A friend of mine spent three years at a Series A startup. She had 0.4% equity, fully vested, in a company that got acquired by a large tech firm for what the press release called “a significant investment in talent.” The deal closed. She got a retention bonus and a job offer. Her equity paid out zero.

She was not unusual. She was the norm.

Acqui-hires are one of the most misunderstood exits in tech, in part because everyone involved has a reason to be vague about how they actually work. Founders get to say they had an exit. Acquirers get to announce a talent acquisition. Employees get to feel like they landed somewhere soft. The mythology holds together until you actually read the deal terms, at which point the whole thing looks a lot more like a structured wipeout dressed up as a win.

My position is simple: in most acqui-hires, common equity holders get little to nothing, and this is not an accident. It is the point.

The Liquidation Stack Eats First

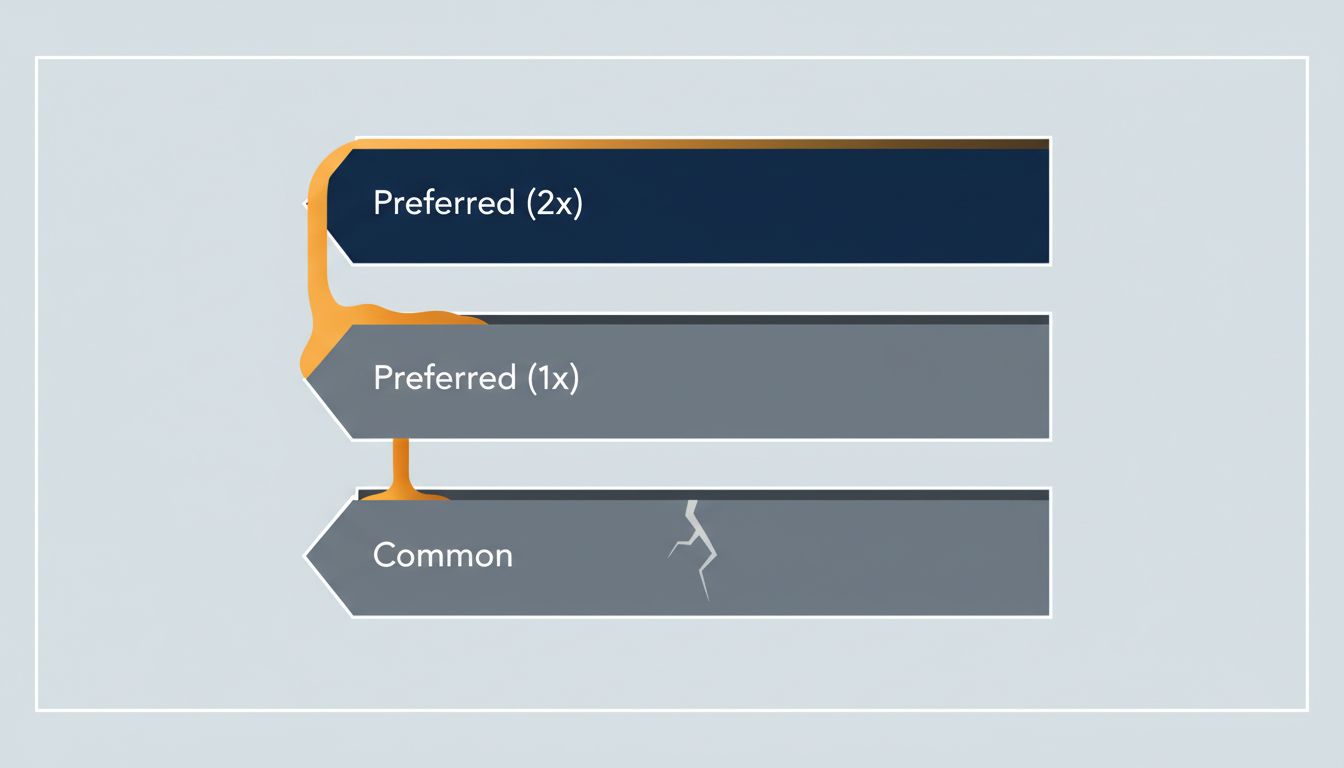

To understand why, you need to understand what happens to a startup’s capital structure before any acquisition closes. Most venture-backed companies have issued preferred shares to investors, and those shares almost always carry liquidation preferences. A 1x liquidation preference means investors get their money back before anyone else sees a dollar. Many deals include 2x preferences or participating preferred terms, which let investors double-dip: they get their preference first, then participate in the remaining proceeds pro rata.

In a distressed acqui-hire, the acquisition price is usually low. The company is being sold because it ran out of runway, failed to find product-market fit, or simply got beaten. When the price is $15 million and investors put in $20 million with a 1x preference, the math is over before it starts. Common shareholders, which means most employees, get nothing. The acquiring company knows this. The investors know this. The founders usually know this. The engineers who just got offered $180,000 salary plus a retention bonus are often the last to figure it out.

Retention Bonuses Are Not Equity Payouts

The move that obscures all of this is the retention bonus. Acquirers routinely offer employees cash packages that vest over two to four years, which feel like compensation for giving up equity. They are not. They are compensation for showing up to work at the new company. The framing matters enormously, because employees often accept the bonus as a substitute for the equity conversation rather than as a separate negotiation.

This is not illegal. It is not even particularly unusual. But it does mean that an engineer with four years of vested equity in a company can walk out of an acquisition with exactly what a new hire off the street would get, minus the unvested portion they forfeited by leaving before the retention cliff.

The acquirer’s incentive here is clean: they want the talent, they do not want to pay for the equity. Structuring the deal so that the acquisition price is absorbed by liquidation preferences, while separately offering employment packages to the people they actually want, achieves exactly that.

Founders Often Do Fine. That Is Not a Coincidence.

Here is where the incentive misalignment gets uncomfortable. In many acqui-hires, the founders receive specific deal terms that common shareholders do not. These can take the form of consulting agreements, earnouts tied to their personal retention, or direct payments for IP that are structured outside the standard equity distribution.

This is legal, and sometimes it is even reasonable, because acquirers genuinely are buying access to specific people. But it creates a situation where the founders who negotiated the deal have a financial outcome that looks nothing like the outcome experienced by the people who worked for them. A founder who takes home $2 million from a consulting agreement while the cap table produces zero for employees is technically compliant with the deal terms. It still feels like a betrayal, because it is.

Employees who have watched the startup mythology up close know this dynamic exists. Most still do not read their term sheets carefully enough to anticipate it.

The Counterargument

The honest version of the counterargument is this: employees chose to take startup risk. The equity was always contingent. A vesting schedule is not a promise of a payout, it is a promise of ownership in a vehicle that might pay out. If the company failed to build enough value to clear its liquidation stack, that is the risk every common shareholder accepted.

There is real merit here. Equity compensation is not salary. The risk is disclosed, at least formally, even when the complexity of preferred liquidation preferences is not explained at the offer stage. Holding startups to an implied guarantee of payout would change how early-stage compensation works in ways that would not obviously help employees.

But this counterargument is strongest when applied to genuine failure. The problem with acqui-hires is that many of them are not failures for everyone. The founders get paid. The investors recover something. The acquiring company gets the people they wanted at a price that excluded the common equity holders. Calling that a shared risk outcome requires a definition of “shared” that most employees would not recognize.

What to Actually Do About It

If you have equity in a startup and you hear the words “strategic acquisition” or “acqui-hire” in a all-hands, the first question is not what the deal is worth. The first question is what your liquidation stack looks like and whether the deal price clears it.

Get a copy of your company’s certificate of incorporation and find the preferred stock terms. Ask directly whether any part of the deal consideration is being paid outside the equity distribution, as consulting fees or retention arrangements to founders specifically. Ask whether the acquisition price is sufficient to return any proceeds to common shareholders before factoring in any retention bonuses you’re being offered separately.

Most employees will not ask these questions, because asking them feels adversarial and the retention bonus feels real and immediate. That is exactly why the structure works.

The acqui-hire is not inherently predatory. Sometimes it genuinely is the best available outcome for everyone. But it is designed, structurally, to prioritize investors and select founders while compensating everyone else through employment rather than equity. Walking in with that understanding is the only way to negotiate from anything approaching a real position.