The Simple Version

If your startup gets acquired for less than the total amount investors put in, the investors get paid back first. By the time everyone with a preferred claim gets their money, common stockholders, which usually means founders and employees, often get nothing.

Why This Surprises People

Picture an engineer who joined a Series B startup three years ago. She took below-market salary, vested through two grueling years of product pivots, and watched the company get acquired. The press release says the deal was for $40 million. Her friends congratulate her. Then she gets the breakdown from HR, and her payout is zero.

This is not a rare edge case. It happens in the majority of startup acquisitions, most of which never get covered because $40 million sounds like a win until you understand the capital structure underneath it.

The confusion comes from treating equity as a simple percentage of a sale price. It isn’t. The type of equity you hold, and where it sits in the payment queue, determines everything.

Preferred vs. Common: The Stack That Decides Your Fate

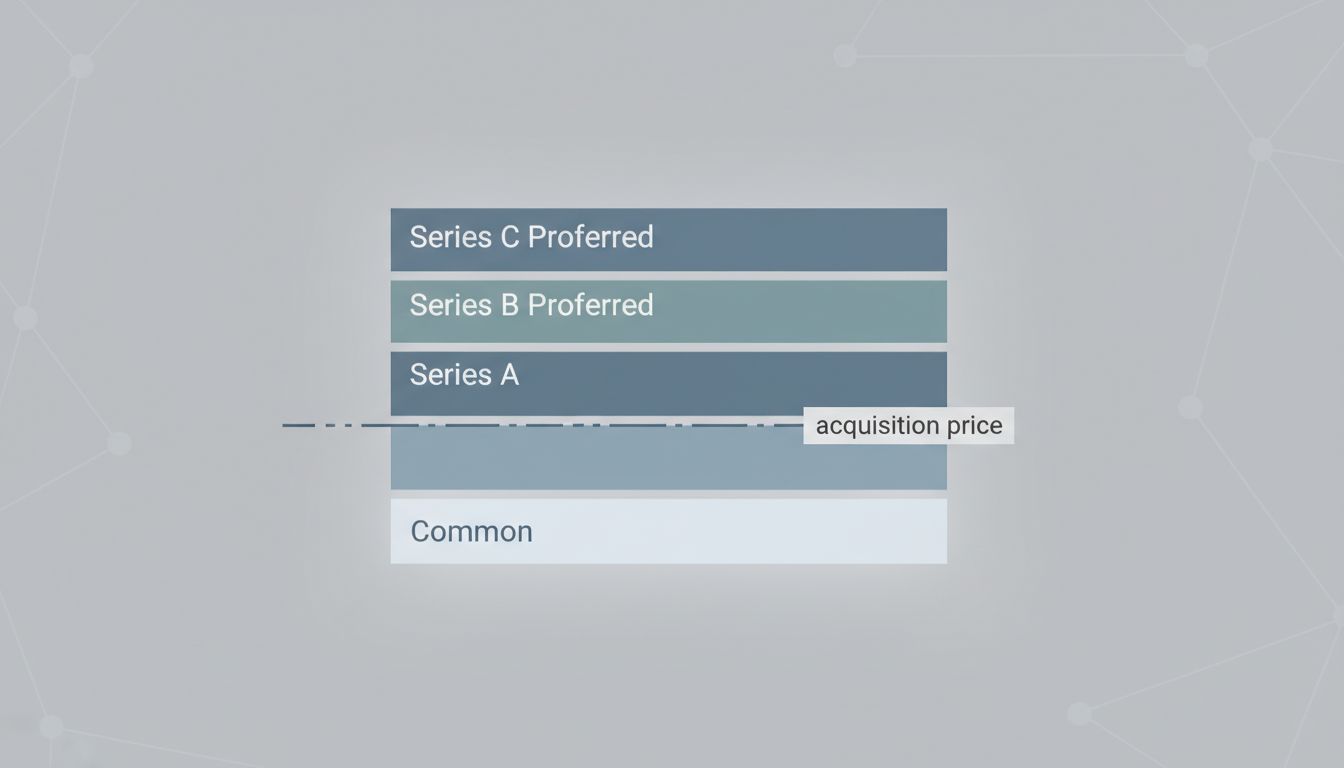

When a VC writes a check, they almost never get the same class of stock that founders and employees hold. They get preferred stock, which comes with a liquidation preference. In plain terms: preferred stockholders get paid first, up to some multiple of what they invested, before anyone holding common stock sees a dollar.

A standard 1x liquidation preference means investors get back exactly what they put in before the distribution waterfall reaches common shareholders. A 2x preference, which is more aggressive but not uncommon in later-stage or distressed rounds, means they get twice their investment back first.

So if a company raised $60 million total across multiple rounds, each round with its own liquidation preference, the acquisition price has to clear $60 million before founders and employees participate at all. If the company sold for $40 million, the entire amount goes to preferred holders, and it may not even cover the full preference stack.

Some preferred shares also come with participation rights. This means that after preferred investors get their liquidation preference back, they also convert to common and participate in the remaining proceeds alongside everyone else. Participating preferred is essentially getting paid twice. It’s more common in earlier rounds and in markets where investors have more leverage.

The Math on a Real-ish Scenario

Let’s run through a concrete case. A startup raises $80 million across four rounds: $2 million seed, $8 million Series A, $20 million Series B, and $50 million Series C. All investors have 1x non-participating liquidation preferences.

The company, unable to reach the growth targets that justified its last valuation, finds a strategic acquirer willing to pay $75 million.

That $75 million gets distributed starting at the top of the preferred stack. Series C investors get their $50 million. Series B gets $20 million. That’s $70 million gone. Series A gets their $8 million. Wait, we only have $5 million left. Series A gets $5 million, seed investors get nothing, and common shareholders get nothing.

In this scenario the option pool, which covers all employee equity grants, is common stock. Every engineer who took a salary cut for upside walked away empty.

Change one number and the picture shifts. If the acquisition price were $85 million instead of $75 million, all preferred gets paid, $5 million flows to common, and employees and founders split a small remainder. Small compared to the headline price, but not nothing.

The difference between zero and something can be $10 million in deal price, or the difference between participating and non-participating preferred, or anti-dilution provisions that protected earlier investors by effectively diluting common further when later rounds came in at lower valuations.

What Liquidation Preferences Actually Look Like in Practice

Most people signing offer letters don’t read the company’s certificate of incorporation. Even if they did, the capital structure they’re joining will change with every subsequent funding round. The terms employees see on day one don’t reflect the preferences that will be in place the day an acquisition closes.

Founders who understood this dynamic going into a Series C negotiation sometimes pushed back on participating preferred or agreed only to 1x non-participating in exchange for a slightly lower valuation. That negotiation, which seems abstract at signing, is the one that determines whether employees ever see money.

Some acquirers also structure deals with retention packages, either to keep engineers through integration or because the deal is technically an acqui-hire dressed up as an acquisition. In those cases, the headline acquisition price is almost cosmetic. The real compensation is in cash retention packages paid over two to four years, which aren’t equity distributions at all. Employees who stick around may do fine. Employees who leave, or whose jobs are eliminated post-close, may not.

If you’re wondering about the other ways an acquisition can quietly change your situation, what really happens to your workflow after an acquisition covers the operational side of this.

What You Can Actually Do With This Information

If you’re currently employed at a startup, you can ask for the company’s total raised and the liquidation preference structure before you accept an offer or before a significant life decision hinges on a potential payout. Most companies won’t share the full cap table, but asking how much has been raised and whether preferred stock has participating rights is a reasonable question. A recruiter who can’t answer that shouldn’t be surprised you asked.

The number to care about isn’t the last valuation. It’s the liquidation preference overhang, meaning how much the acquisition price has to clear before common shareholders participate. If that number is $80 million and the company is struggling, your equity is out-of-the-money in the same way a stock option is worthless below its strike price.

If you’re a founder, understanding what you actually own after a VC writes you a check is where this conversation starts, not when the term sheet for the acquisition lands.

The uncomfortable truth is that startup equity for employees functions less like a wealth-building instrument and more like a lottery ticket with opaque odds. For a small number of people at a small number of companies, it pays off substantially. For the much larger group who work at startups that get acquired for less than they raised, the math simply doesn’t reach them. That’s not cynicism. It’s the structure of the deal, written into the certificate of incorporation on the day the first preferred check was cashed.