Here is a number that should change how you think about your software subscriptions: analysts at Bain & Company estimate that increasing customer retention by just 5% increases profits by 25% to 95%. Platform companies understood this math long before most people did, which is why the most successful ones stopped competing on product quality years ago and started competing on exit costs instead. The distinction matters enormously, because one of those strategies builds something genuinely valuable and the other simply builds a wall.

Platform companies don’t kill competitors. They make competition impossible.

What Ecosystem Lock-in Actually Means

The term gets used loosely, but the mechanics are specific. Ecosystem lock-in occurs when the cost of switching away from a platform exceeds the cost of staying, even when a competing product is objectively superior. Those switching costs are rarely financial in a direct sense. They are usually structural: your data is in a format only the incumbent reads well, your workflows are built around the incumbent’s tools, your colleagues are already on the incumbent’s platform, and leaving means rebuilding all three simultaneously.

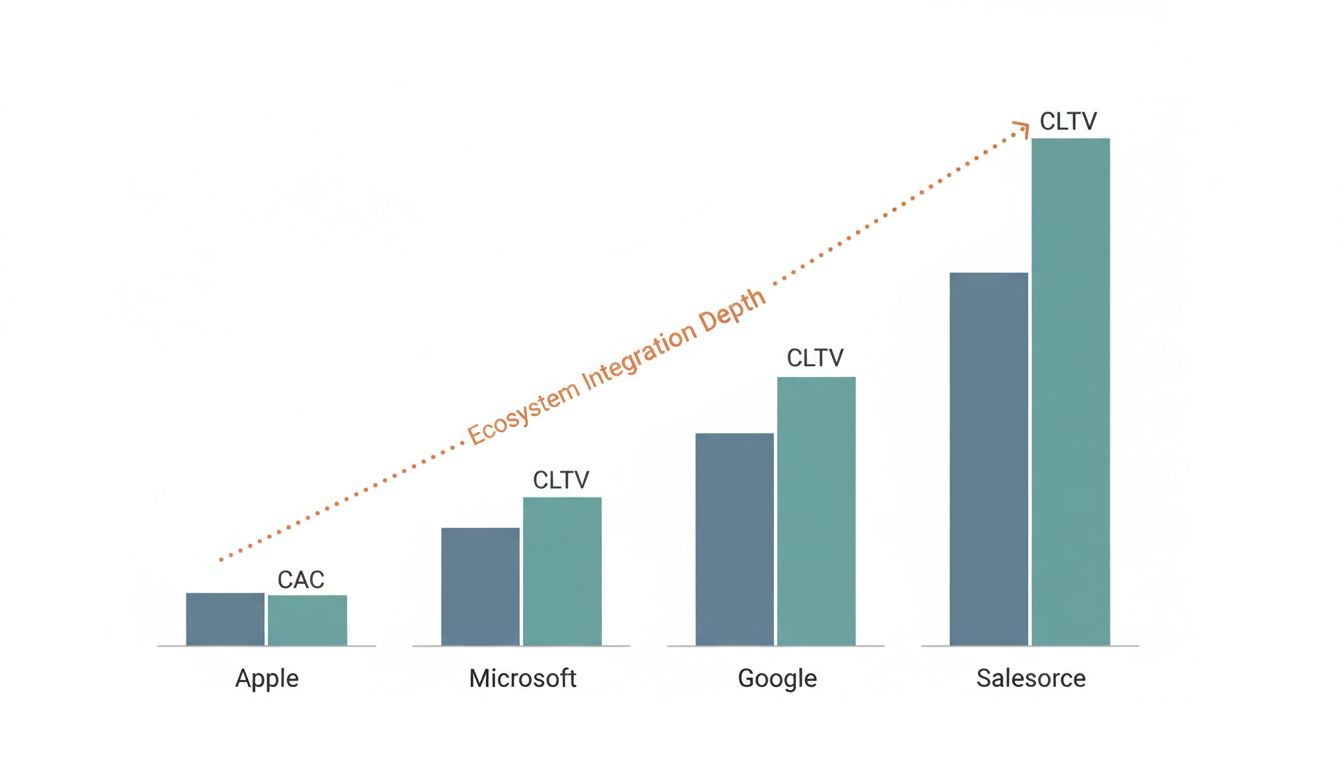

Apple is the clearest case study. A 2022 analysis by SellCell found that 91.4% of iPhone users chose another iPhone when upgrading. That retention rate is not driven primarily by hardware superiority, though Apple’s hardware is genuinely excellent. It is driven by iMessage, AirDrop, Handoff, the Apple Watch pairing requirement, and a decade of photos stored in iCloud formatted for seamless Apple device access. The switching cost is not $999 for a new phone. It is $999 plus the psychological and logistical cost of untangling an entire digital life.

Microsoft’s enterprise dominance follows the same pattern. Excel files with embedded macros, SharePoint document libraries, Teams channels woven into daily workflows, Active Directory managing authentication across thousands of enterprise machines. Each individual product is defensible on its own merits. Together, they create a gravitational field that makes the economics of switching prohibitive regardless of what competitors offer.

The Revenue Math Behind Staying Power

The 80% figure in the headline is not arbitrary. Research from multiple sources, including a widely cited McKinsey analysis of SaaS businesses, consistently shows that the majority of platform revenue comes not from new customer acquisition but from existing customers expanding their usage, renewing subscriptions, and purchasing adjacent products within the same ecosystem. In enterprise software specifically, the pattern is even more pronounced. Salesforce, ServiceNow, and Workday all report that net revenue retention (the amount existing customers spend year over year, including upsells) regularly exceeds 120%, meaning they would grow even if they never signed a single new customer.

This is why software subscriptions cost more than one-time purchases. The subscription model is not just a cash flow preference. It is the mechanism by which platform companies convert a user into a recurring revenue unit whose lifetime value compounds with every additional service they adopt. The longer a customer stays, the more they integrate, and the more they integrate, the longer they stay. It is a self-reinforcing loop designed from the beginning.

How Lock-in Gets Built, Layer by Layer

The process is rarely accidental. Platform companies architect lock-in deliberately, though they typically describe it using friendlier language like “integration” or “seamless experience.” The strategy follows a recognizable sequence.

First, offer one product at a price that is hard to refuse, often free. Google’s suite of productivity tools, AWS’s introductory pricing, Slack’s freemium tier. Second, make that product genuinely excellent so users invite others and create internal network effects. Third, launch adjacent products that work significantly better together than with competitors’ tools. Fourth, migrate user data into proprietary formats or architectures that require meaningful effort to export. Fifth, let the switching costs accumulate quietly until the idea of leaving feels more exhausting than it is worth.

This is also why tech companies build better tools for themselves than they sell to you. The internal tooling that makes platform companies operationally efficient is often the same infrastructure their customers depend on, just exposed through a different interface. Understanding that gap explains a great deal about why enterprise software often looks and feels the way it does.

Notification systems play a subtler role in this architecture than most people recognize. Platforms use alerts and pings not just to keep users informed but to reinforce daily usage habits that make the platform feel indispensable. Once checking Slack or Teams becomes a muscle-memory behavior embedded in a workday, the switching cost includes retraining an entire organization’s instincts.

Why Competitors Struggle to Break Through

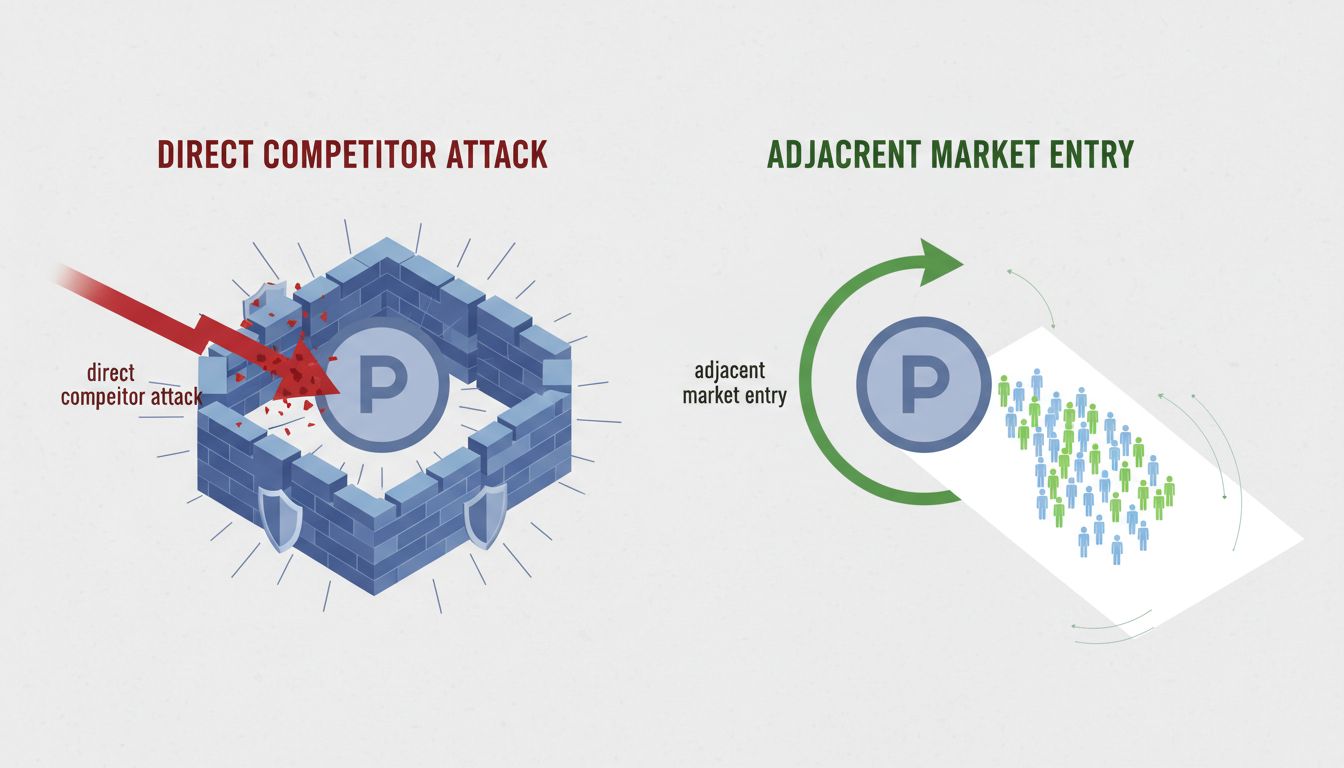

A product that is 20% better on a feature checklist rarely defeats an entrenched platform. The rational calculus is not “which tool is superior” but “is this tool superior enough to justify the cost and disruption of switching.” For most users in most contexts, the answer is no, even when the challenger is genuinely better.

This dynamic partially explains why the most successful new platform entrants tend to target users who have not yet been captured, rather than trying to pull users away from incumbents. Figma did not win by convincing Adobe users to leave Photoshop. It won by capturing designers who were beginning their careers and had no loyalty or integration debt with existing tools. By the time Adobe recognized the threat and paid $20 billion to acquire Figma (a deal later blocked by regulators), a generation of designers had already built their workflows around Figma’s collaboration model.

Similarly, the startups most likely to disrupt established platforms often begin not as direct competitors but as adjacent tools that eventually become platforms themselves. Most profitable startups started as side projects, and part of the reason is that side projects face less incumbent resistance precisely because they do not initially appear threatening.

What This Means for Anyone Building or Buying Software

For companies evaluating enterprise software, the most important question is not what a platform costs today but what it will cost to leave in five years. Data portability, export formats, API availability, and contract terms around data ownership are not technical footnotes. They are the actual price of admission, paid in arrears.

For anyone building a platform, the lesson is that sustainable revenue does not come primarily from acquisition spending. It comes from designing genuine integration value, not artificial friction, that makes users want to stay rather than feel they have no choice. The distinction matters both ethically and strategically, because platforms built on artificial lock-in are perpetually vulnerable to regulatory scrutiny and to challengers patient enough to target the users they have not yet captured.

The companies that generate 80% of their revenue from existing ecosystems are not doing something mysterious. They are doing something very old: making themselves difficult to replace. The only question worth asking is whether that difficulty reflects genuine value or a carefully constructed exit tax.