The simple version

Platform companies reach margins that manufacturing businesses can’t touch because every new user makes their product better, which attracts more users, which generates more data, which makes the product better still. Competitors can copy the software. They can’t copy the data.

Why software margins are already unusually high

Before getting to data moats specifically, it helps to understand the baseline. Software costs a lot to build and nearly nothing to copy. Once a company has written the code and absorbed the fixed costs, each additional customer adds almost no marginal cost. A pharmaceutical company spends roughly the same to produce the ten-millionth pill as the first. A software company’s cost to serve its ten-millionth user is a rounding error.

This is why mature software businesses routinely report operating margins of 30 to 40 percent while industrial companies consider 10 percent acceptable. The structure of the business, not the talent of the managers, produces the difference.

But data moats push this logic further, and the mechanism is worth understanding precisely.

What a data moat actually is

A data moat is not simply having a lot of data. Storage is cheap. The moat is the feedback loop between data and product quality that a competitor cannot replicate even with unlimited capital.

Consider Google Search. Every search query, every click, every result a user ignores feeds directly back into the ranking algorithm. Google processes roughly 8.5 billion searches per day. Each one is simultaneously a product interaction and a training signal. A competitor launching a search engine today could hire identical engineers and build identical infrastructure. What they cannot buy is 25 years of revealed user preferences at that scale.

The practical consequence: Google’s search results are better because more people use Google, which makes more people use Google. This is not a metaphor. It is the mechanism by which the margin gets built.

How the margin math works

Alphabet (Google’s parent company) reported an operating margin of roughly 28 percent across its full business in 2023. But that number blends a highly profitable core with significant investment in cloud and hardware. Its advertising segment, which is where the data moat sits, runs substantially higher. Visa, which operates a different kind of data moat (transaction patterns that help it price fraud risk better than any new entrant), consistently reports net margins above 50 percent.

The 90-percent figure in the headline deserves honest context. Gross margins (revenue minus direct cost of goods) at companies like Google and Meta do approach or exceed 70 to 80 percent on their core advertising products. A few specialized data businesses, like financial data providers, can push gross margins near 90 percent. Net margins after operating expenses are lower but still extraordinary by any historical standard for businesses at scale.

The reason these margins are defensible, not just high, comes down to what economists call increasing returns to scale. Most businesses get slightly more efficient as they grow. Data-moat businesses get qualitatively better. There is a difference between cutting unit costs and actually improving the product with each new unit sold. The latter is what makes these margins sticky across decades.

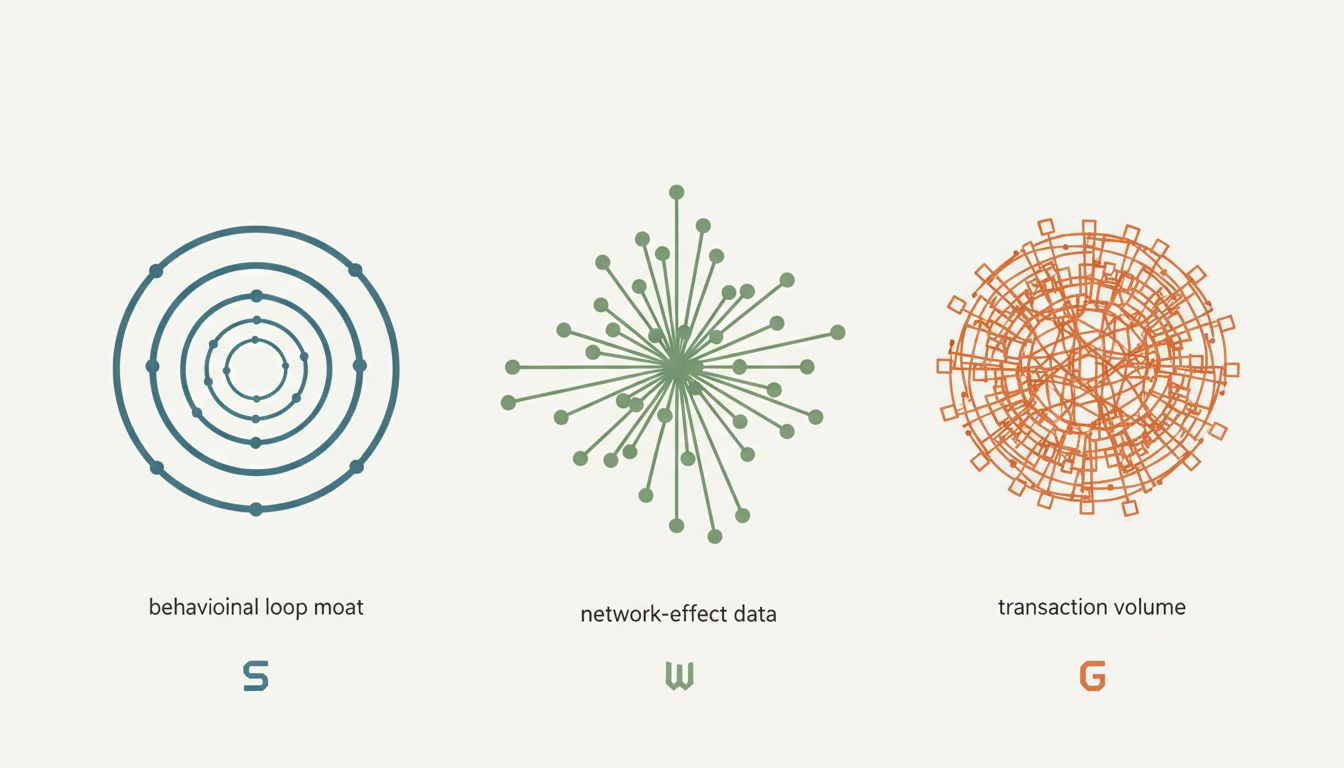

The three types of data moat

Not all data advantages are equal. The most durable ones share a specific structure.

Behavioral loops are the most powerful. Every user action improves the model, which improves the product, which generates more user actions. Spotify’s recommendation engine is a useful example: the more you listen, the better it predicts what you want to hear next, which makes you listen more. A new streaming service with an identical catalog cannot replicate a decade of listening history for 600 million users.

Network-effect data compounds differently. Each new Uber driver improves pickup times for every rider in that market. Each new Airbnb booking adds a review, a pricing data point, and a calibration signal for search ranking. The data is inseparable from the network. You cannot copy one without the other.

Proprietary transaction data is less visible but equally powerful. Visa sees roughly 200 billion transactions per year. That volume lets it build fraud models that a smaller payment network simply cannot build. It is not that Visa’s engineers are better. It is that fraud patterns only become statistically clear at a certain transaction volume, and no competitor can bootstrap their way to that threshold quickly.

Why this is harder to compete with than it looks

The instinctive response to a company with a data advantage is to go get more data. This is approximately as useful as telling a new restaurant to go get more years of experience.

The data moat problem is a cold-start problem with compounding penalties. A new entrant has worse data, which produces a worse product, which attracts fewer users, which generates less data. The gap does not stay constant while the new entrant catches up. It widens.

This is why well-funded competitors keep failing in markets with strong data moats. Microsoft’s Bing has existed since 2009 and has invested billions. Its global search market share remains around 3 percent. The engineers are capable. The capital is there. The feedback loop is not.

There are exceptions. Data moats built on a single narrow behavioral loop can be broken if user behavior shifts to a new surface. TikTok’s recommendation engine outflanked Instagram not by having more data, but by building a superior loop (video watch time as signal) on a behavior that didn’t yet have an entrenched incumbent. The moat was geography-specific: TikTok competed where Meta wasn’t yet dug in.

The practical takeaway for anyone thinking about where platform power is actually located: the margin is not a reward for building a better product. It is the compounding return on being first to close the feedback loop. Once closed, it stays closed with surprising durability, and the companies that benefit have strong incentives to keep it that way — which is a separate and increasingly important story.