The business press loves a creation myth. The garage, the eureka moment, the lone visionary who saw what nobody else did. What gets less attention is what happened five years later, when a better-capitalized, better-informed competitor walked in, learned from every mistake the pioneer made, and took the market.

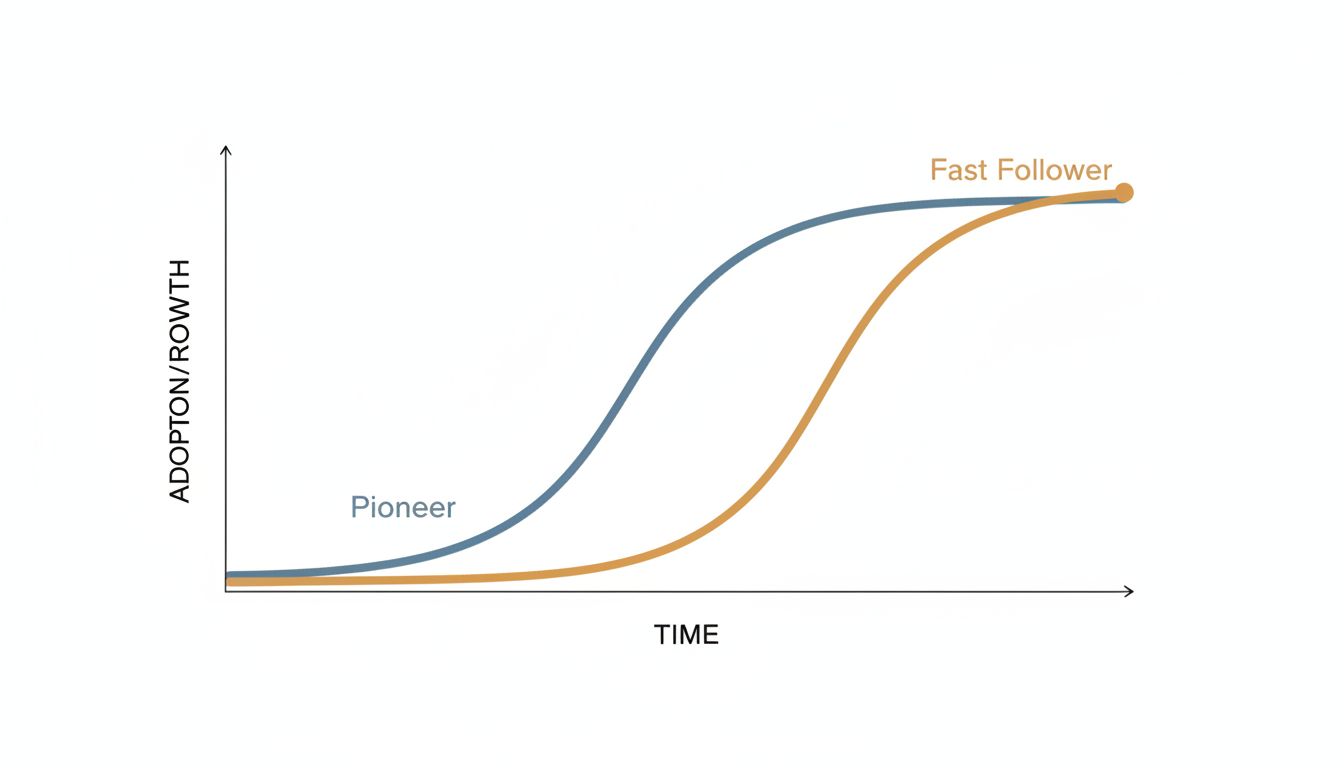

This pattern is so common in tech that economists have a name for it: the second-mover advantage. It is not a fluke. It is structural.

1. The Pioneer Pays the Education Tax

Building a new market is expensive in ways that don’t show up on a balance sheet. You have to convince customers that the problem is real, that your solution is viable, and that they should change how they work. This is not a sales problem. It is a category-creation problem, and it costs years.

Netscape built the commercial web browser and spent enormous resources educating the world about what a browser was. Microsoft waited, watched, and then bundled Internet Explorer into Windows for free. By 1999, IE held roughly 75% of the market. Netscape had done the teaching. Microsoft took the exam.

The pioneer’s marketing budget effectively subsidizes the entire category, including every competitor who enters later with customers already primed to buy.

2. Early Versions Anchor the Wrong Assumptions

When you build the first product in a category, you build it based on hypotheses. You don’t know what customers actually want because no customer has used anything like it before. So you guess. You build what seems logical. You ship.

Then you find out you were wrong about several things at once. The first version of any product in a new category is almost always a wrong version, optimized for a problem that turns out to be slightly different from the actual problem. The pioneer then faces a brutal choice: rebuild from scratch and confuse existing users, or iterate incrementally and stay stuck with the original wrong assumptions baked into the architecture.

The second mover doesn’t have this problem. They enter with real usage data, real customer complaints, and a clear picture of where the pioneer got it wrong. They can build the right thing the first time.

3. The Market Signals When It’s Ready

Timing is not just about being early. Being too early is functionally the same as being wrong. The market has to be ready: the infrastructure has to exist, the customer behavior has to shift, the willingness to pay has to emerge.

General Magic, in the early 1990s, built what was essentially a smartphone. The company included talent that later went on to found or lead major tech companies. It failed completely, not because the product was poorly conceived, but because the infrastructure (cellular networks, mobile internet, miniaturized components) didn’t exist yet to support it.

Apple watched that failure, and others like it, for more than a decade. By 2007, when the iPhone launched, broadband was ubiquitous, flash memory was cheap, cellular networks were fast enough to be useful, and consumers had already adopted digital music players. Apple didn’t invent the smartphone category. It arrived when the category was ready to be won.

4. Switching Costs Work Against the Pioneer, Not For Them

Conventional wisdom says the first company into a market builds the highest switching costs. Lock in customers early and they’ll never leave. This is sometimes true, but it requires the pioneer’s product to be good enough that customers accept it as a permanent solution rather than a temporary one.

In practice, early-market customers are the least locked in. They adopted the product before it was mature, they’ve seen its limitations up close, and they’re the most aware that better alternatives might exist. When a well-funded second mover shows up with a cleaner product, these customers are often the first to switch, because they’ve been mentally preparing for an upgrade since day one.

As switching costs become clearer over time, they tend to favor the product with the larger installed base, better integrations, and more mature ecosystem. That usually ends up being the second mover who scaled more efficiently.

5. Capital Allocation Favors the Follower

Venture capital is pattern-matching capital. Investors are cautious about funding the first company in a category because there’s no proof the market exists. The pioneer often has to bootstrap longer, raise smaller rounds, and grow more slowly than the eventual scale of the opportunity would justify.

Once the pioneer has demonstrated the market, the dynamic inverts. Now there’s proof. Investors can point to real revenue, real customers, real growth rates. A second mover can raise a larger round faster, hire more aggressively, and outspend the pioneer in sales and marketing within eighteen months of founding.

This is not theoretical. Salesforce entered the CRM market after Siebel had already spent years convincing enterprises that CRM software was worth paying for. Salesforce’s innovation was delivery model (cloud-based, subscription) not category creation. It raised capital in a market Siebel had already validated and used that capital to build faster than Siebel could defend.

6. Operational Efficiency Compounds Differently at Scale

Pioneers often build operations to match the scale of a new, uncertain market. Processes, headcount, and infrastructure get sized for a company that doesn’t quite know what it is yet. When growth comes faster than expected, these systems break in expensive ways.

Second movers can study how the pioneer scaled and build for the next level from the start. They hire people with experience in that growth stage. They pick infrastructure that won’t need to be replaced at 10x. They avoid the organizational debt that accumulates when a company grows faster than its systems.

The compounding effect is real. A company that avoids two years of operational chaos is not just two years ahead on efficiency. It’s two years ahead on cash, on hiring reputation, on customer retention, and on management bandwidth to focus on competition rather than internal firefighting.

7. The Pioneer Gets Credit in the History Books, Not in the Bank

This is the part the creation myth consistently omits. There is genuine honor in building something new, in doing the hard conceptual work, in bearing the risk of being wrong before anyone knows whether you’re wrong.

But market share and historical credit are different currencies. Xerox PARC developed the graphical user interface, the mouse, and ethernet. Apple and others commercialized them. Friendster created the social network template. Facebook monetized it. TiVo proved consumers wanted digital video recording. Comcast and cable companies made the money.

As second place often earns more than first in tech markets, the financial returns to pioneering are often weaker than the narrative suggests. The risk is higher, the timing is harder to control, and the competitive moat is shallower than it looks from the outside.

If you’re building a company, being second into a validated market with a clearly superior product is not a consolation prize. It is frequently the better business.