Tech companies aren’t confused about how to make money. They’re making deliberate choices that produce losses on paper while building enormous real-world value. The confusion belongs to observers who evaluate software businesses using frameworks built for manufacturing. Here’s what’s actually happening.

1. Stock-Based Compensation Is a Real Cost That Gets Treated Like It Isn’t

When a tech company grants engineers stock options, no cash leaves the building. But that doesn’t mean the cost is fictional. Shareholders get diluted. Value transfers from existing equity holders to employees. Under GAAP accounting, this shows up as an operating expense, which is why companies like Salesforce and Snap can report strong revenue growth while showing operating losses year after year.

The sleight of hand happens when companies report “adjusted” or “non-GAAP” earnings that strip out stock-based compensation entirely, as though paying employees in equity is somehow less real than paying them in cash. At many large tech firms, stock-based compensation runs into the billions annually. Ignoring it isn’t analysis. It’s wishful reading.

2. Growth Spending Gets Booked as a Loss, Even When It’s an Investment

Under standard accounting rules, most operating expenses hit the income statement immediately. When Uber spends heavily on driver subsidies and rider discounts to capture a new city, that spending reduces this quarter’s profit. But the value created, a dominant position in a market that will generate revenue for years, doesn’t appear on the balance sheet at all.

This creates a structural mismatch. Software companies that are aggressively expanding look financially worse than they actually are, because accounting rules weren’t designed for businesses where customer acquisition today pays off over a decade-long subscription relationship. The loss isn’t evidence of failure. It’s often evidence of rational investment with a delayed return.

3. Deferred Revenue Inflates the Gap Between Cash and Reported Earnings

When a company sells a two-year software contract for $240,000 upfront, it collects all the cash on day one. But it can only recognize $10,000 in revenue per month as it delivers the service. This is deferred revenue, a liability on the balance sheet representing money received but not yet “earned” under accounting rules.

The practical result is that a company can be cash-flow positive and profitable in any intuitive sense while reporting a loss because it’s growing its deferred revenue balance faster than it’s recognizing income. Salesforce built much of its early reputation on this dynamic. The business was fundamentally healthy while the reported financials looked strained. Investors who understood the distinction made money. Those who didn’t were confused by the wrong numbers.

4. Research and Development Gets Expensed, Not Capitalized

If a manufacturing company builds a factory, the cost goes on the balance sheet as an asset and depreciates over many years. If a software company builds a product, most of those engineering costs hit the income statement immediately as R&D expense, reducing profit in the year they’re incurred regardless of how long that product will generate revenue.

This asymmetry means that the more aggressively a tech company invests in its future, the worse its current profitability looks. A company spending 40 percent of revenue on R&D is making a bet on future products, not burning money irresponsibly. But the income statement treats both scenarios identically. This is partly why tech companies are valued on revenue multiples and future cash flow projections rather than current earnings, which often tell you almost nothing useful.

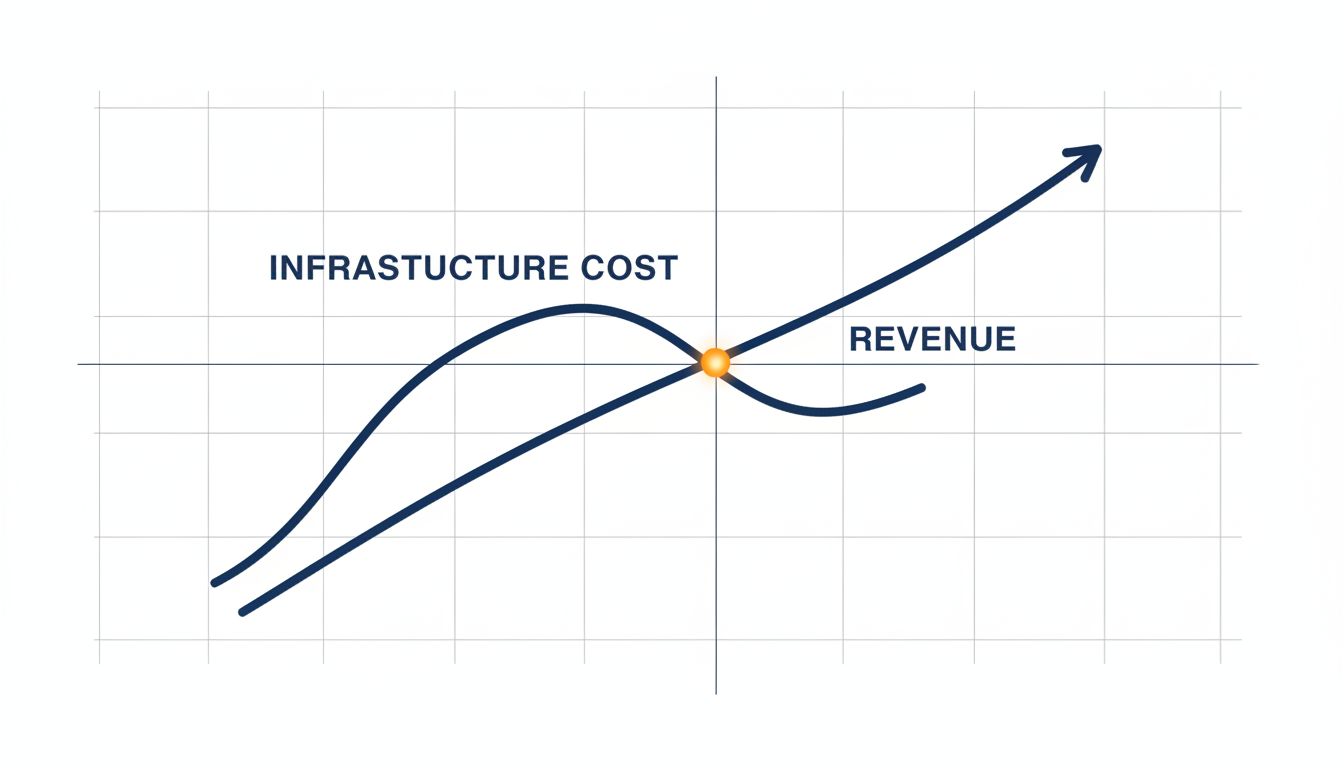

5. Infrastructure Costs Scale Ahead of Revenue, by Design

Cloud infrastructure has to be built before customers arrive. A company launching a new data product can’t wait until it has enough users to justify server capacity. It buys capacity in advance, incurs the cost immediately, and watches revenue catch up over the following quarters or years. During that catch-up period, the financials look terrible.

This is especially visible in AI infrastructure right now, where companies are spending at a scale that won’t be justified by current revenue for years, if ever. The spending is a calculated bet that the infrastructure advantage compounds over time. Whether that bet pays off is genuinely uncertain. But the loss itself isn’t evidence that the bet is wrong, only that the future is still pending.

6. Tax Strategy Keeps Reported Profits Low on Purpose

For companies that do turn a profit, there are structural incentives to minimize reported income in high-tax jurisdictions. Transfer pricing, intellectual property licensing arrangements routed through low-tax territories, and deferred tax assets all work to reduce the taxable income that shows up on financial statements. The result is that a company can generate substantial economic value and report minimal profit simultaneously, not because the business is failing, but because the tax optimization is working.

Apple, Google, and Meta have all faced scrutiny over exactly these arrangements. The point isn’t that they’re doing anything illegal. The point is that “profit” as reported and “value created” are different quantities, and conflating them produces consistently wrong conclusions about which tech businesses are actually succeeding.

The honest takeaway is that reported losses in tech are often signals worth decoding rather than reasons to panic or dismiss. Understanding what those numbers actually represent is the baseline for having any useful opinion about these companies at all.