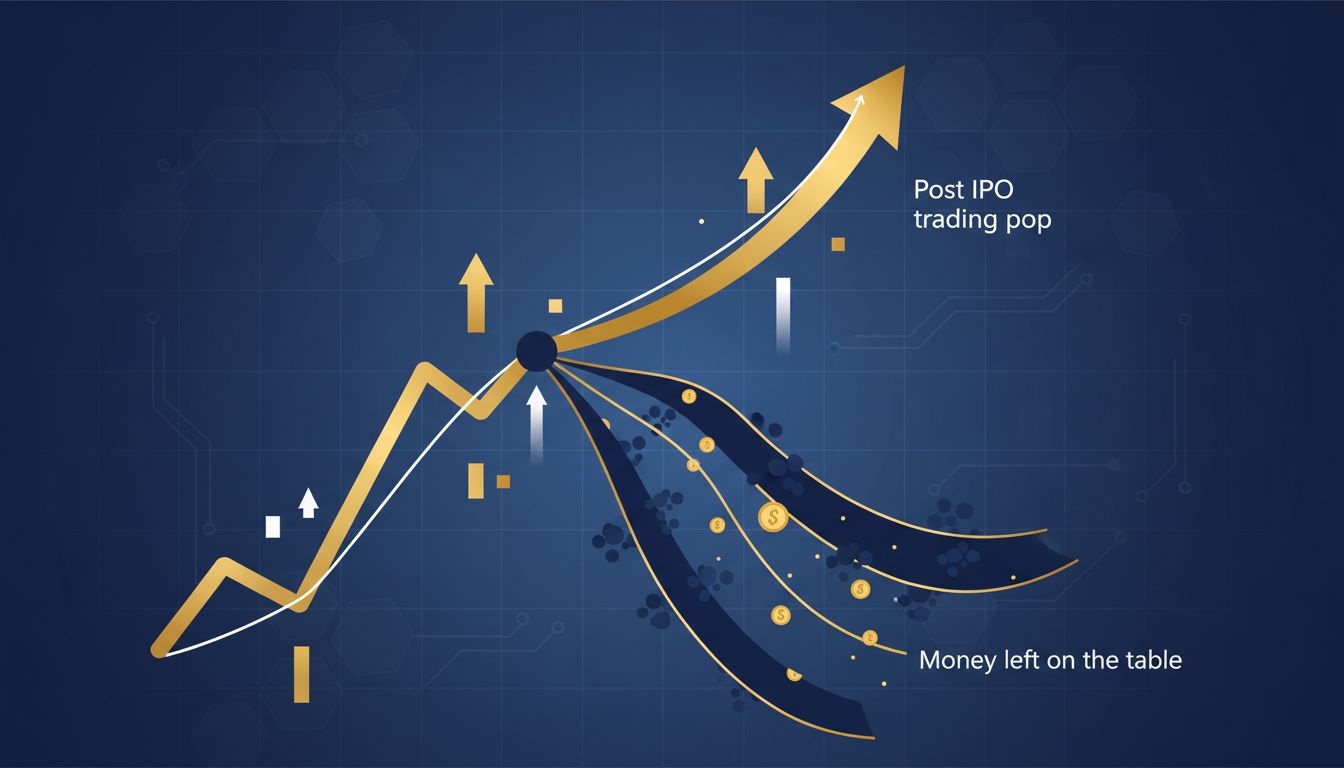

When a tech company goes public and its stock jumps 40 percent on the first day of trading, the financial press calls it a success. The founders ring the bell, the photos look great, and the narrative writes itself. What that narrative omits is the more interesting story: the company just left hundreds of millions of dollars on the table, and the people who put it there knew exactly what they were doing.

IPO underpricing is not an accident. It is a predictable, recurring feature of the way initial public offerings are structured, and it persists because it serves the people with the most control over the process.

How the Price Gets Set

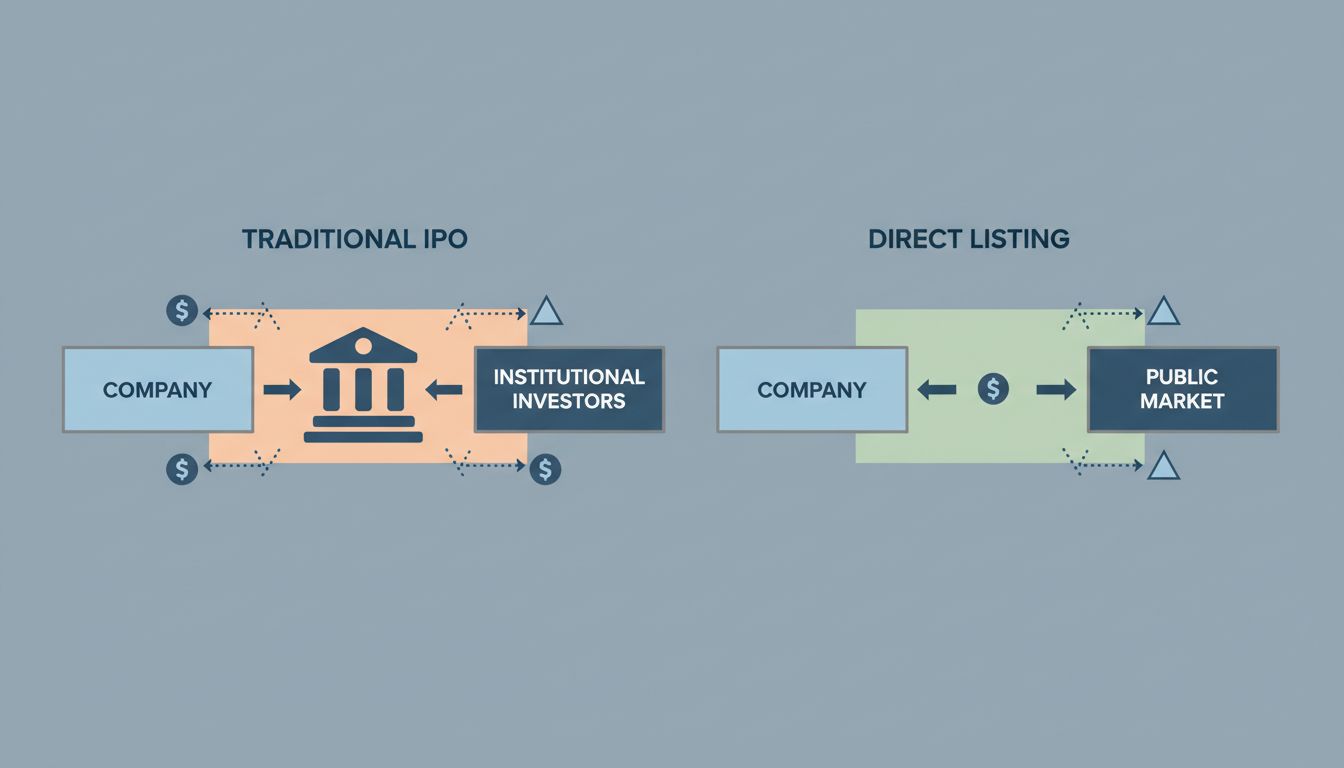

The mechanics of a traditional IPO give the underwriting banks extraordinary power. A company hires a lead bank, typically one of the large investment banks with established institutional relationships, to run the offering. That bank conducts a roadshow, pitches the company to institutional investors, collects what are called indications of interest, and then uses those signals to set the offering price.

The key word is “indications.” These are not binding commitments. Institutional investors have every incentive to signal lower demand than they actually feel, because underpricing means they buy shares at the IPO price and can sell into the pop. The bank, for its part, has relationships with those same institutional clients that extend far beyond any single offering. A bank that prices IPOs aggressively, squeezing maximum value for the issuing company, risks making its best clients unhappy. A bank that leaves money on the table keeps everyone in the room satisfied, except the company that hired it.

The conflict of interest is structural, not a matter of bad actors.

The Allocation Game

The problem compounds through share allocation. In a traditional IPO, the underwriter decides which investors receive shares at the offering price. This discretion is enormously valuable. Getting IPO allocations in hot offerings is a privilege extended to favored clients, and favored clients are, unsurprisingly, the institutional investors who generate the most trading commissions for the bank year-round.

This creates a closed loop. Banks underprice offerings, allocate shares to preferred clients, those clients profit from the pop, and the relationship deepens. The issuing company absorbs the cost. That cost is real money: a company that prices at $18 and trades to $30 on day one has effectively sold equity at a significant discount. The investors who flipped those shares captured value that belonged to the company and, by extension, to its existing shareholders.

The academic literature on this is not subtle. Researchers have documented persistent first-day returns in IPOs over decades and across markets. The pattern does not look like noise. It looks like a tax on going public, collected by intermediaries.

Why Companies Accept This

The obvious question is why companies continue to hire the same banks under the same terms if the arrangement is so clearly costly. Several forces keep the system in place.

First, there is reputational anchoring. The major investment banks have brand equity among institutional investors, and a company going public wants those investors in its cap table. The logic, not entirely wrong, is that a Goldman Sachs or Morgan Stanley imprimatur signals credibility that a smaller underwriter cannot provide. Second, company executives and early investors are often focused on getting the deal done rather than optimizing every basis point. After years of private fundraising, the IPO is the exit event, and a successful-looking pop feels better than a flat open, even if the flat open represents better economics.

Third, and most importantly, the people making the pricing decision are not the people absorbing the loss. Founders and early investors sell some shares in the offering but typically hold large positions they cannot immediately liquidate. The dilutive cost of underpricing falls on the company’s equity broadly. The executives negotiating with the bank have already made their money.

This connects to a broader pattern in tech finance, where the incentives of those running a transaction diverge sharply from the interests of the entity they represent, as explored in the dynamics of how IPOs treat employees differently depending on when they joined.

The Alternatives That Threatened the Model

The most revealing evidence that underpricing is a choice rather than a necessity came from the direct listing, pioneered by Spotify in 2018 and followed by Slack, Palantir, Coinbase, and others. In a direct listing, no new shares are sold in an offering and no bank sets an opening price. Shares are listed on an exchange and open wherever buyers and sellers agree they should.

The results challenged the conventional wisdom. Spotify opened above where analysts expected based on its last private valuation and did not exhibit the same first-day volatility that characterizes traditional IPOs. The company raised no new capital in the process (though direct listings can now include capital raises following an SEC rule change), but it also paid no underwriting discount and left no first-day gains to institutional favorites.

The reaction from the major banks was instructive. They lobbied aggressively to limit direct listings, argued that the method exposed companies to volatility and lacked “price discovery” (a claim with some merit but considerably less than was asserted), and worked to keep their clients in the traditional process. When a structural alternative appears and the incumbents fight it, you learn something about whose interests the structure was serving.

SPAC mergers, whatever their many problems, represented another pressure valve: a way to go public without handing pricing control to an underwriter. The fact that SPACs were ultimately captured by the same financial intermediaries and became their own mechanism for value extraction only reinforces the point. Capital markets are very good at finding the fee.

What This Tells You About Market Efficiency

The persistence of IPO underpricing is sometimes cited as evidence that financial markets are not efficient, that there is free money being left on sidewalks. This framing misses the point. The market is efficient at serving the people with the power to set its rules. Institutional investors who receive IPO allocations are not experiencing a market failure. They are experiencing a market that works exactly as designed for their benefit.

For the company going public, the lesson is that the price on offer from a traditional underwriter is not a market-clearing price derived from genuine price discovery. It is a negotiated outcome shaped by relationships and incentives that do not fully align with the company’s interests. The first-day pop is not validation. It is the invoice.

Sophisticated founders increasingly understand this. Whether the infrastructure exists to let them act on that understanding is a different question, and the answer, for most companies most of the time, is still no.