A founder I know raised a Series B at a $180 million valuation in 2021. Eighteen months later, her investors told her the company needed capital and the market had moved. The new round came in at $60 million. She took it, because the alternative was worse. What she didn’t fully grasp until weeks later was how thoroughly the cap table had been rearranged beneath her feet.

Down rounds are not just embarrassing press releases. They are structural events that redistribute ownership, reset incentives, and sometimes quietly transfer control. If you’re a founder who has never been through one, here is what actually happens.

1. Your Ownership Percentage Gets Compressed, Fast

When new investors come in at a lower valuation, the company issues new shares to cover their investment. Everyone who held shares before that round now owns a smaller percentage of a smaller pie. That includes you.

The math feels abstract until you run it. Say you owned 20% of the company going into the down round. After the new shares are issued, your stake might be 12% or lower, depending on the round size and any anti-dilution provisions that kick in for earlier investors. Your absolute share count hasn’t changed. Your percentage has.

This matters at exit. If the company is eventually acquired for $100 million, the difference between 20% and 12% is $8 million in your pocket. That is not an abstraction.

2. Anti-Dilution Clauses Become the Most Important Sentences in Your Old Term Sheets

Most institutional investors negotiate anti-dilution protection into their preferred stock terms. There are two main flavors: broad-based weighted average and full ratchet. The difference is enormous.

Broad-based weighted average is the standard. It adjusts the conversion price of earlier investors’ preferred stock to something between the old price and the new price, softening but not eliminating their dilution. Full ratchet is the punishing version: it reprices earlier investors’ shares all the way down to the new, lower price, which means they get issued more shares to compensate, which means common shareholders (founders, employees) absorb a disproportionate hit.

Few founders read those clauses carefully when things are going well. A down round is when you find out what you agreed to. If you have investors with full ratchet protection and a significant down round, the dilution to common shareholders can be severe enough to make the equity nearly worthless.

3. Employee Option Pools May Be Underwater, and That Affects Everyone

Options are priced at the fair market value of common stock at the time of grant. After a down round, the 409A valuation of the company typically drops, which resets what common stock is worth. Options granted at the previous high may now have a strike price above the current value of the shares they represent.

Underwant options don’t vest faster. They don’t disappear. They just stop motivating the people who hold them. An engineer who joined two years ago because her options felt meaningful now has paper that is functionally worthless unless the company not only recovers but surpasses its previous valuation. Many companies do option repricing after down rounds to keep talent from walking. That repricing is its own administrative and morale exercise.

The human cost of a down round is often most visible here. Retention gets harder precisely when execution matters most.

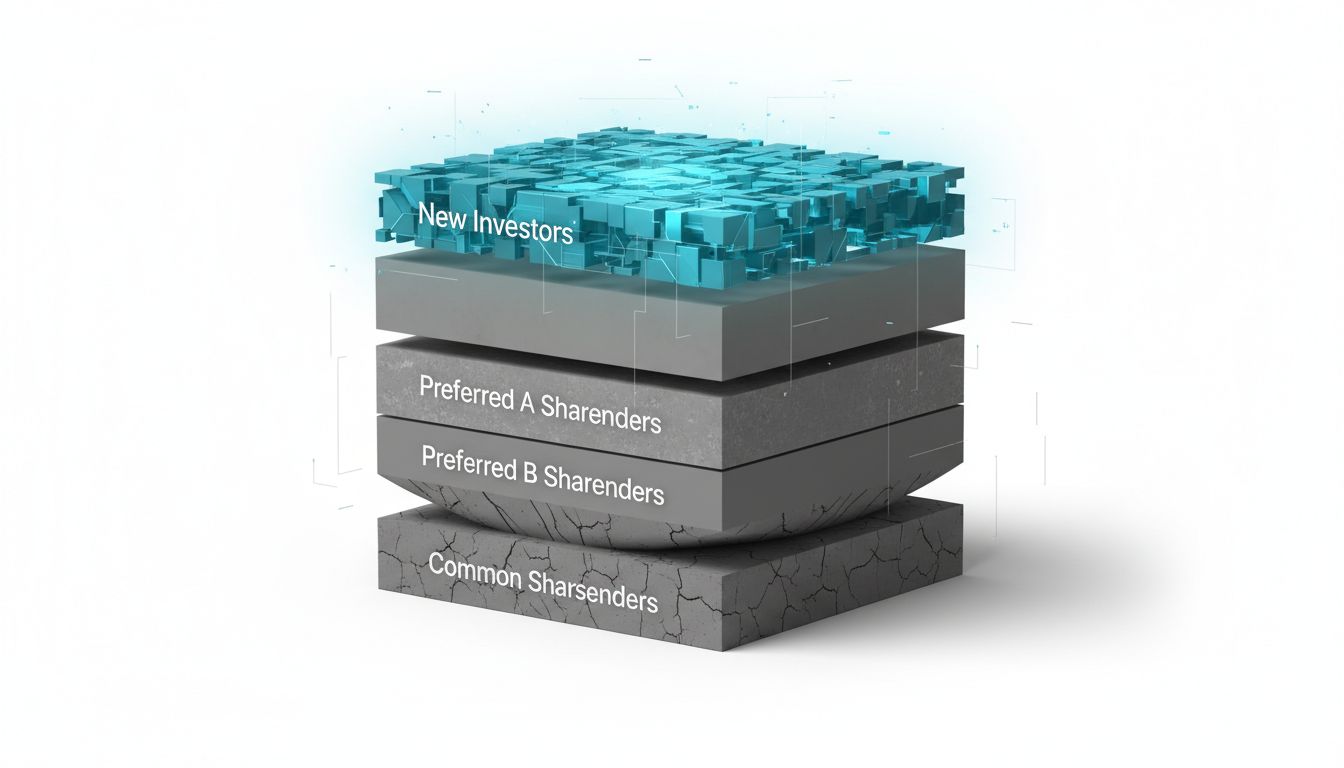

4. Liquidation Preferences Stack, and Later Investors Often Go First

Preferred shareholders typically have liquidation preferences, meaning they get paid before common shareholders in an exit. Most Series A and B term sheets include a 1x non-participating liquidation preference, which means investors get their money back first, and then common shareholders split the remainder.

In a down round, new investors almost always negotiate their own liquidation preferences at the top of the stack. This is called a senior preference, and it means they get paid before everyone who came before them. Founders and employees are common shareholders. Early-stage angels are often common or have weaker preferred terms. If the company sells for anything less than the sum of all liquidation preferences, the common shareholders get nothing.

This is not a hypothetical. Many acquisitions in distressed markets happen at prices that clear the new investors’ preferences and leave earlier investors and founders with little or nothing. The headline number of an acquisition can look respectable while the actual distribution is deeply lopsided.

5. Control Provisions May Shift Without a Board Seat Changing Hands

Down round investors often extract protective provisions that give them blocking rights over major decisions: future fundraising, acquisitions, changes to the option pool, debt issuance. These provisions don’t require a board majority to be meaningful. A single veto right over an acquisition can effectively hold a company hostage.

Founders often focus on board composition as the measure of control. That is incomplete. The actual levers of power in a cap table live in the protective provisions and voting agreements attached to preferred stock. After a down round, those provisions may have multiplied, and the new investors’ interests may not align with yours.

If you are negotiating a down round, have your lawyer go through every control provision being proposed. Some are standard. Some are aggressive. The negotiating leverage founders think they’ve lost because of the valuation drop is often still there, it just requires knowing where to push.

6. The Round Can Damage Signaling as Much as the Cap Table

A down round tells the market something. Other investors who were watching your company now have a data point. Future employees who are considering joining will find out eventually. Customers doing due diligence before a large contract will sometimes ask about it directly.

None of this is disqualifying. Many companies that took down rounds went on to strong exits. What matters is the story you can honestly tell about why the round happened and what changed. Macro conditions shifted. The business model pivoted. The market timing was wrong on the first raise. These explanations land differently than ones that suggest the business fundamentals were broken.

Founders who treat the down round as a private financial restructuring and fail to communicate clearly with their teams usually regret it. The story leaks anyway, and the version that fills the vacuum is always worse than the one you could have told.

7. The Cap Table After a Down Round Is a Negotiation, Not a Fate

The mechanics above are real, but they are not fixed. Down rounds are negotiated events, and sophisticated founders use them as opportunities to clean up terms that were poorly structured in earlier rounds. Investors who want the company to survive have an incentive to be reasonable. New investors who want motivated founders have an incentive not to wipe out all the common equity.

Some founders have used down round negotiations to collapse multiple liquidation preference stacks, simplify governance, and reprice option pools in a single transaction. It requires goodwill from existing investors and a credible path forward, but it happens.

The worst outcome is a founder who takes a down round passively, signs whatever the term sheet says, and discovers later that they restructured the company into something that no longer makes economic sense for them to run. If the deal doesn’t leave you with a reason to keep building, say so. Investors generally prefer a motivated founder with less ownership to a checked-out one with more.