Salesforce and Rackspace launched within a year of each other, both riding the early wave of internet-delivered software, both burning through venture capital, both promising to replace expensive on-premise systems. By most external measures in 2005, they looked like cousins. Today Salesforce has a market capitalization above $200 billion. Rackspace went public, went private again, went public again, and has spent years trading at a fraction of its peak value while struggling to find a durable business model. The divergence was visible early, and it was hiding in gross margin.

Gross margin, for a software company, is revenue minus the direct cost of delivering that revenue, divided by revenue. For a pure software business, those direct costs are mostly servers, support staff, and infrastructure. What remains after those costs is the money available to fund sales, marketing, research, and eventually profit. It is not a glamorous metric. Investors spend more time talking about revenue growth rates and total addressable market. Gross margin sits quietly in the middle of the income statement, underappreciated until the business hits a wall.

Rackspace sold managed hosting. A customer paid Rackspace to run their servers for them. Every new customer meant more physical hardware, more data center space, more engineers to babysit those machines. Revenue scaled, but costs scaled nearly as fast. Rackspace’s gross margins hovered in the low-to-mid 60s as a percentage of revenue during its growth years, which is respectable for a services business but not exceptional.

Salesforce sold access to software running on shared infrastructure. A new customer signing up did not require Salesforce to buy proportionally more servers. The marginal cost of serving an additional customer was low. Gross margins ran consistently above 70 percent and eventually climbed past 75 percent as the company scaled. That gap, ten to fifteen percentage points, compounded into something significant over time.

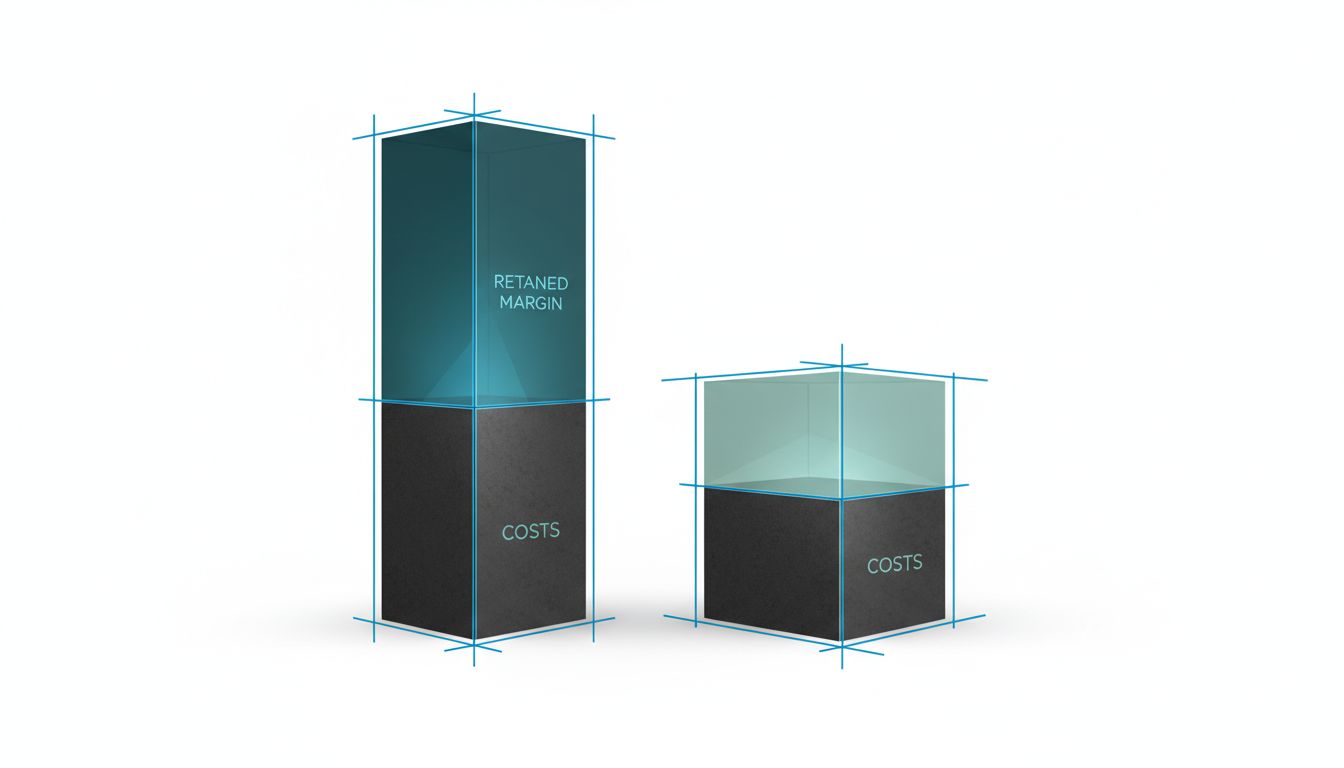

Here is why the compounding matters. A company with 70 percent gross margins that grows to $1 billion in revenue has $700 million available for operating expenses before hitting zero operating income. A company with 55 percent margins has $550 million. Both companies might be growing fast, both might have enthusiastic investors, but the first company can outspend the second on sales hiring, product development, and customer acquisition while maintaining the same operating loss. In a market where distribution determines winners, that structural advantage is not temporary.

The deeper issue is what gross margin predicts about a business model’s future. Low gross margins in software almost always signal one of two problems. The first is that the product is genuinely difficult to deliver and requires substantial human intervention, meaning the company has not figured out how to scale without adding headcount proportionally. The second is that the company is subsidizing its product with services to compete on price, which signals competitive weakness in the core software itself.

Rackspace eventually tried to pivot toward managed cloud services, essentially becoming the human expertise layer on top of AWS and Azure. It is a coherent strategy, but it is a services business, and services businesses have structural margin ceilings that pure software does not. When a rival goes to market with a dramatically lower price and no equivalent service wrapper, the services company has limited room to respond without destroying its own economics.

The contrast becomes sharper when you look at what high gross margins enable operationally. Salesforce spent aggressively on sales and marketing for years, sometimes more than 50 percent of revenue, and still generated positive free cash flow at scale. That math works only when gross margins are high enough to absorb it. A company with 55 percent gross margins cannot afford a Salesforce-style sales motion without accepting permanent losses.

This is not an argument that gross margin alone determines fate. Companies with high gross margins fail for other reasons, and some services businesses generate excellent returns for shareholders. The point is narrower: in software specifically, gross margin is a structural constraint, not just a financial ratio. It determines the ceiling on how much you can invest in growth, the floor on how low you can cut prices in a price war, and the buffer you have when the market slows.

Consider what happened to companies selling software with embedded hardware in the 2010s. Security appliance vendors, for instance, carried margins significantly below pure software vendors because their product required physical boxes. As cloud-delivered security emerged from companies like Zscaler, which reported gross margins above 75 percent at scale, the appliance vendors faced a competitor that could price aggressively, invest heavily in product, and still sustain the business. The margin structure was telling the story years before the market share data confirmed it.

The lesson for founders is to treat gross margin not as a financial reporting exercise but as a product design question. Every architectural decision, every choice about how much human support a customer requires, every decision about whether to build or buy infrastructure capability, has a direct effect on the long-run gross margin of the business. A product that requires significant professional services to implement is not just operationally complex; it is a strategic liability because it caps margins and attracts competitors who can deliver the same outcome more efficiently.

The lesson for investors is that revenue growth without gross margin expansion, or worse, with gross margin compression, deserves serious scrutiny. A company growing revenue at 40 percent per year while watching gross margins decline is not building a more valuable business at scale. It is discovering that its cost structure does not support its pricing, which is a problem that rarely resolves itself without a fundamental change to the product or the market position. As underpricing can quietly destroy a startup’s unit economics, so can a business model that was structurally thin from the start.

Rackspace was not badly managed. It built real products, served real customers, and competed effectively for years. The constraint was structural. A managed hosting business competes on execution and relationships, not on margin expansion, because margin expansion in that model requires either raising prices or eliminating the human labor that defines the service. Neither is easy to do without losing customers.

Salesforce faced no such ceiling. Higher margins funded more sales investment, which funded more revenue, which funded more product development, which extended the competitive moat. The compounding was not accidental. It was the direct consequence of having built a product whose cost structure rewarded scale.

Ten years from now, the software companies still operating and growing will almost certainly share one characteristic: they found a way to deliver genuine value without letting their cost of delivery grow as fast as their revenue. Gross margin is not a perfect predictor. But it is the closest thing the income statement has to one.