The five largest U.S. technology companies, Apple, Microsoft, Alphabet, Meta, and Nvidia, collectively authorized more than $300 billion in share buybacks in 2023 alone. Apple has repurchased more than $600 billion of its own shares over the past decade, a figure that dwarfs the GDP of many countries. Critics frame this as executives choosing financial manipulation over genuine investment. That framing is mostly wrong, and understanding why tells you more about how mature technology businesses actually work than any earnings call ever will.

1. The Honest Problem Is That They Have Run Out of Good Places to Invest

The standard critique of buybacks assumes companies are choosing them over productive investment. But the real question is whether productive investment opportunities exist at the scale the cash demands. Apple generates roughly $100 billion in free cash flow per year. There is no acquisition target, no R&D program, no capital expenditure plan that can responsibly absorb that volume of cash while generating returns above the company’s cost of capital.

When a company earns a 30% return on invested capital and cannot find new investments that clear even a 10% hurdle, returning cash to shareholders is not financial laziness. It is the correct decision. The failure mode, which investors should fear more than buybacks, is deploying that cash into acquisitions or expansion programs that destroy value just to appear busy. History is littered with tech companies that did exactly that.

2. Buybacks Are a Tax-Efficient Substitute for Dividends

When a company pays a dividend, shareholders pay income tax on it immediately. When a company buys back stock, the remaining shareholders own a slightly larger slice of the business, and they only pay tax when they sell. For long-term shareholders, including the pension funds and index funds that own most of these companies, that deferral has real economic value.

This is not a loophole. Congress has known about this dynamic for decades and has periodically adjusted the rules around it. The 1% excise tax on buybacks introduced in the Inflation Reduction Act of 2022 was a direct acknowledgment that the tax treatment difference exists and matters. Executives choosing buybacks over dividends are not doing anything exotic. They are selecting the more tax-efficient mechanism for returning capital, which is precisely what their fiduciary duty requires.

3. Buybacks Are a Signal, Not Always the Message Critics Think

When a company buys its own stock, management is implicitly saying they believe the stock is worth more than the current market price. That can be self-serving. But it can also be accurate. Apple’s buyback program, initiated aggressively after 2013 under pressure from activist investor Carl Icahn, preceded a period of substantial stock appreciation. The repurchases were not a substitute for innovation; the iPhone business was compounding steadily throughout.

The signal breaks down when companies borrow to fund buybacks, which many have done in low interest rate environments. A company that takes on debt to buy its own shares is not expressing confidence in its future, it is making a leveraged bet on its current valuation. That version of the strategy does carry meaningful risk, particularly as rates rise. Investors should distinguish between companies repurchasing from genuine excess cash and those engineering their capital structure to prop up per-share metrics.

4. Earnings Per Share Math Explains More Behavior Than Any Strategic Vision Statement

Reducing the share count raises earnings per share even if total earnings stay flat. Executives whose compensation is tied to EPS growth have a direct financial incentive to pursue buybacks regardless of other considerations. This is the cynical version of the argument, and it is not entirely wrong.

Studies have found that buyback activity tends to cluster in the months before executive option grants, which would be a troubling pattern if confirmed at scale. The SEC has increased scrutiny of this timing question. The problem is not that buybacks are inherently corrupt. The problem is that compensation structures that reward per-share metrics rather than total business performance create predictable incentives to reduce the denominator instead of growing the numerator. That is a governance failure, not an indictment of the financial instrument itself.

5. The Real Alternative Was Never “Build More Products”

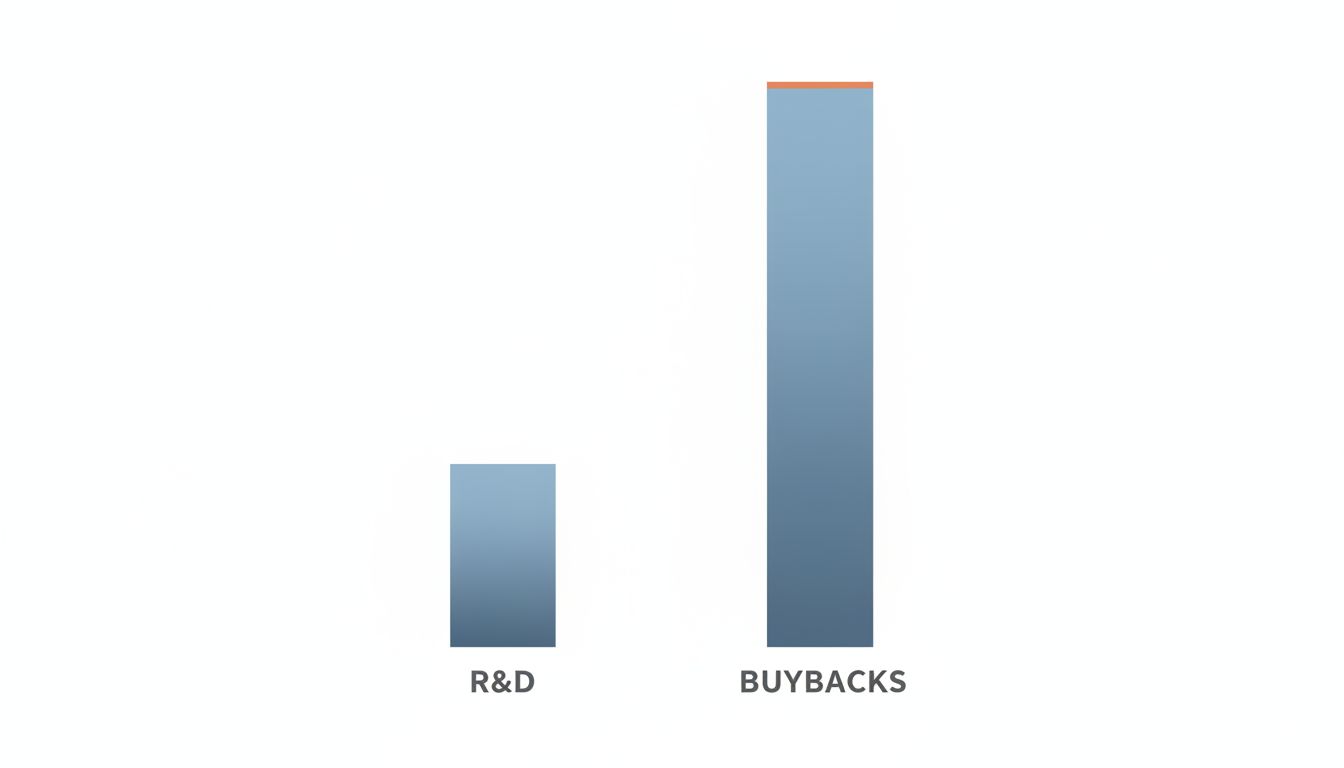

The implicit assumption behind buyback criticism is that the same billions could have funded transformative new products. This rarely holds up under examination. Apple spending $90 billion on buybacks in a given year did not prevent it from spending $26 billion on R&D in the same period. Microsoft has simultaneously run one of the most aggressive buyback programs in tech history and executed a wholesale reinvention of its cloud business. The capital constraint for innovation at these companies is almost never cash.

The actual constraints are talent, regulatory environment, competitive timing, and the organizational difficulty of running genuinely disruptive experiments inside a company optimized for predictable returns. No amount of additional cash resolves those problems. A company that cannot find its next growth driver with $26 billion in R&D is not going to find it with $116 billion.

6. When Buybacks Are Genuinely Indefensible

The defense of buybacks has limits. When companies reduce R&D, cut headcount, and defer infrastructure investment to fund repurchases, the critics are right. Several major airlines and hotel chains used buybacks to distribute essentially their entire cash reserves in the years before 2020, leaving themselves with no cushion when revenue collapsed. They then required government bailouts to survive. That sequence represents a genuine failure of capital stewardship.

The same risk applies in tech when companies face rapidly shifting competitive landscapes. A company that needed to invest heavily in AI infrastructure but instead prioritized buybacks to support its stock price would be making a dangerous trade. The test is not whether a company is buying back stock. The test is whether it is maintaining the investment levels required to stay competitive in its core markets while doing so. Companies that fail that test are not being financially sophisticated. They are consuming themselves.