot of founders to optimize for the wrong thing.

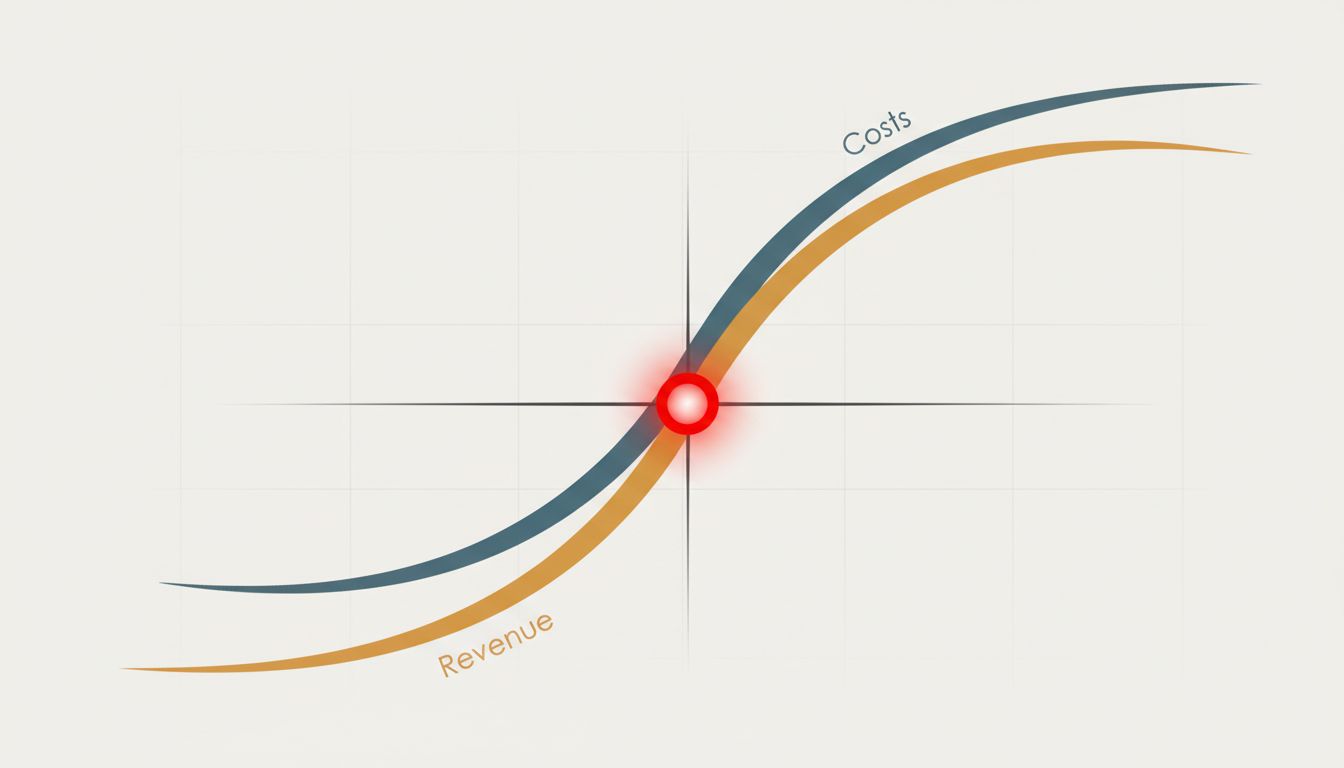

The number you should actually care about

Burn multiple is the metric that cuts through the noise. The formula is straightforward: net burn divided by net new ARR. If you burned $500K last quarter and added $250K in new annual recurring revenue, your burn multiple is 2x. You spent two dollars to generate one dollar of new revenue.

A burn multiple under 1x is exceptional. Under 2x is good. Over 3x, you have a real problem regardless of how much cash you have in the bank, because you’re telling a story about a business that gets more expensive to grow over time, not less.

David Sacks popularized this framing, and it’s the most useful single ratio I’ve seen for early-stage companies trying to understand whether their spending is working. It forces a connection between the cost side and the output side that burn rate alone never does.

Here’s why this matters more than you might think. Two companies can have identical burn rates and completely different fates. Company A burns $200K a month and adds $100K in new ARR each month. Company B burns $200K a month and adds $300K in new ARR each month. Same headline number. One of those companies is building something; the other is running a very expensive experiment.

Burn rate treats both companies the same. Burn multiple doesn’t.

The efficiency trap hiding inside “low burn”

Reducing burn is not inherently good. This is the part that gets founders in trouble.

When times get hard, the instinct is to cut. Lay off the marketing team, freeze hiring, reduce cloud spend. The burn rate drops. The board meeting feels better. Runway extends. But if those cuts reduce your ability to generate new revenue, you haven’t solved anything. You’ve just slowed the clock while the underlying problem festers.

I’ve watched companies cut their way into irrelevance. They hit 18 months of runway, then 24 months, but the growth curve flattened to nearly nothing. They were efficient at spending money and terrible at making progress. Investors noticed. The next round didn’t come.

The question isn’t “how do we spend less?” The question is “how do we spend less per dollar of new revenue we generate?” Those are very different problems with very different solutions.

What actually improves your burn multiple

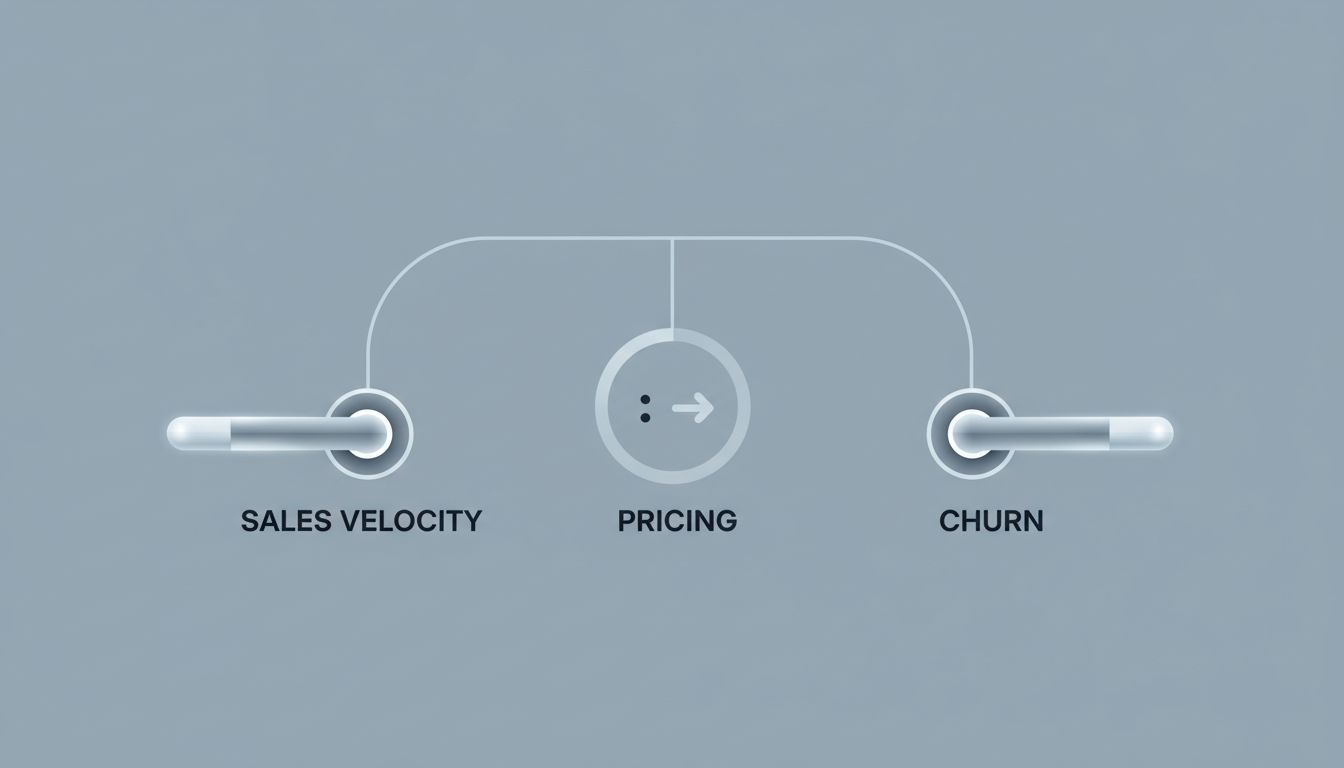

Three levers move this number, and they’re not all on the cost side.

Sales velocity. If you can close deals faster, you generate the same ARR with fewer months of payroll, commissions, and overhead loaded against it. Shortening a 90-day sales cycle to 45 days doesn’t just feel better; it mechanically improves your efficiency.

Pricing. Underpriced products force you to win more customers to hit the same revenue, which means more sales headcount, more customer success, more everything. Pricing your product too low tells buyers it doesn’t work, and it makes your unit economics quietly terrible at the same time.

Churn. This is the sneaky one. A company losing 3% of ARR monthly has to generate enormous new ARR just to stay flat, which means every dollar of new growth is fighting against a leak. High churn inflates your burn multiple because your net new ARR figure is suppressed. Fixing retention is often the highest-leverage move a struggling SaaS company can make, and it rarely shows up in the burn rate conversation.

How to actually use this in practice

Track burn multiple every quarter, not just burn. Put both numbers in your board deck. If your burn multiple is rising, that’s a warning sign even if absolute burn is flat. If it’s falling, that’s evidence your go-to-market is working, and that’s worth more in a fundraising conversation than a low burn rate by itself.

Set a target. Most growth-stage investors want to see burn multiples trending toward 1.5x or below before they’ll get excited about a Series B. That gives you a concrete goal to optimize against instead of just trying to minimize a spending number in isolation.

And resist the urge to benchmark your burn rate against competitors. You don’t know their revenue growth. You don’t know their customer quality. Burn rate comparisons are almost always misleading. Burn multiple comparisons, if you can get them, tell you something real.

The founders who survive the current environment will be the ones who figured out that capital efficiency is a ratio, not a subtraction problem. Spend less than you earn, yes, but more specifically: generate as much new revenue as possible for every dollar you put to work. That’s the discipline that actually builds companies.