Picture a manufacturer selling a widget. Money changes hands, widget changes hands, transaction complete. The accountant books the revenue. Simple, clean, done.

Now picture Salesforce selling an enterprise CRM contract. Money changes hands on January 1st. The software doesn’t ship in a box. Access is provisioned immediately. But Salesforce doesn’t book all that revenue in January. It spreads it across twelve months, sometimes longer. The CFO is not confused. The accountant is not making an error. This is intentional, mandated, and loaded with economic logic that most people outside of finance completely miss.

The difference between those two scenarios explains more about how tech companies actually operate than almost anything else you’ll read in a quarterly earnings report.

What Revenue Recognition Actually Means (And Why It Took Accountants Decades to Figure Out)

Revenue recognition is the accounting principle that governs when a company records money as earned. The core question is not when cash arrives, but when the company has actually delivered what it promised to deliver.

For a century, this was relatively uncomplicated. You sold a physical thing, you delivered a physical thing, you recognized the revenue. The matching principle in accounting was designed around this model: expenses and revenues get recognized in the same period so that profit calculations are meaningful.

Software broke this model almost immediately. In the 1980s and 1990s, companies like Oracle and SAP were selling software licenses in massive upfront deals, recognizing all that revenue on day one, then immediately booking losses on the ongoing support obligations they’d promised. The revenue looked front-loaded and spectacular. The economics were, in many cases, terrible.

The SEC started pushing back. Accounting standard setters published new guidance specifically targeting software arrangements. Then in 2014, FASB and IASB jointly issued ASC 606, a comprehensive framework meant to finally create consistent rules across industries. The core principle: recognize revenue when (and only when) you’ve satisfied a performance obligation by transferring control of a good or service to a customer.

For software, that phrase does a lot of heavy lifting.

The Five-Step Model That Changed How Tech Companies Look on Paper

ASC 606 gives companies a five-step model: identify the contract, identify the performance obligations within it, determine the transaction price, allocate that price across the obligations, and recognize revenue as each obligation is satisfied.

Step two is where tech companies earn their complexity premium. A single enterprise software deal might contain a software license, a year of support, professional services for implementation, and training. Each of those is a separate performance obligation. Each gets a slice of the total contract price allocated to it based on standalone selling prices. Each gets recognized on its own timeline.

The software license might be recognized upfront if it’s functional (meaning the customer can use it independently). The support contract gets recognized ratably over twelve months. Professional services get recognized as hours are delivered. Training might be recognized when sessions are completed.

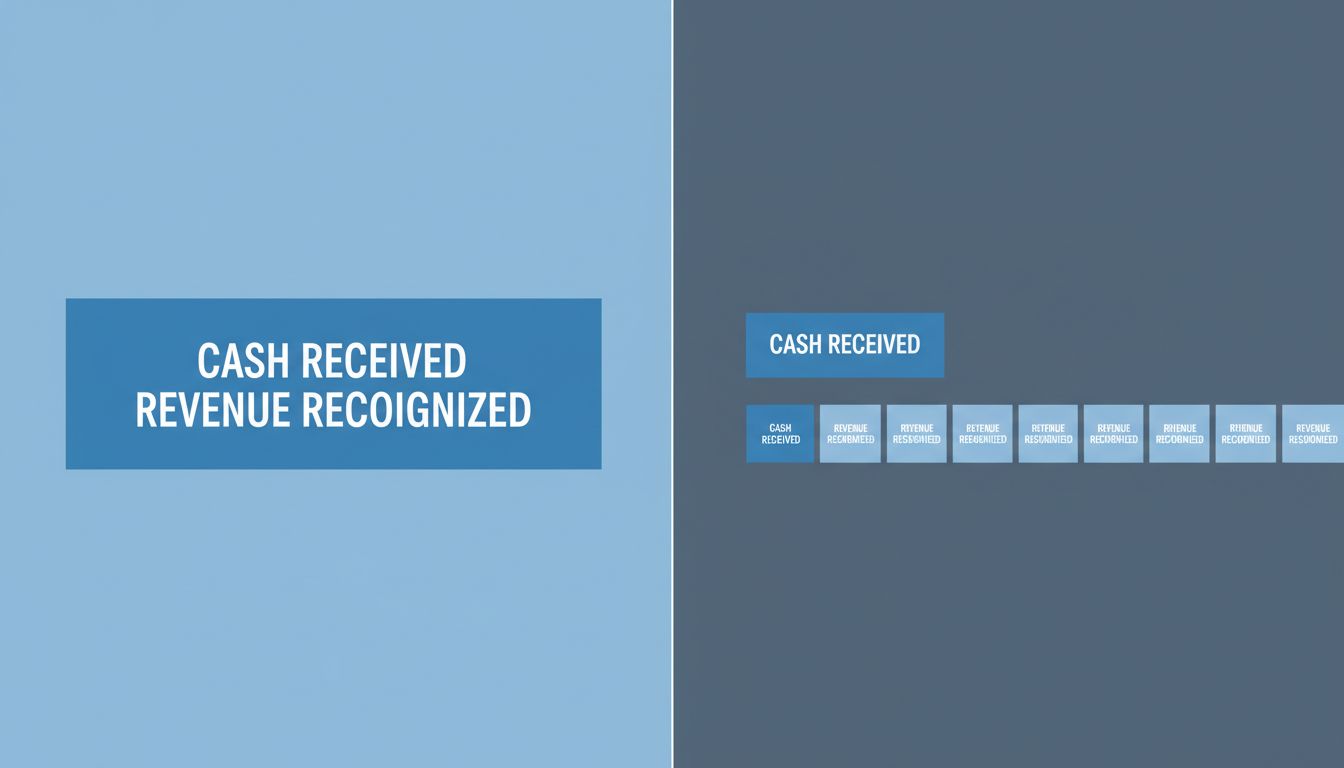

One deal, four revenue streams, four recognition schedules. This is why a company can sign a blockbuster contract in Q3 and show barely any impact in Q3 revenue.

SaaS made this even more pronounced. When you sell a subscription, you haven’t delivered anything except the right to use software during a period. That right is delivered continuously, month by month. So the revenue gets recognized month by month. Sign a three-year enterprise deal on December 1st and you recognize one month in Q4, four months in Q1, and so on. The cash might all arrive up front. The revenue recognition will span years.

Deferred Revenue Is Not a Liability, It’s a Signal

Here’s the part that trips people up when they first read a tech balance sheet. Deferred revenue sits in the liabilities section. To non-accountants, that sounds alarming. The company owes money to someone.

In a narrow technical sense, yes. Deferred revenue represents cash collected for services not yet delivered. If Salesforce takes your money on January 1st for a year of CRM access, it owes you eleven months of software access on February 1st. That obligation is real.

But here’s the thing: deferred revenue is arguably one of the most bullish signals in a software company’s financials. It means customers paid in advance. It means cash flow is running ahead of reported revenue. It means the company has visible, committed future revenue sitting on its balance sheet right now.

When Salesforce’s deferred revenue balance grows quarter over quarter, that’s not a liability growing. That’s a backlog of future revenue that will convert almost automatically, assuming customers don’t churn. Investors who understand this look at deferred revenue growth as seriously as they look at reported revenue growth. Sometimes more seriously, because deferred revenue is harder to game.

This is the inverse of how most industries work. A manufacturer with growing payables on its balance sheet might be struggling to pay suppliers. A software company with growing deferred revenue is often thriving.

Why ARR, MRR, and RPO Are Not Made-Up Metrics

Because GAAP revenue recognition for subscription businesses creates such a disconnect between economic activity and reported numbers, the industry invented its own metrics. Annual Recurring Revenue (ARR), Monthly Recurring Revenue (MRR), and Remaining Performance Obligations (RPO) exist because GAAP numbers alone tell an incomplete story.

ARR is not a GAAP metric. You will not find it defined in an accounting standard. Companies calculate it differently. It’s essentially the annualized value of current subscription contracts, and it gives investors a real-time view of the recurring revenue engine that GAAP reporting smears across time periods.

RPO is closer to GAAP-adjacent. It’s the total value of contracted but not-yet-recognized revenue. When a company reports that its RPO grew significantly year-over-year, it’s telling investors that future revenue is locked in, even if current-period revenue doesn’t yet reflect it.

Critics call these metrics ways for companies to spin bad numbers. Sometimes that’s true. The growth-at-all-costs playbook that destroyed WeWork has a quieter SaaS equivalent, and inflated ARR definitions are part of that toolkit. But the metrics themselves aren’t invented to deceive. They’re invented because GAAP was designed before subscription businesses existed at scale, and the mismatch between the two is genuine.

The Cloud Transition Made Everything Harder to Read

Microsoft’s transition from on-premise software licenses to Azure and Microsoft 365 subscriptions is one of the cleanest case studies in how revenue recognition restructuring can make a healthy company look temporarily troubled.

When Microsoft sold an on-premise Windows Server license, it recognized that revenue largely upfront. The cash and the accounting income arrived together. When it moved the same customer to Azure, the revenue started trickling in monthly, tracked against consumption. A customer spending the same amount with Microsoft per year started generating revenue that looked completely different on the income statement, even though the underlying economics were arguably better (subscription revenue being more predictable and sticky than one-time license revenue).

During major cloud transitions, reported revenue can stagnate or even decline while the underlying business is actually becoming more valuable. Analysts who understand revenue recognition saw this at Microsoft and called it correctly. Analysts who read the headline revenue number without context were confused about why a dominant company looked flat.

The same dynamic played out at Adobe when it moved Creative Suite to Creative Cloud. Reported revenue dropped initially. The stock sold off. People who understood deferred revenue and subscription economics bought that dip and were right to do so.

Hardware Is Weird Too, and That’s By Design

Apple’s revenue recognition is a case study in how product bundling creates accounting complexity even in hardware.

When Apple sells an iPhone, it’s not just selling a piece of hardware. It’s selling a device that will receive software updates, security patches, and operating system upgrades for years. The SEC pushed Apple, and eventually Apple agreed that some portion of each iPhone sale should be deferred and recognized over the device’s expected useful life, because some of what the customer paid for gets delivered in the future.

Apple also sells AppleCare, which is a multi-year service contract with multiple components. It sells iCloud subscriptions. It sells App Store access, which involves performance obligations to both developers and end users. Its revenue recognition footnotes in 10-K filings run for pages.

This is not unique to Apple. Any tech company that bundles hardware, software, and services into a single transaction has to allocate the contract price across all those components and recognize each separately. The result is that no tech company’s reported revenue in a given quarter actually represents cash collected in that quarter. Revenue reported and cash collected are two different numbers, moving in loosely correlated but distinct patterns.

What This Means

If you’re an investor, analyst, or operator trying to understand a tech company’s financial health, GAAP revenue is a starting point, not a destination. The balance sheet items around it (deferred revenue, unbilled receivables, RPO) often tell you more about trajectory than the income statement does.

If you’re inside a tech company, understanding how your contracts translate into recognized revenue matters more than most non-finance employees realize. The deal your sales team closes in December might barely register in Q4 numbers even if it was a record contract. Enterprise software contracts are structured precisely to create long-term revenue streams, and the accounting follows that structure.

The deeper truth is that revenue recognition differences aren’t arbitrary or political. They reflect something real: software, subscriptions, and bundled tech products are delivered over time, not all at once. Accounting that pretended otherwise would be less accurate, not more. The complexity exists because the underlying economics are actually complex, and that’s worth understanding before dismissing a company’s deferred revenue balance or its non-GAAP metric suite as obfuscation.

Sometimes it is obfuscation. But usually, it’s accounting catching up to a business model that didn’t exist when the rules were written.