The simple version

The company that wins a tech market often has to spend so aggressively to win it that the prize barely pays off. The company in second place frequently spends less, charges more, and keeps more of what it earns.

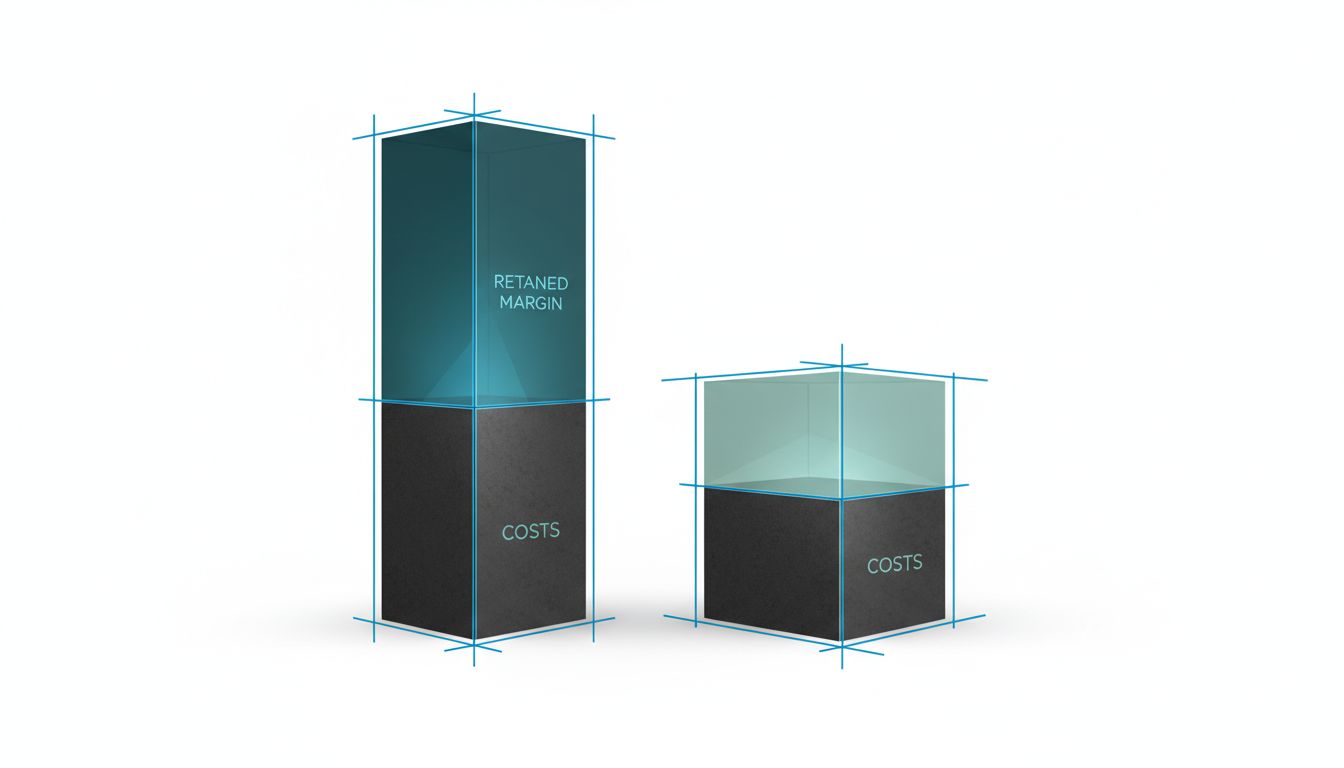

The cost of winning

Market leadership in technology is usually earned through subsidization. The leader discounts heavily to acquire customers, spends on sales teams to convert enterprise accounts, and invests in brand to maintain its position. These aren’t optional expenses once you’re at the top. They’re structural. Competitors are always just behind, ready to pick off customers who feel underserved or overcharged.

Uber spent years losing money on nearly every ride to hold market share against Lyft. Amazon Web Services priced its services aggressively enough to build a moat, then watched margins recover only gradually over time. In both cases, the leader’s financials looked worse than those of well-positioned competitors operating in adjacent or narrower niches.

The underlying math is straightforward: the more dominant your position, the more you have to defend it. Every potential customer becomes someone you feel obligated to win, even unprofitable ones.

What the second-place company gets to do differently

A company that isn’t chasing market leadership has a different set of choices available to it.

It can be selective about customers. The leader has to sell to everyone because walking away from a deal means gifting a customer to a rival. The second-place company can focus on segments where it wins easily, and decline the deals that require deep discounting or disproportionate support. This alone dramatically improves margin.

It can charge closer to what the product is actually worth. When you’re not fighting a land-grab, your pricing can reflect value rather than competitive pressure. As we’ve written before, pricing your product too low tells buyers it doesn’t work, and the market leader is often the company most trapped into underpricing.

It can also let the winner absorb the cost of market development. Educating buyers about a new category is expensive. Creating the sales playbooks, the analyst relationships, the case studies that make enterprise procurement comfortable — the market leader funds all of this, and the second-place company often benefits from it for free.

The prisoner’s dilemma that traps the leader

Here’s the structural reason this pattern repeats: the market leader almost never gets to choose to relax. Slowing down investment in customer acquisition or brand feels too risky. A CEO who says “we’re going to let our market share slip from 38% to 32% because the marginal customer isn’t profitable” will face a board revolt and a stock selloff before lunch.

So the leader keeps spending. The spending prevents the margin improvement that the business theoretically deserves. And all the while, the second-place company with 18% share is running a tighter operation, serving customers it’s actually well-suited to serve, and generating more free cash flow per dollar of revenue.

This is especially visible in enterprise software, where the category leader often has the most complex go-to-market motion: large field sales organizations, solution engineers, implementation partners, and professional services arms. The second-place competitor can serve a defined niche with a lighter model and pocket the difference.

When second place is actually a better strategic position

Not every tech market follows this pattern. In markets with strong network effects, like social media or payments infrastructure, second place can be genuinely catastrophic. If the value of the product comes from how many other people use it, being smaller is a permanent disadvantage, not a cost structure choice.

But in markets where customers buy based on fit, feature requirements, or relationship rather than on who has the most users, the second-place position can be durable and profitable. The CRM market, the data analytics market, the cloud security market — all of them sustain multiple healthy businesses precisely because no single vendor is the obvious right answer for every buyer. Switching costs lock customers in place regardless of whether they’re using the market leader or not.

The mistake is assuming that winning means leading. In a large enough market, the company that wins at being the right choice for a defined segment can outperform the company that wins at being the most-used product overall.

The investor blind spot

This is where the theory has practical consequences. Investors, analysts, and press all default to market share as the measure of who’s winning. A company with 40% market share gets valued on growth and dominance. A company with 18% market share gets discounted as a also-ran, even if its margins are better and its customer relationships are more durable.

The second-place company often looks worse by the metrics that get the most attention, and better by the metrics that actually predict long-term value creation: gross margin, net revenue retention, sales efficiency, customer lifetime value relative to acquisition cost.

This mispricing creates real opportunity. Businesses that look like they’re losing the market share race but winning the profitability race are frequently undervalued by markets that haven’t worked through the economics carefully. For investors willing to do the work, second place is sometimes the best seat in the house.