In the mid-2000s, AMD had a stretch where it was genuinely beating Intel on performance per dollar. Its Athlon 64 chips were better than what Intel was shipping, and it was gaining real market share. And then Intel crushed it. Poured billions into fab capacity, signed exclusive agreements with OEMs, and drove AMD to the edge of bankruptcy. Intel won. And spent years as one of the least profitable large-cap chip companies in tech, burdened by the infrastructure it had built to stay on top.

AMD, forced to spin off its fabs into what became GlobalFoundries, went fabless. Lighter. More flexible. By the time Lisa Su took over and started shipping Ryzen, AMD was a company that could generate serious margins without owning a single factory. Intel owned everything and was being eaten alive by the cost of owning everything.

This is not a coincidence. It is the normal shape of competitive dynamics in tech markets.

The Burden of the Crown

Being the market leader in tech means you have to act like it. You have to support the broadest possible customer base. You have to maintain backward compatibility that nobody asked for but everybody depends on. You have to staff sales teams for deals that barely break even because losing a flagship account would make a bad headline. You have to show up at every industry conference, sponsor every trade organization, and litigate against every patent troll who figures out your pockets are the deepest ones in the room.

None of this is optional. Market leadership is a performance as much as it is a financial position. And performance is expensive.

The second-place player can skip most of this. They win business by being better on specific dimensions that matter to specific customers. They don’t have to be everything to everyone because nobody expects them to be. They can say no to bad deals. They can focus R&D on the areas where they can actually win instead of spreading it across everything to protect a perimeter.

This is related to something worth understanding about startup pricing: the cost structure of fighting to maintain leadership is one reason underpricing doesn’t kill startups the way most people think. It’s the infrastructure of dominance that does the real damage.

The Advertiser Subsidy Problem

Look at search. Google’s market share in search advertising is enormous. Bing’s is small. And for years, Microsoft’s search business has generated margins that look very healthy relative to the revenue base, partly because the advertising market on Bing is less saturated, which means advertisers competing for keywords face less auction pressure, which means Microsoft captures a different margin profile than you’d expect from a distant second-place player.

Google has to invest massively in infrastructure just to maintain the latency and quality that its market position demands. It has to index more of the web, more often. It has to fight the SEO spam economy that specifically targets it because it’s worth gaming. It has to fund entire research divisions to stay ahead of quality problems that come from being the default choice for billions of queries a day.

Bing has a smaller, somewhat self-selected user base that tends to be less adversarially gamed. The economics are just different.

This pattern shows up in cloud, too. AWS has spent years defending its position by building out more regions, more services, and more compliance certifications than any rational business case would require for a single customer. It’s the cost of being the default. Google Cloud and Azure can be more selective about where they invest because they’re selling on specific strengths rather than maintaining omnipresence.

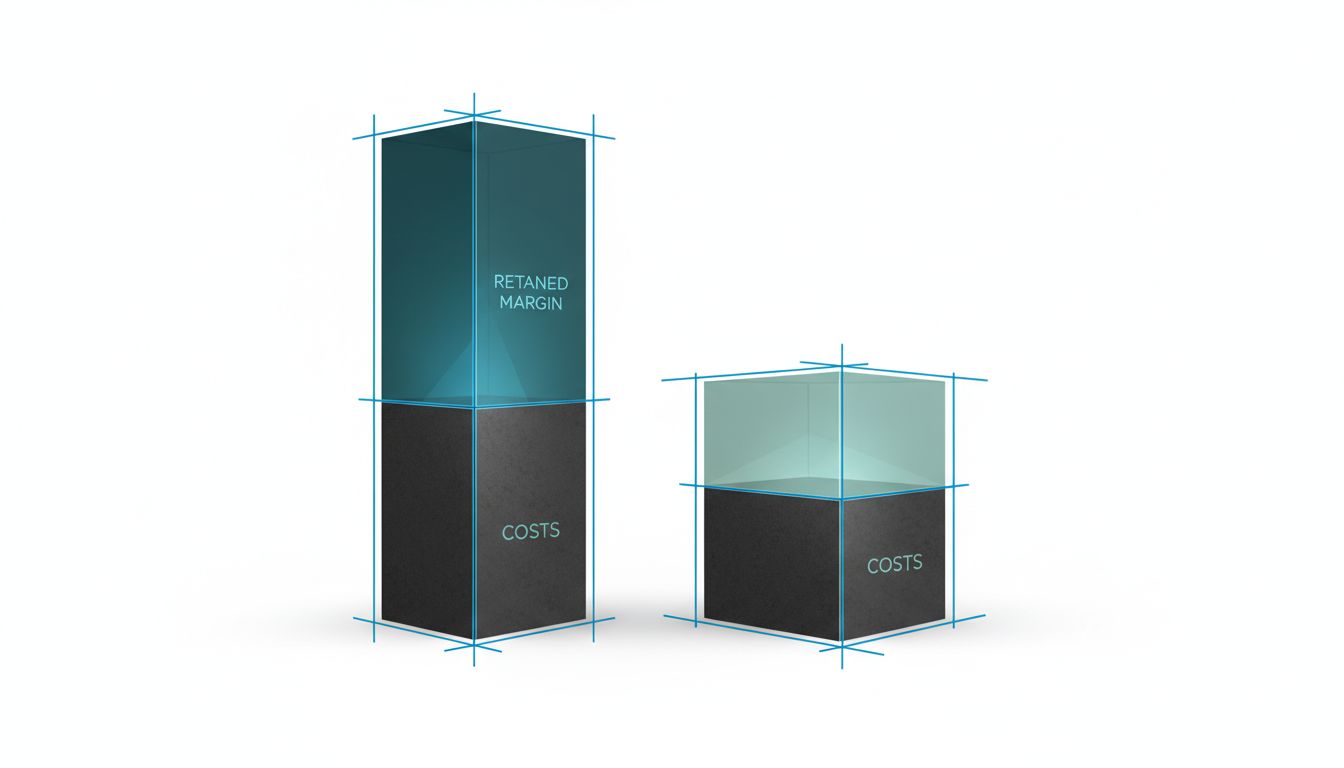

Customer Mix Follows Market Position

Here’s a dynamic that doesn’t get talked about enough. Market leaders accumulate the most price-sensitive customers because price-sensitive customers default to the leader. The biggest market share players often have the worst customer economics at the margin, because the last customers they won were the ones who needed the most discounting to close.

The second-place player’s customers made an active choice. They evaluated the leader and decided it wasn’t right for them, then chose the alternative. That selection process tends to produce customers who are buying on fit rather than price, which means they churn less and complain less about price increases.

Salesforce is the clear leader in CRM. HubSpot built a genuinely profitable business by winning customers who found Salesforce too complex or too expensive, and by owning that segment deeply rather than fighting for the enterprise accounts where Salesforce has entrenched relationships. HubSpot’s net revenue retention and customer satisfaction numbers have consistently been strong because its customers are there for reasons other than default.

This is not a strategy you can execute from the top. You have to actually be second to benefit from it.

Where Second Place Fails

This doesn’t work in every market, and it’s worth being clear about that. In markets where network effects are strong enough that the product literally gets worse as you lose share, second place is just slow death. Social networks are the clearest example. MySpace was once the leader. Being in second place did not give it a profitability cushion. It gave it a shrinking user base and a product that degraded relative to Facebook as the gap widened.

Payments have a version of this too. The value of a payment network is partly its ubiquity, so a distant second-place payment rail faces real product problems that a distant second-place CRM does not.

The pattern holds most reliably in markets where the product competes on features and price rather than on network membership. Enterprise software, developer tools, cloud infrastructure, hardware, security products. Markets where a customer can have a genuinely good experience with the second-place product even if their entire industry is on the leader’s platform.

The Lesson Is Not to Aim for Second

Nobody builds a company trying to be second. And this analysis is not an argument for sandbagging. The reason second place is often more profitable is not that second place is strategically superior, it’s that the costs of first place are higher than the revenue premium justifies. The market leader was usually trying to win, and did win, and is now paying for it.

What it means in practice is that when you’re building a business in a market with a clear leader, the worst strategy is to try to out-leader the leader. You won’t out-invest them, you won’t out-distribute them, and you’ll end up with all the costs of trying to be ubiquitous without the revenue base to support those costs.

The better move is to be excellent at something specific that the leader is too encumbered to be excellent at. Win a segment deeply. Build a customer base that chose you. Keep your cost structure lean enough that you don’t need 40% market share to generate returns.

AMD didn’t beat Intel by trying to have more fabs than Intel. It beat Intel by not having any fabs at all, and being very good at chip design. The crown was always Intel’s. AMD just had better economics.