In 2008, a Swedish startup sent a private beta invite to a small group of Europeans. The product streamed music instantly, without downloading, from a library of millions of songs. The sound quality was good. The interface was clean. And the marginal cost of playing one more song to one more user was, for practical purposes, zero.

That last part is the whole story, if you know how to read it.

Spotify didn’t invent streaming. It didn’t own the music. It didn’t manufacture anything. What it built was a layer between rights holders and listeners, and that layer, once constructed, could serve an additional user for a cost so small it barely registers on a balance sheet. Today the company has a market capitalization that exceeds the annual revenue of the entire recorded music industry it depends on. That inversion is not an accident or a fluke of investor sentiment. It is the direct consequence of zero marginal cost economics, and understanding it is probably the most important thing anyone building or investing in software can internalize.

What Actually Happened

Spotify’s early years were genuinely difficult. The licensing negotiations with major labels were brutal. Founders Daniel Ek and Martin Lorentzon had to convince rights holders to accept a model where the per-stream payout would be fractions of a cent, arguing that volume and reduced piracy would compensate. The labels were skeptical. Several deals nearly collapsed.

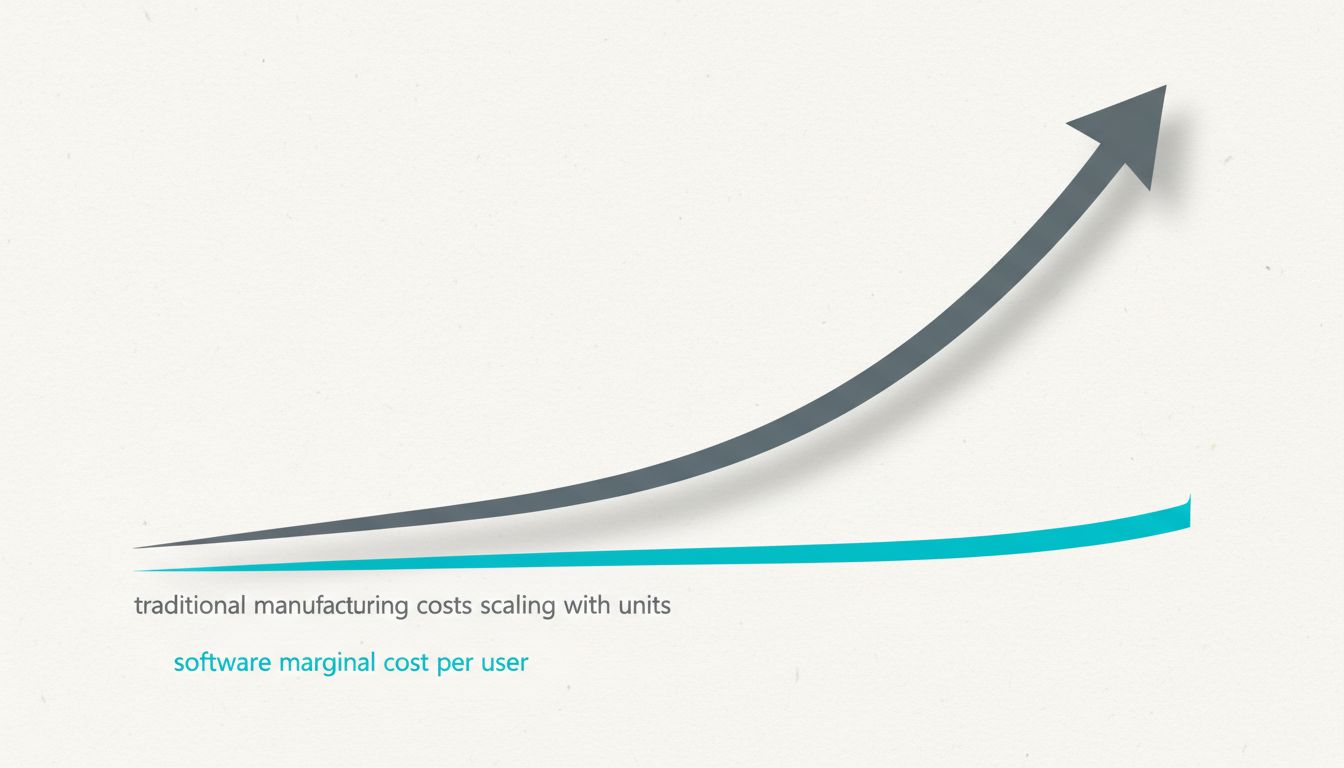

But Spotify was negotiating on the right side of the cost curve. Once those licensing deals were in place and the infrastructure was built, something remarkable happened: growth stopped being expensive in the way growth is expensive for physical businesses. A car manufacturer that doubles its output roughly doubles its production costs. Spotify adding its next ten million users mostly needed more server capacity, which is cheap and getting cheaper, and a bit more in licensing fees, which were already structured as a revenue percentage rather than a fixed per-user cost.

This is the distinction that matters. Fixed costs (building the platform, securing licenses, hiring engineers) are large. Variable costs (serving the next user) approach zero. Economists call this structure increasing returns to scale. Everyone else should call it the most powerful force in modern business.

By 2023, Spotify had over 600 million monthly active users. The incremental cost of user number 600,000,001 is not meaningfully different from user number 200,000,001. The platform was already built. The licenses were already signed. The servers scale. What this means in practice is that every new user is nearly pure margin contribution, which is why software companies at scale look so different from traditional businesses in their financials.

Why This Creates Strange Valuations

When investors value Spotify at multiples that seem disconnected from its current profitability, they are not being irrational. They are doing the math on what happens when a business with near-zero marginal costs keeps adding users. The value lives in the future, in the compounding difference between a fixed cost base and a revenue line that grows with every subscriber.

This same logic explains Microsoft, Salesforce, and Adobe. It explains why Adobe’s shift from selling boxed copies of Photoshop to subscription-based Creative Cloud was actually a bet on this economics model, not just a pricing change. Physical software copies had distribution costs. A Creative Cloud subscription has almost none. Once a user is on the platform, the cost of keeping them there is trivial compared to what they pay.

The software industry figured out something that physical product businesses still struggle with: in a zero-marginal-cost business, competition is not primarily about production efficiency. It is about who gets to the scale threshold first, because once you are there, the unit economics become nearly unbeatable.

The Dark Side of the Model

Here is what the triumphant version of this story usually skips. Zero marginal cost to the software company does not mean zero cost, full stop. It means the costs have been shifted somewhere else.

Spotify’s model shifted costs onto artists, who receive payouts that many have described as non-viable for anyone outside the top fraction of streamers. The per-stream rate is so low that a moderately successful independent musician might need hundreds of thousands of plays to earn a month’s rent. The cost did not disappear. It moved.

Similarly, social media platforms with zero marginal cost to serve content discovered that the actual costs of their model were externalized onto society in the form of attention extraction, misinformation spread, and mental health impacts. The business model looked clean internally. The balance sheet externally was a different story.

This is worth sitting with before assuming that zero-marginal-cost models are inherently virtuous. They are structurally powerful. That is different from structurally good.

What This Means If You’re Building Something

The practical lesson from Spotify’s economics is not “build a streaming service.” It is about what kind of value you are actually creating and where your costs live.

If your product’s costs scale linearly with users, you are not in the software economics game, you are in the services business, which is harder. Consulting firms, for example, are valuable but their costs grow with revenue because humans are doing the work. That is a fundamentally different ceiling.

If your product costs are mostly fixed, meaning most of the expense is in building the thing rather than in each instance of using it, then your job is to get to scale faster than competitors can replicate your fixed cost base. That is the real race. The moat in zero-marginal-cost businesses is not secrecy or patents in most cases. It is the installed user base that makes your fixed costs irrelevant per-user, while a new entrant would have to spend comparably to match your infrastructure before having a single paying customer.

This is why artificial usage limits in early platform launches are not just marketing tactics. They are about managing the ramp to the scale threshold where the economics flip in your favor.

Spotify did not win because it had better taste in music than Apple or better engineers than Google. It won in Europe first because it understood the regulatory environment, moved fast to lock in licensing deals, and got to the scale where its marginal costs became irrelevant before competitors could replicate the infrastructure investment. By the time Apple Music launched in 2015, Spotify had a six-year head start in user data, playlist infrastructure, and label relationships that would have required enormous fixed cost investment to replicate.

The product that costs almost nothing to copy, once built, is an extraordinary thing to own. The trick is surviving long enough, and spending enough up front, to build it.