The Simple Version

A tech company sells a product below cost, sometimes for free, until competitors run out of money and quit. Then it raises prices or monetizes in ways users never anticipated.

The Classic Version Is Older Than Silicon Valley

Grocery stores have sold milk and eggs below cost for decades to get customers through the door. The logic is straightforward: take a loss on one item, make it up across the full cart. This is a loss leader, and it only works because the store expects to profit somewhere else.

Tech companies borrowed this playbook and scaled it in ways grocery chains never could, because software has near-zero marginal cost. Printing another copy of Microsoft Word costs essentially nothing. Serving another Google search costs a fraction of a cent. That changes the math dramatically. A grocery store absorbs a fixed dollar loss on each gallon of milk. A tech company can absorb losses on millions of users simultaneously while its cost per user actually falls with scale.

The result is that in tech, loss leaders do not just attract customers. They can systematically bankrupt entire categories of competition.

Amazon’s Fulfillment Machine Was Built on Subsidized Shipping

Amazon Prime launched in 2005 at $79 per year. At that price, anyone who ordered more than a couple of packages annually came out ahead, and Amazon absorbed significant shipping costs to make it work. Analysts questioned the economics for years. Jeff Bezos said at the time that he wanted to make the decision to not join Prime feel “irrational.”

That phrase is the key. The goal was not to make Prime profitable immediately. The goal was to make competing without Prime economically untenable for other retailers. Once customers normalized free two-day shipping as a baseline expectation, any retailer that charged for shipping started to feel like a penalty. Amazon built that expectation deliberately, at a loss, for years.

Prime’s membership fees have since risen considerably (to $139 per year as of 2024), and the service now bundles video, music, and cloud storage. The original shipping subsidy purchased a behavioral norm across an entire consumer base. The subscription revenue came later.

Google Search Was Always Free, But the Product Was Never You

Google never charged users for search, which should be the first question any economics student asks. Running the infrastructure to answer billions of queries per day costs real money. Where did it come from?

The answer is advertising, but the more precise answer is that free search was itself a loss leader for building an advertising monopoly. Google needed search volume to develop the targeting data that made its ads worth more than competitors’ ads. More users meant better data, which meant better targeting, which meant higher ad prices, which funded more infrastructure, which made search better, which attracted more users. The free product was the engine that made the expensive product possible.

By the time Google had built this loop, the barrier for a competitor was not just building a good search engine. It was rebuilding a decade of behavioral data and the advertiser relationships that data supported. Microsoft has spent many billions of dollars on Bing over the years without meaningfully closing the gap, which illustrates just how durable a data moat built on free products can be.

AWS Priced Cloud Computing to Kill the Market for On-Premise Servers

Amazon Web Services launched in 2006 with prices low enough to make corporate IT departments nervous about their own infrastructure decisions. AWS could afford to price aggressively because it was already running massive server infrastructure for its retail operations. Renting out spare capacity at low margins was pure upside.

The companies that competed directly with AWS, particularly traditional server vendors and managed hosting providers, faced a structural problem. They were not competing against AWS’s margins. They were competing against Amazon’s ability to cross-subsidize cloud from retail profits, and later to accept years of below-market pricing in anticipation of long-term dominance.

AWS is now consistently one of Amazon’s most profitable divisions, generating well over $90 billion in annual revenue. The early pricing that worried analysts was not an error. It was an investment in killing off the competitive alternatives before they could reach scale. Platform economics reinforce this advantage in ways that compound over time.

The Regulatory Problem Is That the Harm Happens After the Competition Disappears

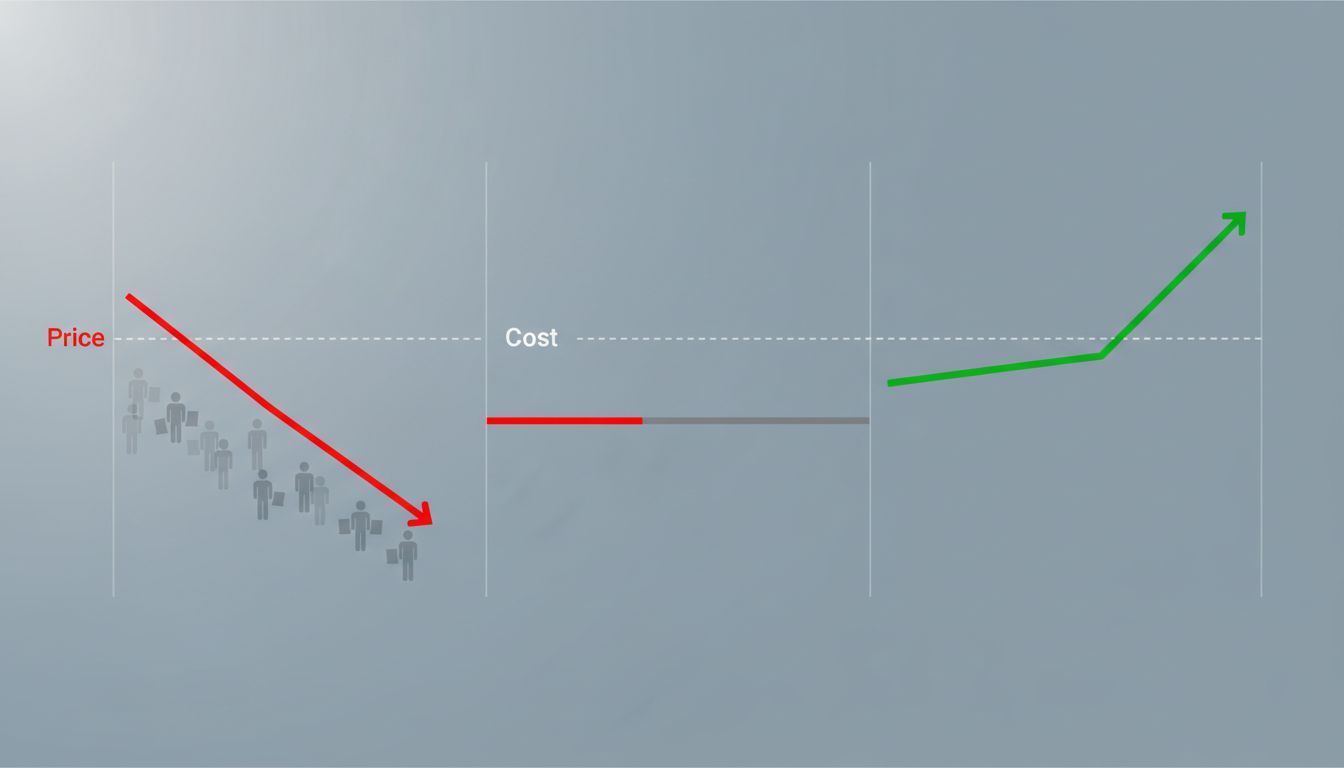

Antitrust law, particularly in the United States, was built around a simple intuition: if prices are low, consumers are not being harmed. Low prices are the point of competition. This created a genuine problem for regulators trying to police tech company behavior, because the loss leader phase of any of these strategies looks fine by traditional consumer welfare measures. Prices are low. Users are getting services for free. What is the harm?

The harm is future tense. It materializes when competition is gone and the company that spent years at a loss begins recapturing its investment. By that point, the competitive alternatives have often closed, the talent has dispersed, and rebuilding takes years. Users who “benefited” from free services discover that the price was paid in the form of reduced future choice.

This is why the FTC’s antitrust cases against Amazon and Google, whatever their outcomes, face such a difficult evidentiary challenge. The behavior regulators want to challenge happened years before the harm they can point to today.

The Pattern Is Consistent Enough to Be a Playbook

Stage one: identify a market where scale produces compounding advantages (search data, logistics networks, cloud infrastructure). Stage two: price below cost long enough to exhaust competitors or prevent new ones from forming. Stage three: once the market is captured, monetize through adjacent services, subscription fees, advertising, or pricing power that was impossible earlier.

This is not a conspiracy theory. It is a rational strategy for any company with sufficient capital and a long investment horizon. The companies doing it are not hiding the logic. Amazon has said for years that it operates on thin margins by design, investing in customer acquisition. Google’s founders wrote in their original IPO filing that they intended to manage the company for the long term, accepting short-term losses for long-term gains.

What is worth noting is that this strategy is largely unavailable to startups, because it requires the ability to lose money at scale for years without running out of capital. It favors incumbents with diverse revenue streams or access to patient capital. The companies that can afford to purchase a market through sustained losses are exactly the companies most likely to already dominate adjacent ones.