In 2008, Jason Fried got a call from a VC firm. They wanted to talk about a Series A. Basecamp, then called 37signals, was already profitable, growing steadily, and shipping software that people paid for. Fried turned them down. He has turned down every similar conversation since.

Most people hear that story and file it under “founders who got lucky and could afford principles.” That reading is wrong, and it misses the actual lesson.

The Setup

37signals launched Basecamp in 2004 as a side product. The company was a web design consultancy that needed better project management software and couldn’t find any. So they built it, charged for it, and within a year it was making more money than the consulting work. They spun down the consulting arm and focused on software.

They never raised outside capital. Not a seed round. Not an angel check. Nothing.

By the time competitors started arriving with venture backing, Basecamp was already profitable and had been for years. And the competitors had a problem: they couldn’t figure out what exactly they were competing against. Basecamp wasn’t trying to be an enterprise platform. It wasn’t trying to win every customer. It was priced simply, built simply, and run by a team small enough to fit in a single office.

What Actually Happened

The project management software category attracted enormous investment through the 2010s. Asana raised over $450 million before going public. Monday.com raised hundreds of millions and went public at a valuation exceeding $6 billion. Notion raised at a $10 billion valuation. The category became one of the most funded in productivity software.

Basecamp, meanwhile, kept doing what it had always done. Small team. No outside investors. Profitable every year. They wrote books about their approach. They blogged constantly about how they worked. They weren’t hiding.

Here is the interesting part: the funding their competitors raised wasn’t just capital. It was obligation. Asana had to grow in ways that justified a billion-dollar outcome for investors. Monday.com had to expand into enterprise, then into CRM-adjacent features, then into platform territory, because that’s what the model required. The funding dictated the product direction as surely as any roadmap decision.

Basecamp never had that obligation. They could ship the product they actually wanted to ship. They could say no to features. They could hold prices steady for years. They could make unpopular calls, like their controversial decision to ban internal political discussions, and absorb the PR hit without anyone on their cap table calling to express concern.

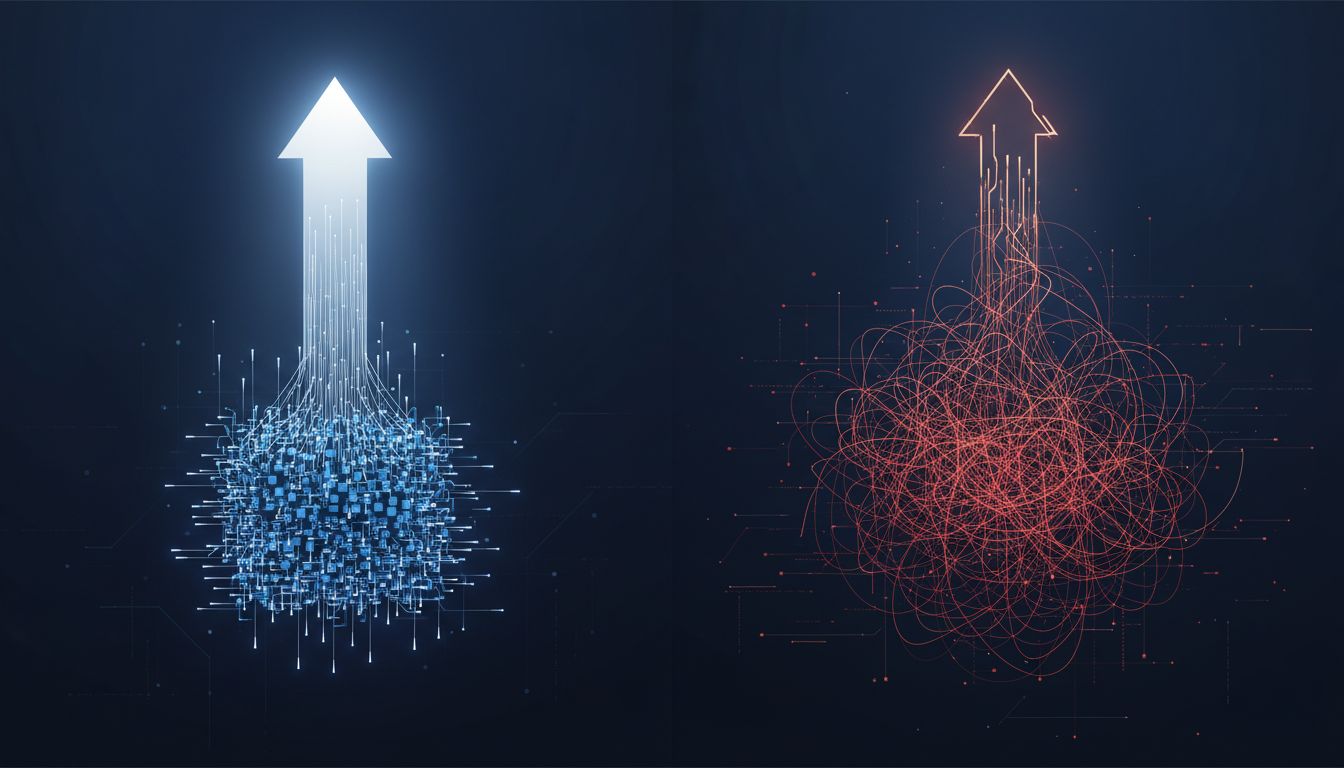

Constraint, in their case, was architecture. Every decision about what not to build, what not to pursue, what not to optimize for, flowed from the same source: they only had the resources their customers gave them, and that was enough.

This connects to something worth naming directly. When you raise significant venture capital, growth becomes the product, not the company. The reporting cadence, the board composition, the pressure to show trajectory on every metric, all of it reshapes what decisions are even available to you. Founders often don’t feel this until it’s deeply embedded in how the company operates.

Why It Matters

The conventional wisdom in startup circles is that capital equals competitive advantage. More money means faster hiring, faster shipping, more marketing, more distribution. Sometimes that’s true. If you’re building infrastructure, or you’re in a category where the first player to reach scale wins the whole market, underfunding is a real risk.

But most software categories don’t work that way. Most of them are fragmented markets where multiple players coexist at different price points, serving different customer segments. In those markets, the advantages that capital buys can become liabilities.

Hiring fast creates coordination overhead. Shipping fast creates technical debt. Aggressive marketing acquires customers who don’t actually fit the product. And all of it requires more capital, which requires more growth, which requires more of the same.

Basecamp avoided all of that by never starting the cycle. Their team stayed small by design. For years it hovered around fifty people globally. That number isn’t an accident; it’s a product decision. A small team writes software that a small team can maintain, which means the product stays coherent, which means customers can actually use it.

The companies that raised enormous rounds are now, many of them, dealing with what growth-stage companies always deal with: layoffs, refocusing, feature bloat they can’t quite undo, and a customer base they expanded into segments that don’t actually love the product. That’s not a failure of execution. It’s a structural outcome of the model they chose.

What We Can Learn

Basecamp is an unusual company in some ways. Fried and David Heinemeier Hansson had unusually clear convictions about how they wanted to run a company, and they stuck to them in an environment that applies constant pressure toward growth-at-all-costs thinking. That’s harder than it sounds.

But the lesson isn’t “don’t raise money.” The lesson is more specific than that.

Capital is a forcing function. It forces decisions about scale, about pace, about what the product has to become. Before you take it, you should be able to answer honestly: does this company need to be a billion-dollar company? Does this category reward scale the way the venture model requires? Or are we raising because that’s what founders do, because the round validates the idea, because it feels safer than betting on the business itself?

If you can build a profitable company at a size that the market actually supports, without the overhead of investor expectations, you have something most well-funded competitors can’t easily replicate. You can make slower, better decisions. You can hold your price. You can say no. You can keep the team small enough that everyone knows what the product is supposed to be.

Gross margin tells you whether the business works. Runway tells you how long you have. But what neither number tells you is whether the obligations you’ve taken on will let you run the company the way it needs to be run.

Basecamp has been profitable for over twenty years. Most of the VC-funded competitors that showed up during their most vulnerable years are either gone, struggling, or locked into a growth trajectory that leaves no room to simply run a good business.

That’s the story. The weapon wasn’t the constraints themselves. It was the clarity the constraints enforced.