The most elegant wealth transfer in modern capitalism doesn’t happen on Wall Street. It happens in HR onboarding packets, buried inside offer letters, framed as a gift. When a tech company hands a new engineer a grant of stock options or restricted stock units, it presents this as participation in the company’s upside. What it rarely mentions is that the employee is also absorbing a significant share of the company’s downside risk, and the company is doing so by design.

This isn’t cynicism. It’s structural. Understanding how it works requires looking at what options actually are, who benefits from their quirks, and why the arrangement persists even when workers would often be better served by higher salaries. The mechanics reveal a compensation philosophy that mirrors other counterintuitive strategies in tech, including how tech companies deliberately price premium products at a loss to capture long-term value while offloading short-term costs to partners or, in this case, employees.

What Options Actually Are (And What They Aren’t)

A stock option gives an employee the right to buy company shares at a fixed price, called the strike price, usually set at the stock’s fair market value on the grant date. If the stock rises above that price, the employee can exercise the option, buy shares at the old price, and pocket the difference. If the stock falls or stays flat, the option is worthless.

This asymmetry sounds favorable to employees. In reality, it obscures a more uncomfortable truth: the company has converted part of its labor cost into a contingent liability that may never materialize. From an accounting perspective, stock-based compensation allows companies to report lower operating expenses today by paying workers in instruments whose cost gets spread across future periods. The employee takes the risk that the payout never comes. The company books the labor as cheaper than it actually is.

For public companies, restricted stock units (RSUs) have largely replaced options, but the dynamic is similar. RSUs vest over time, creating what compensation researchers call “golden handcuffs.” The employee cannot leave without forfeiting unvested shares. Their financial wellbeing becomes tied to a single stock, a level of concentration that any financial advisor would warn against for an ordinary investment portfolio.

The Retention Mechanism Nobody Talks About

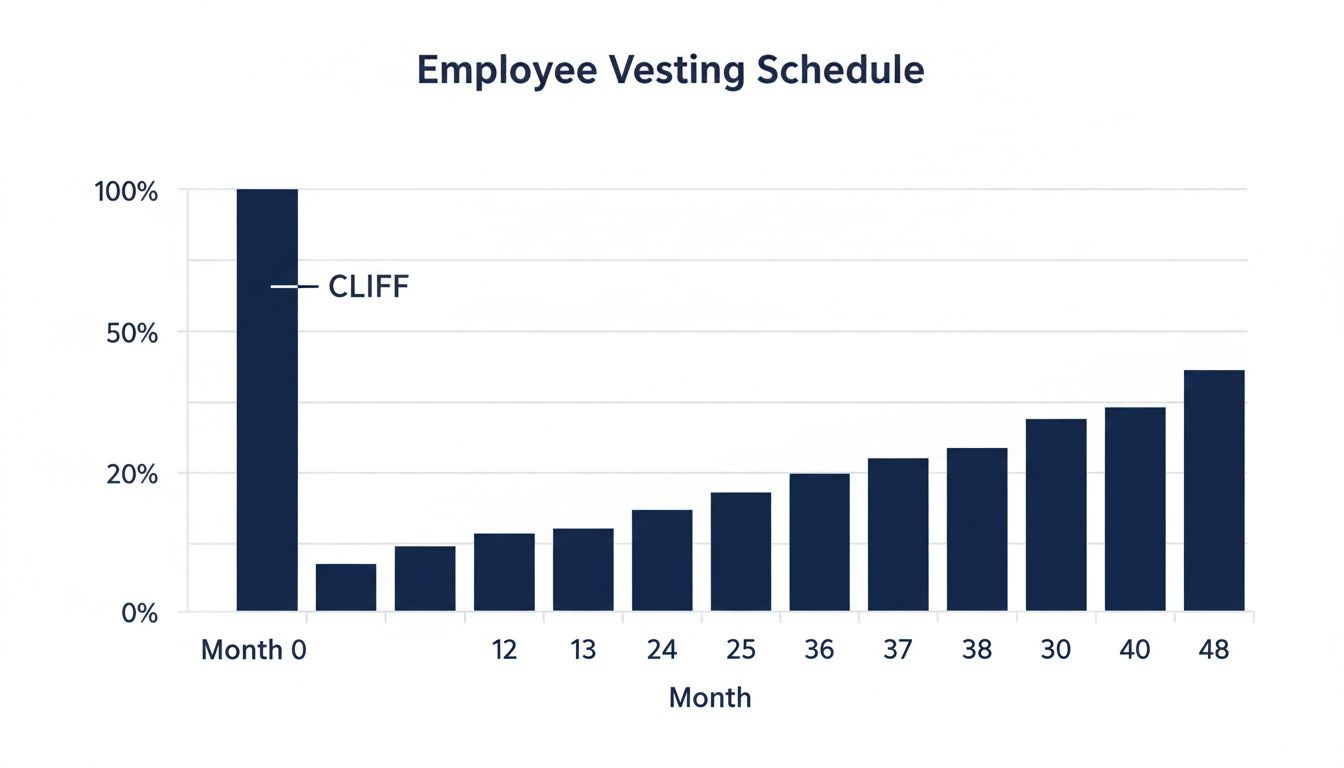

The vesting schedule is the key piece of architecture here. Most tech companies use a four-year vest with a one-year cliff, meaning an employee receives nothing for the first twelve months, then a quarter of their grant at once, then the remainder monthly or quarterly. This structure accomplishes something salary cannot: it makes leaving expensive at almost every point in the employment relationship.

At month eleven, leaving means forfeiting everything. At month thirteen, leaving means forfeiting seventy-five percent of the grant. At year three, an employee is deeply underwater on opportunity cost if they walk away. Companies have discovered that this mechanism reduces voluntary attrition far more effectively than salary increases, which are fungible and portable. A stock grant is neither.

This is a subtle form of the same logic behind early-stage startups waiting to raise their Series A. Timing is leverage. Companies structure compensation timelines to maximize their control over when and how workers make financial decisions.

The arrangement is particularly effective because workers tend to overvalue equity in their own employer. Behavioral economists call this “employer loyalty bias,” a well-documented tendency to assign higher probability to the success of one’s own company than outside evidence warrants. Companies benefit from this bias without creating it. They simply design compensation structures that let it flourish.

How Risk Gets Priced Into the Package

At large public companies, RSUs carry real but manageable risk. The stock might decline, but it’s unlikely to go to zero. The more dramatic risk transfer happens at the startup level, where options are priced at strike prices reflecting early valuations, and the path to liquidity is both uncertain and long.

Consider the math. An engineer joins a Series B startup and receives options with a strike price of five dollars per share. The company raises subsequent rounds at higher valuations. By the time of a potential IPO, the strike price still sits at five dollars, but the paper value looks enormous. Here’s what the offer letter doesn’t highlight: the employee may owe taxes on the spread between the strike price and current fair market value at exercise, a taxable event that can occur before they’ve seen a dollar of liquidity. This is the alternative minimum tax trap, and it has left workers with six-figure tax bills on stock they couldn’t sell.

More often, the company simply doesn’t reach liquidity. The National Venture Capital Association estimates that roughly three-quarters of venture-backed startups fail to return investors’ capital. For employees holding options in those companies, the compensation was always closer to a lottery ticket than a retirement account.

The Salary Trade-off Nobody Accounts For

The most consequential distortion may be the one that happens before the employee ever joins. Tech companies routinely offer below-market base salaries, justified by the “upside potential” of equity. This framing asks workers to discount a certain, portable form of compensation in exchange for an uncertain, illiquid one.

The calculation only works if the equity pays out. When it doesn’t, the employee has effectively worked for a below-market salary for years. Meanwhile, the company has preserved cash, reported lower compensation expenses, and retained the worker through a vesting schedule that made leaving costly at every stage.

This is not a conspiracy. It is a rational response by corporations to the incentives created by accounting rules, tax law, and human psychology. But it is worth naming clearly: the equity compensation system, as currently designed, systematically transfers financial risk to workers while allowing companies to present that transfer as generosity.

Sophisticated employees have begun to recognize this. Some negotiate higher base salaries explicitly in exchange for smaller equity grants. Others diversify by selling vested shares immediately rather than holding. These are rational responses, but they require a level of financial literacy that most offer letters actively discourage by emphasizing the potential upside without presenting a realistic distribution of outcomes.

Understanding this dynamic is also part of why tech founders secretly hire their harshest critics as advisors. The people most likely to see through comfortable narratives are the ones worth keeping close, whether you’re building a company or evaluating a compensation package.

What Workers Can Actually Do

The leverage in this relationship is not symmetrical, but it is not entirely absent. Workers with in-demand skills can negotiate. They can request a full breakdown of the company’s capitalization table, understand their position in the liquidation preference stack, and ask directly what percentage of the company their grant represents rather than accepting a share count that obscures dilution.

They can also treat their equity as the speculative instrument it actually is, rather than the savings account it is often presented as. That means not making financial decisions, including housing purchases or lifestyle choices, based on unvested or unrealized equity. It means understanding that the same company presenting equity as a gift has also structured it to constrain their future choices.

The equity compensation system will not be reformed by disclosure requirements or regulatory pressure anytime soon. It is too useful to too many parties, and it has been normalized through enough cycles of genuine tech wealth creation that workers continue to accept the framing. But knowing the mechanism is at least a start. The lottery ticket might win. It is still a lottery ticket.