A few years ago, I watched a founder close a $20 million Series A for a product that had maybe $800K in annual recurring revenue and a team of eleven people. When I asked him how long the runway was, he said “about four years.” When I asked what he planned to spend it on, he got vague fast. “Hiring,” he said. “Go-to-market. We want to be ready.”

Ready for what, exactly, neither of us could say.

This is not an unusual story. It is, in fact, the template. And the standard explanation, that founders are optimistic, that VCs push bigger checks, that more runway equals more safety, misses what is actually happening. Startups raise more money than they need because the fundraise itself is a business function, not a financing event. The round is marketing. It is recruiting. It is competitive signaling. It is, in a very real sense, the product.

The Round Is a Press Release With a Wire Transfer Attached

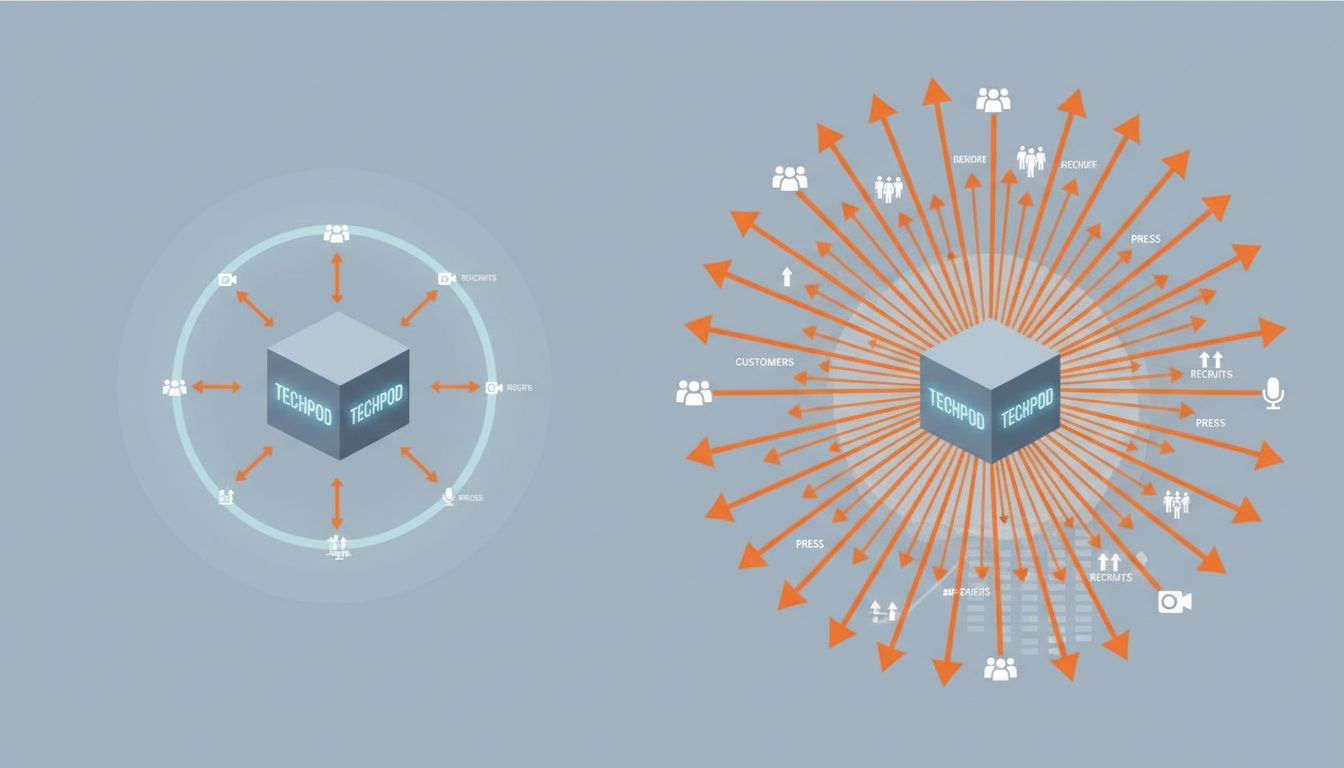

When a startup announces a $30 million raise, the number is the message. Customers who were on the fence read it and think the company is real. Enterprise procurement teams, who are allergic to signing contracts with companies that might disappear, use funding as a proxy for durability. Recruits who had two offers on the table suddenly feel more confident about the riskier one.

None of this requires the company to actually spend $30 million. It requires them to have raised it. The announcement does the work. This is why founders who don’t need the capital raise anyway, and why the round size gets negotiated upward even when the founder’s model doesn’t justify it. A $10 million raise and a $30 million raise have different effects on the market, and both founders know it.

This is also why announced round sizes sometimes bear only a loose relationship to the capital actually deployed. The signal matters more than the cash.

Hiring Good People Is Competitive, and Money Is a Credibility Token

The best engineers have options. A lot of them. And when a talented senior engineer is choosing between a stable job at a large company and a startup with eighteen months of runway and a prototype, the answer is usually no. Raise $25 million and suddenly the calculus shifts. Not because the engineer will get paid more (startup comp is complicated), but because the company now looks like a real bet. The capital is social proof.

Founders understand this intuitively. They are not raising to cover next year’s salaries. They are raising to get the kind of people who make next year’s salaries worth paying. The actual spending is secondary to what the raise communicates about the company’s trajectory.

Over-Raising Is Insurance Against a Market That Closes Without Warning

The 2021-to-2022 funding environment should have taught everyone this lesson permanently. Companies that raised aggressively in 2021, even at valuations that seemed irrational, bought themselves time when the market seized up in 2022. Companies that raised conservatively, proud of their discipline, found themselves trying to go back to market in the worst conditions in a decade.

This is not purely defensive paranoia. Funding markets are genuinely cyclical and often correlated with macro conditions that have nothing to do with a given company’s performance. Founders who have lived through one downturn raise more in good times because they know the window closes. The excess capital is not waste. It is optionality purchased when optionality is cheap.

As we’ve noted before, the accounting strategy behind years of intentional losses is often more deliberate than it looks from the outside. Over-raising fits the same pattern: it looks irrational until you understand what problem it’s actually solving.

The VC’s Incentives Push the Same Direction

Venture capital funds make money on outcomes, not on efficient capital deployment. A VC who leads a $30 million round into a company that returns 20x has done better than one who led a $10 million round into a company that returned 20x, even if the smaller round was the “smarter” choice by any capital-efficiency metric. Bigger checks mean bigger absolute returns on winners, and winners are what carry the fund.

This means VCs often push founders to take more than they modeled for. Founders who resist are sometimes replaced by founders who don’t. The incentive structure selects for over-raising the same way it selects for every other behavior that optimizes for outcome size over outcome probability.

The Counterargument

The obvious pushback is that over-raising destroys discipline. If you have four years of runway and no pressure, you hire too many people, build features nobody asked for, and spend on brand campaigns before you have product-market fit. WeWork is the extreme version of this story, but the mild version plays out constantly.

This is true, and it matters. Some startups that refused to over-raise built more durable companies precisely because the constraint forced real decisions. Capital efficiency is not a made-up virtue.

But the argument against over-raising assumes the primary purpose of the raise is operational. If you accept that the raise is also doing market signaling, recruiting, and competitive positioning work, then “discipline” becomes a harder case to make. The question is not whether the company needs $30 million to operate. The question is whether $30 million in the bank does jobs that $10 million cannot.

For most startups in competitive markets, the honest answer is yes.

The Money Is Real, But It Is Not the Point

Founders who over-raise are not being reckless or naive. Most of them know, at some level, that they will not spend the full round on the model they presented. They are raising for a set of reasons the pitch deck does not mention: credibility, optionality, competitive positioning, and the simple fact that a bigger number changes how the market treats them.

This is not a bug in the venture ecosystem. It is a feature, and it has been for decades. The funding round stopped being purely a financing mechanism a long time ago. It became a signal, a weapon, and a recruiting tool that happens to come with money attached.

The founders who understand this raise accordingly. The ones who think they are just solving a cash flow problem are usually wrong about what problem they are actually solving.