The simple version

In most technology markets, the leader captures a disproportionate share of the profits, not just the revenue. Second place often generates a fraction of the returns despite having a meaningful fraction of the customers.

Why this feels wrong at first

Intuition says markets should divide somewhat proportionally. If two search engines split users 70-30, you might expect their economics to split roughly the same way. They don’t. The distribution of profits in winner-take-most markets routinely looks more like 95-5 than 70-30, even when the user split looks close.

This is not a coincidence or a market failure. It follows from a few structural forces that compound on each other.

The advertising premium that only the leader gets

Search advertising illustrates the mechanism cleanly. Google has held roughly 90 percent of global search market share for years. Bing, despite being a legitimate product backed by Microsoft’s resources, operates at a persistent disadvantage that goes beyond raw traffic.

Advertisers running search campaigns face a choice: spend time and money optimizing for Bing’s platform, or concentrate resources on Google where the volume is. Most choose concentration. This means Google attracts more advertiser competition for the same slots, which drives up auction prices. More competition per slot means higher revenue per query. Bing, with less advertiser competition, earns less per query even for the searches it does serve.

So Bing doesn’t just get less traffic. It gets less money per unit of traffic it does get. The revenue gap is wider than the audience gap, and the profit gap is wider still because Bing still has to maintain a full search index, data centers, and a sales organization to compete for those advertisers.

This pattern repeats across markets. The leader’s platform becomes the default target for third-party investment, integration, and optimization. Developers build for iOS first. Advertisers optimize for Google first. Merchants prioritize Amazon first. Each of these choices reinforces the leader’s data and revenue advantages.

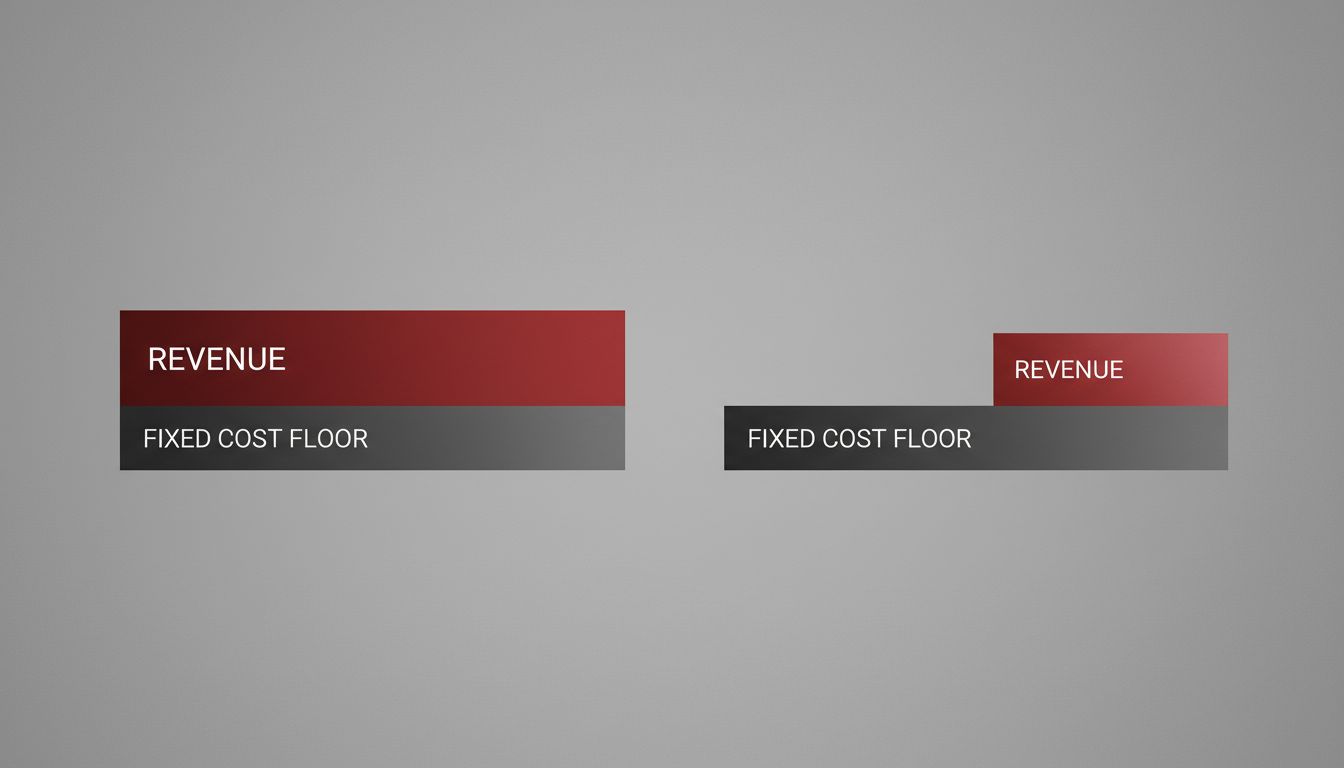

Fixed costs don’t scale with market share

Running a search engine, a smartphone operating system, or a cloud platform requires enormous fixed investment. You need the infrastructure whether you have 90 percent of the market or 10 percent. The leader amortizes those fixed costs over far more revenue. The follower carries a nearly identical cost structure against a fraction of the income.

This is why being second in a capital-intensive technology market is so economically punishing. It isn’t just that you earn less. Your margins are structurally thinner because your cost base doesn’t shrink proportionally with your market position.

Consider what this means for investment decisions. The market leader can afford to spend on R&D at a rate that the second-place player simply cannot match without operating at a loss. Over time, the leader’s product improves faster. The gap widens. Second place falls further behind not because of bad decisions, but because the economics of the position make it nearly impossible to keep pace.

Network effects as a one-way valve

Many technology products get more valuable as more people use them. This is the standard definition of a network effect, and it’s real. What’s less discussed is that network effects don’t just attract users to the leader. They actively push users away from everyone else.

Consider professional social networking. LinkedIn has over a billion members. A competitor with 100 million users isn’t offering a proportionally smaller version of the same thing. It’s offering something qualitatively different and less useful, because the value of the network is a function of who’s already there. Recruiters go where candidates are. Candidates go where recruiters are. A second-place network with half the users might have one-tenth the practical utility for a job seeker.

This is why the economics of being second only hold in markets where network effects are weak or where the market is genuinely segmented. In tightly networked markets, second place is a precarious position that tends to degrade over time, not stabilize.

The customer acquisition trap

Second-place players face a cruel dynamic in customer acquisition. To grow, they need to offer meaningful discounts, better terms, or heavier marketing to convince customers to switch from the market leader. This is expensive. The leader, by contrast, often operates as the default choice, which means lower acquisition costs per customer.

The follower spends more to acquire each customer and earns less from them (because of the margin compression described above). The return on customer acquisition is structurally worse. This is a slow bleed that shows up in burn rates and unit economics long before it shows up in market share numbers, which is part of why second-place companies can look healthier than they are for longer than they should.

Where this logic breaks down

None of this means second place is always a losing position. A few conditions change the math.

First, if the market is genuinely segmented, second place in one segment can be first place in another. Salesforce is not the most-used CRM in absolute terms if you count small businesses, but it dominates enterprise. That’s a first-place position in the segment that pays.

Second, if the leader has saturated its market, the growth story shifts. The second-place player in a mature market can sometimes generate better returns than the leader simply because there’s nowhere for the leader to go. This is a specific and unusual situation, not the general case.

Third, in markets where network effects are minimal and differentiation is strong, the structural disadvantages shrink. A boutique software tool doesn’t need to compete with the default the way a search engine does.

But in large, networked, advertising-dependent, or infrastructure-heavy technology markets, the economics of second place are punishing in ways that don’t show up clearly in market share statistics. The useful number isn’t share of users. It’s share of profit. And there, the gap between first and second is almost always far larger than the audience numbers suggest.

Understanding this changes how you evaluate competitive positions. A company at 30 percent market share isn’t halfway to success. Depending on the structure of the market, it may be close to irrelevance.