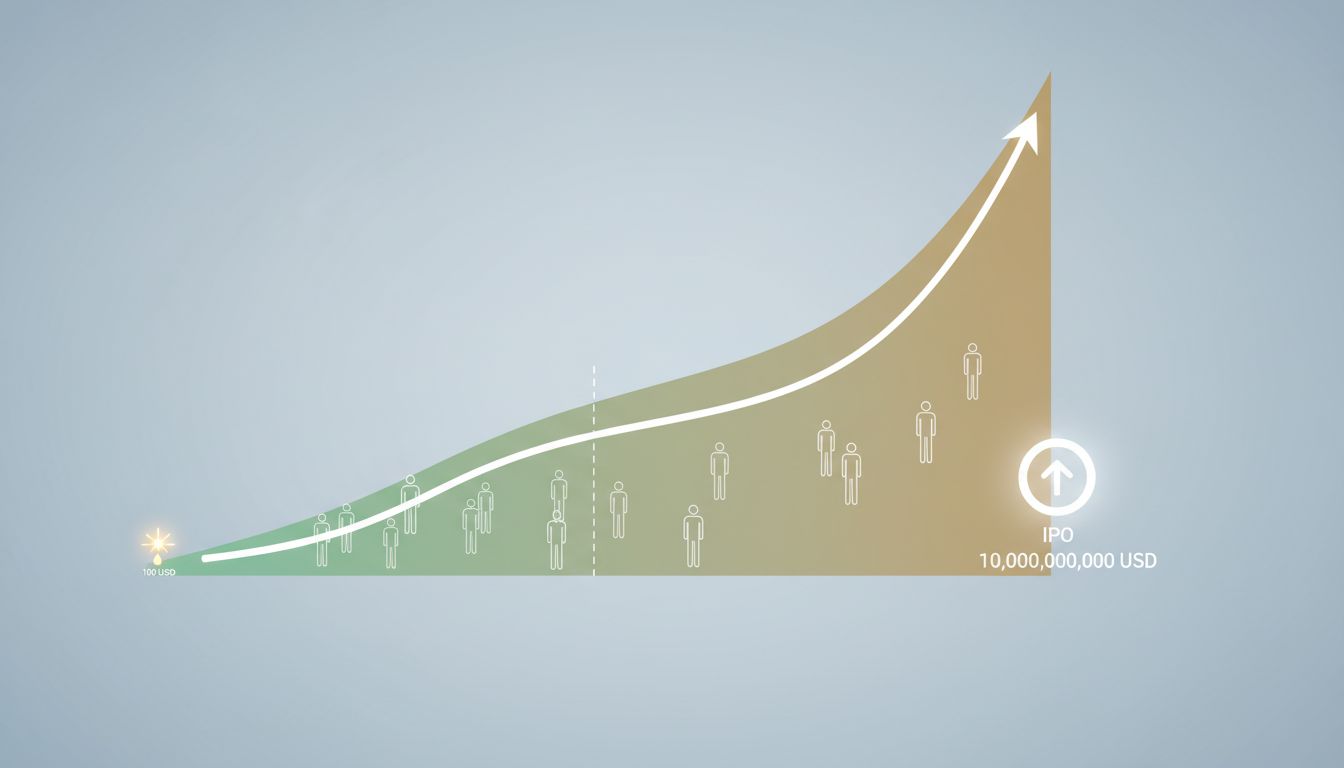

The Simple Version

Early employees get cheap stock in a company worth almost nothing. By the time the company goes public, that stock is worth a fortune. Late hires get stock in a company already valued in the billions, so there’s nowhere left for the price to go.

How Equity Actually Works at a Startup

When a company like Uber or Airbnb is founded, it’s essentially worth nothing. The founders take on enormous personal risk, so they own most of the company outright. Early employees, who also take on risk (a real salary cut, career uncertainty, the possibility the whole thing collapses), get compensated partly in stock options.

A stock option is the right to buy a share at a fixed price, called the strike price, set at the time the option is granted. If you join a startup when it’s valued at $5 million and you get options with a strike price of $0.10 per share, your options only become valuable if the company’s share price rises above $0.10. When the company goes public at, say, $50 per share, your gain is $49.90 per share. Multiply that across thousands of shares and you understand how engineers who joined Stripe or Snowflake in the early years retired in their thirties.

None of this is accidental. It is the entire point. Equity is how startups compete for talent against large companies that can pay higher salaries. The trade is explicit: accept less cash now, hold the risk of failure, and if the company wins, you win disproportionately.

The Valuation Trap That Catches Late Hires

Here is where it breaks down for employees who join later.

By the time a company reaches Series D or E funding, it has typically already been valued in the hundreds of millions or low billions. Professional investors, not employees, have priced in the expected growth. When you join as employee number 400, your options are set at a strike price reflecting that mature valuation. The low-hanging appreciation has already been captured.

Worse, most companies go public at a valuation close to their final private-market price. The IPO is not the beginning of a company’s value creation story. It is closer to the end of the high-growth phase. When Lyft went public in 2019 at around $24 billion, the venture investors and early employees who had bought in years earlier at fractions of that valuation made extraordinary returns. Employees who joined in the two years before the IPO often found that their options, by the time they vested, were worth less than expected once the stock price stalled or fell.

This is sometimes called the “late employee trap,” and it is structural, not a bug. Private markets now keep companies private far longer than they did in the 1990s and early 2000s. In that earlier era, companies would often go public within three to five years of founding, when a meaningful share of value creation still lay ahead. Today, companies routinely stay private for a decade or more. By the time ordinary investors (or late-stage employees) can participate, the extraordinary gains have already occurred in private markets, accessible only to venture funds, growth equity firms, and wealthy individuals.

Dilution Makes It Worse

Each time a startup raises a new funding round, it issues new shares. This dilutes existing shareholders, including employees. Early employees accept this dilution willingly because the company’s growing valuation more than compensates. If a round of funding cuts your ownership percentage in half but triples the company’s valuation, you are ahead.

For late employees, the math runs the other direction. They start with a smaller ownership percentage at an already-high valuation. Subsequent funding rounds dilute that position further. By the time the company IPOs, a late hire with 10,000 options might find that each share carries a strike price close to the IPO price, and that their total stake represents a vanishingly small fraction of the company.

One structural detail that compounds this: many companies issue preferred shares to investors, which come with rights and protections that common stockholders (including employees) don’t have. In a down round or a below-expectations IPO, those protections mean investors get paid out first. Employees holding common stock can end up with less than the headline numbers suggest.

The 409A Valuation and the IRS

There is a tax layer to this worth understanding.

The U.S. tax code requires private companies to periodically assess the fair market value of their common stock through an independent appraisal, called a 409A valuation. Companies use this to set strike prices for new option grants. The 409A value is typically set below the preferred share price investors pay (because common stock carries more risk and fewer protections), but it tracks the company’s growth. As a startup matures and raises more capital at higher valuations, its 409A valuation rises, and so does the strike price for new employees’ options.

This is the mechanical reason why joining early matters so much. Employee number 10 gets a strike price based on a 409A valuation of a company that barely exists. Employee number 500 gets a strike price based on a 409A valuation of a company with hundreds of millions in revenue. The IRS isn’t the villain here. It is just codifying what the market already priced in.

What Late Employees Can Actually Do

The news isn’t entirely bleak. RSUs, or restricted stock units, have largely replaced options at mature pre-IPO companies specifically because they provide guaranteed value at vesting rather than a bet on appreciation. If a company grants you RSUs worth $200,000 at a $20 billion valuation, you get something close to that value at vest even if the stock price stays flat, unlike options that can expire worthless.

Some employees negotiate for larger grant sizes to compensate for joining at a higher valuation. Secondary markets, where employees can sell private company shares before an IPO, have also grown, giving earlier employees more liquidity and reducing some of the all-or-nothing nature of the original bargain.

But none of this fully closes the gap. The fundamental asymmetry persists because it is not a policy failure. It is the mechanism by which startups attract the specific kind of talent they need early: people willing to bet on an unproven idea. That bet pays off handsomely when it works. Joining after the bet has already paid off is a different proposition entirely, and pretending otherwise is what gets late hires into trouble.