The Profit That Wasn’t There

In 2016, the European Commission ordered Apple to pay Ireland €13 billion in back taxes, ruling that the country had given Apple illegal state aid through sweetheart tax arrangements. Ireland, the supposed beneficiary, appealed the ruling. A country fought in court to avoid receiving €13 billion.

That detail tells you almost everything about how transfer pricing works. The arrangements that produce these outcomes are not accidents or oversights. They are the product of sustained, deliberate financial engineering, built on a legitimate accounting concept that has been stretched well past its original purpose.

What Transfer Pricing Actually Is

When two unrelated companies do business, the price is set by negotiation in a real market. When two subsidiaries of the same parent company do business, no such market exists. The parent sets the price internally. That internal price is a transfer price.

The concept is straightforward and, in principle, sensible. A manufacturing subsidiary in one country sells goods to a distribution subsidiary in another. Someone has to put a number on that transaction. Tax authorities care enormously about what that number is, because it determines how much profit gets recognized in each jurisdiction, and therefore where the tax bill lands.

The governing standard, established by the OECD, is the “arm’s length principle”: the transfer price should approximate what two unrelated parties would have agreed to in an open market. In practice, applying this standard to unique assets, particularly intellectual property, involves enough judgment and ambiguity to fit a Boeing 747 through.

The Intangible Asset Problem

Physical goods have market prices. An algorithm, a brand, a software platform, or a drug patent does not. There is no market for Google’s search ranking algorithm because there is only one, and it was never sold. This is where tech companies have a structural advantage over, say, a car manufacturer.

The mechanics work roughly like this. A company develops valuable intellectual property, typically in the United States or another high-tax jurisdiction where the engineers actually work. It then transfers or licenses that IP to a subsidiary in a low-tax jurisdiction, say Ireland (12.5% corporate rate) or Luxembourg. The valuation of that IP is set at an early stage, when the IP is arguably worth little, so the transfer happens cheap. As the IP becomes enormously valuable, the royalties flow to the low-tax subsidiary. Every dollar of royalty income that gets booked in Dublin rather than California saves the parent company around 6 to 8 cents in tax.

Multiply that by the scale of Google’s ad revenue or Microsoft’s enterprise software business and the numbers become material very quickly.

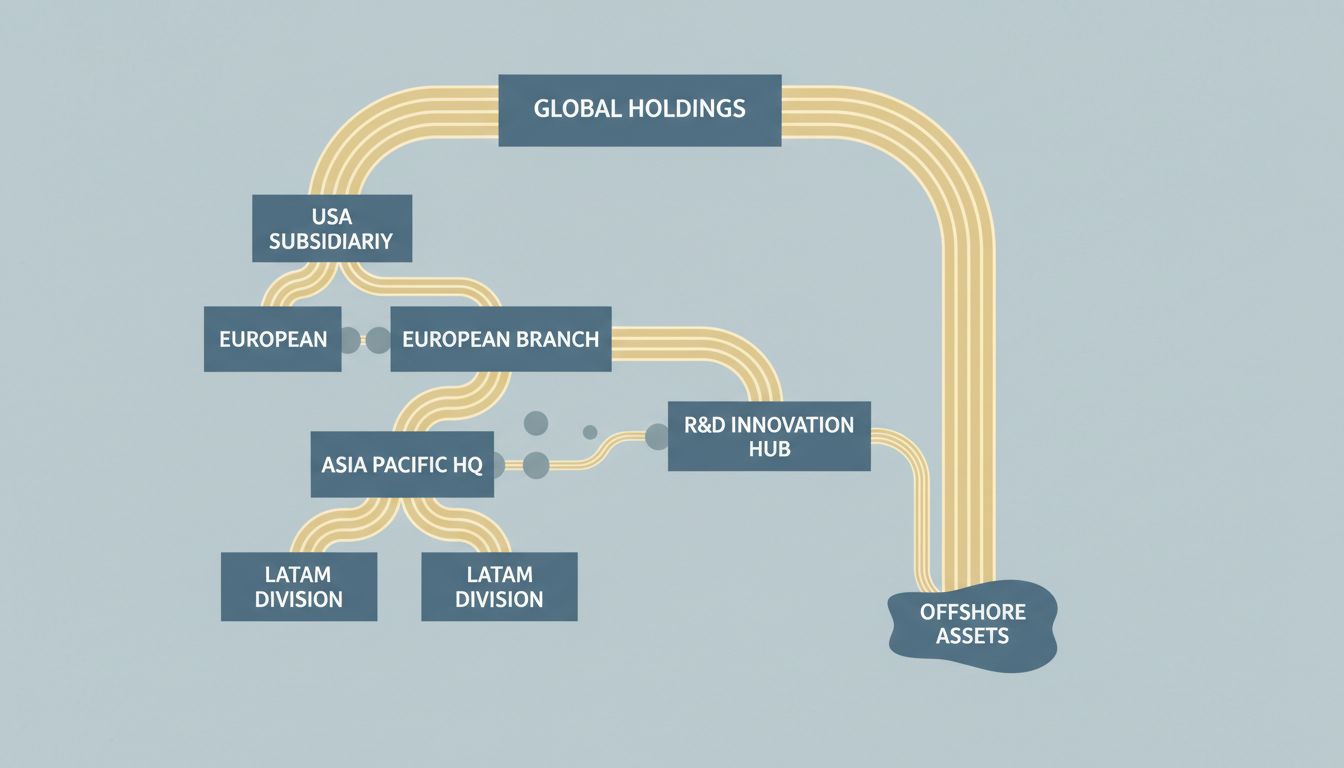

Double Irish, Dutch Sandwich, and Other Menu Items

The most documented example of transfer pricing in tech is the structure known as the Double Irish, which Google, Apple, Facebook and others used for years before Ireland agreed to phase it out in 2015 (with existing structures allowed to run until 2020).

The architecture was baroque but effective. An Irish-registered company that was tax-resident in Bermuda (exploiting a mismatch between Irish and American rules about where a company is considered resident) would hold the IP rights. A second Irish company would license the IP from the first and then sublicense it to operating companies across Europe. Royalty payments flowed up and out of the taxable Irish entity toward Bermuda, where the corporate tax rate is zero.

The Dutch Sandwich added a Netherlands holding company in the middle of this chain, exploiting Dutch rules that allowed royalty payments to pass through without withholding tax. This wasn’t regulatory arbitrage in a loose sense. It was regulatory arbitrage as a core business function, executed by teams of lawyers and accountants whose entire job was to maintain the plumbing.

Google’s parent Alphabet disclosed in SEC filings that its effective tax rate for years ran well below the U.S. statutory rate, with the gap explained partly by earnings taxed at lower foreign rates. The company’s 2017 10-K reported a tax benefit from foreign earnings that ran into billions of dollars.

Why Regulators Have Such Trouble Stopping It

The challenge for tax authorities is partly legal and partly empirical. Transfer pricing disputes come down to valuation arguments. The IRS might contend that a piece of IP was undervalued when it was transferred to a foreign subsidiary. The company’s lawyers will produce expert valuations showing it was worth exactly what was paid. Both sides can point to defensible methodologies. The litigation is expensive, slow, and uncertain.

The structural problem is that intellectual property genuinely is hard to value at early stages. Courts have limited appetite for second-guessing complex financial expert testimony. And multinationals can afford better experts than most tax authorities can retain.

There is also a coordination problem among countries. Ireland’s low corporate rate is a feature, not a bug, from the Irish government’s perspective. It attracts real investment and real employment. Tightening the rules means competing with dozens of other jurisdictions that would happily absorb the next wave of IP holding companies. The European Commission can issue rulings, but it cannot set Irish tax policy.

BEPS and the OECD’s Attempted Fix

The OECD’s Base Erosion and Profit Shifting project, launched after the 2008 financial crisis drew political attention to corporate tax avoidance, produced a package of recommendations that more than 140 countries have nominally adopted. The core idea is that profits should be taxed where economic activity occurs and value is created, not simply where IP happens to be registered.

The most consequential development is the global minimum tax, formally known as Pillar Two under the OECD framework, which came into force in many jurisdictions in 2024. It sets a 15% floor on corporate tax rates for large multinationals. The goal is to remove the incentive to shift profits to zero or near-zero tax jurisdictions.

Fifteen percent is not a high bar. The U.S. federal corporate rate is 21%, and combined with state taxes many companies face effective rates above 25%. But 15% does make Bermuda and the Cayman Islands much less attractive as profit repositories. Early evidence from countries implementing the rules suggests the structural incentive for some of the more aggressive arrangements has diminished, though multinationals are already exploring how the minimum tax interacts with credits, exemptions, and substance requirements.

The arm’s length standard itself remains intact. Transfer pricing is still legal. The dispute is over where the floor sits.

What This Looks Like on an Income Statement

For investors and analysts, the relevant number is the effective tax rate: taxes paid divided by pre-tax income. For most of the 2010s, major tech companies reported effective rates substantially below the U.S. statutory rate. Some years the gap was dramatic. Apple’s effective rate, as reported in its 10-K filings, has varied considerably depending on earnings geography and one-time repatriations.

The Tax Cuts and Jobs Act of 2017 changed the U.S. picture by lowering the statutory rate and introducing GILTI (Global Intangible Low-Taxed Income), a minimum tax specifically designed to capture foreign IP income. Tech companies lobbied extensively against GILTI’s implementation. They did not win every argument, but they won enough that the structure of the rules preserves significant planning opportunities.

What you see in tech earnings is the downstream effect of these structures. Headline revenue is large. Pre-tax income is a fraction of what it would be if all revenue were taxed where it was earned. Effective tax rates often look low relative to statutory rates. If you want to understand why, the answer usually starts with where the IP is booked. As we’ve noted in examining the accounting moves behind tech company financials, the gap between reported profit and cash generation is rarely accidental.

What This Means

Transfer pricing is not a loophole in the pejorative sense. It is a legitimate mechanism for allocating income across a corporate structure. The problem is that intellectual property makes it almost impossibly hard to apply the arm’s length standard in a way that produces results consistent with economic reality. When a company can move an asset worth billions to a low-tax jurisdiction by valuing it at millions, the standard has broken down.

The OECD’s minimum tax represents the most serious attempt to short-circuit this dynamic by taking the rate differential out of the equation rather than trying to fix the valuation problem. Whether it works depends on how consistently major economies implement it, how aggressively companies exploit carve-outs, and whether the next generation of IP structures finds angles the rules don’t cover.

For now, the honest reading is this: large tech companies pay less tax than their headline profitability suggests they should, the arrangements that produce this outcome are legal and professionally managed, and the regulatory tools to change it are incomplete. The profit didn’t disappear. It just got on a plane.