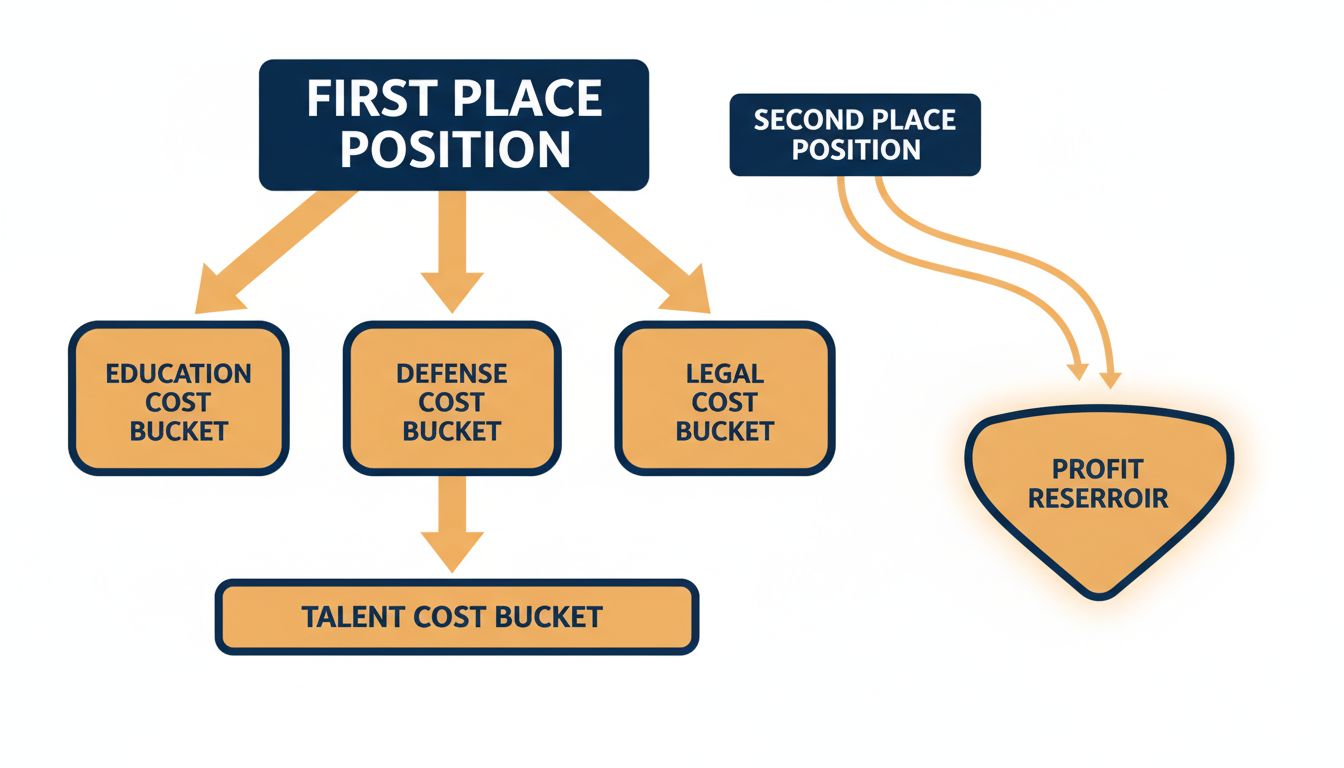

The instinct in tech is to chase number one. Highest market share, most users, fastest growth. But a consistent pattern across software, hardware, and platforms suggests the obsession with dominance is economically misguided. The second-largest player in a mature tech market frequently generates better margins, stronger returns on capital, and more durable earnings than the leader.

This isn’t about being a comfortable also-ran. It’s about where the costs of winning actually land.

1. The Leader Pays for the Market’s Education

Building a new category requires convincing customers that the problem is worth solving, the technology is trustworthy, and the vendor will be around in five years. That work is expensive. The first company to achieve dominance absorbs most of those costs, through sales cycles that take years, support infrastructure for early-adopter edge cases, and marketing that establishes the category before it establishes the brand.

By the time a strong second player has scaled, customers already believe in the category. The sales cycle shortens. The educational overhead drops. The second player can redirect that budget toward product quality or simply toward margin.

2. R&D Spending Becomes Defensive at the Top

Market leaders face a structural trap: they have to protect their position across every possible threat vector. That means funding research into adjacent areas not because there’s a compelling business case, but because a competitor might build something there. It means maintaining legacy products for enterprise customers who refuse to upgrade. It means running R&D programs whose primary purpose is deterrence.

Second-place companies can be selective. They can watch which bets the leader makes, identify which ones actually gain traction, and follow with more targeted investment. This is not a new observation, but its financial consequences are underappreciated. The leader’s R&D line carries substantial defensive spending that never converts to revenue. The follower’s R&D tends to be more concentrated on things customers will actually pay for.

3. Talent Costs Less When You’re Not the Prestige Hire

The top company in any hot tech sector becomes a magnet for candidates who want the credential, not just the job. That drives up compensation for everyone. Google, Amazon, and Salesforce all pay prestige premiums that their second-tier competitors don’t match. The market leader essentially sets a wage floor that disproportionately burdens itself.

The second-place company attracts strong engineers who want interesting problems and competitive pay, but who aren’t specifically chasing the brand. In many cases that produces better retention: people leave prestige employers at high rates once they have the credential. Companies one step below the prestige tier often show better tenure numbers, which matters because institutional knowledge has real dollar value.

4. Pricing Power Sits With the Alternative, Not the Standard

This is the most counterintuitive piece. You’d expect the market leader to have the strongest pricing power, and in some narrow sense it does: it can charge more than anyone else. But enterprise buyers are sophisticated. They almost always run a competitive process, and they need a credible alternative to the leader to negotiate effectively.

The second-largest vendor in a market is the preferred alternative. That position is structurally valuable. It means full deal flow from every major customer evaluation, without having to compete against five smaller players for the right to be taken seriously. It also means pricing discipline: the second player doesn’t have to slash prices to get in the room. They’re already in the room by default. Salesforce benefits from this when competing against Oracle. AMD benefits when Intel’s enterprise clients want leverage. The alternative slot pays well.

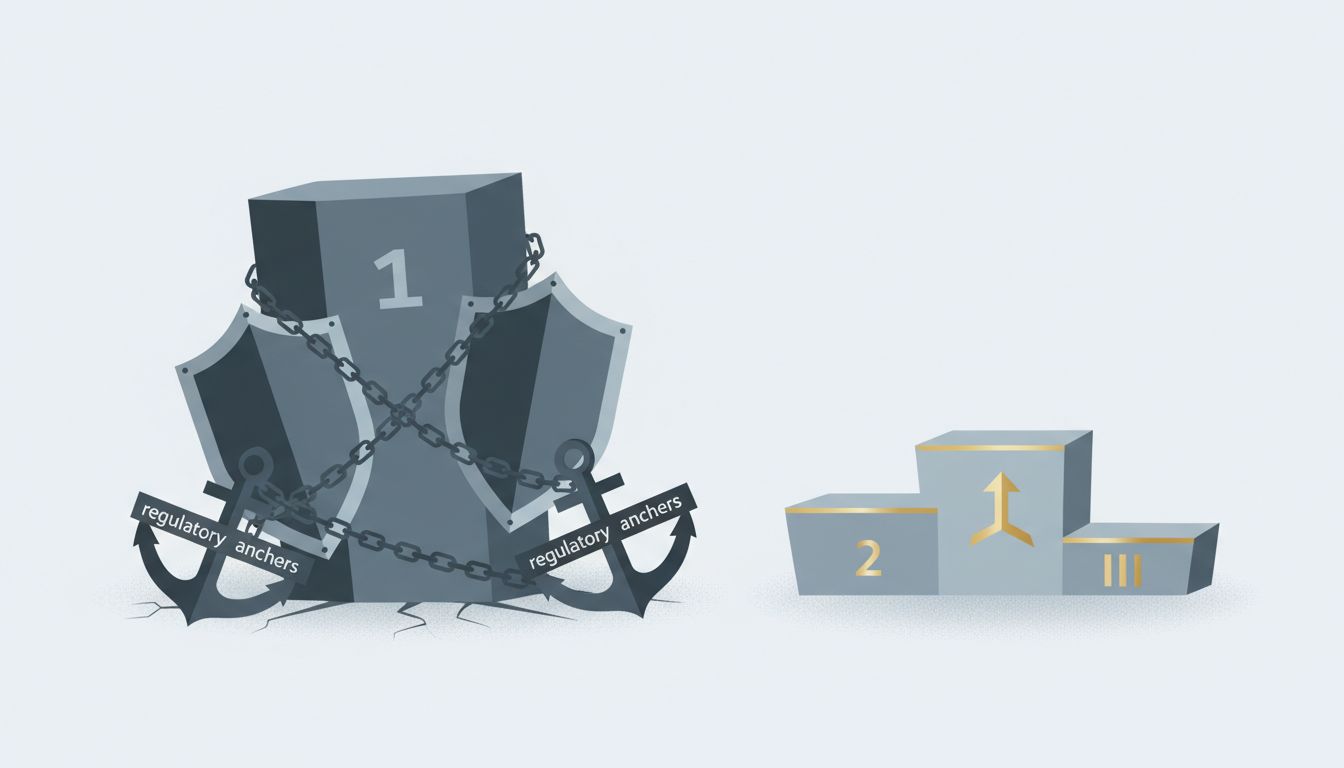

5. Regulatory Scrutiny Scales With Dominance

Antitrust attention follows market share. The leader’s legal and compliance costs grow substantially as dominance solidifies, not just from direct enforcement actions but from the organizational overhead of responding to inquiries, preparing documentation, and structuring deals to avoid triggering review. Google’s parent company Alphabet has spent heavily on antitrust defense across multiple jurisdictions simultaneously. Microsoft spent years in consent decree management after its browser-war-era dominance. These aren’t catastrophic costs, but they’re not trivial either, and they scale with how dominant you actually are.

The second-place company operates largely outside this zone. It can pursue acquisitions with less scrutiny. It can structure partnerships without worrying that regulators will interpret them as foreclosure strategies. The regulatory headroom at number two is genuinely worth something on the balance sheet, even if it rarely appears there explicitly.

6. Failure Is Cheaper When You’re Not Carrying the Market

When the market leader launches a product that fails, it’s news. Customers who relied on that product direction feel misled. Partners who built integrations around it face write-downs. The organizational cost of a high-profile failure at the top is amplified by the scrutiny and dependencies that come with dominance.

Second-place companies can experiment with less collateral damage. Their failures are quieter. Their bets are smaller relative to the whole market’s expectations. This is not just about reputation management; it’s about the actual financial cost of winding down products that didn’t work. Flexibility in experimentation has real economic value, and the leader has less of it.

None of this suggests that companies should aim to finish second. The point is more specific: the economics of tech markets routinely reward the runner-up more than the race’s winner, and companies that understand why can make better decisions about when to stop spending to close the gap. The costs of achieving and defending number one are systematic, not accidental. They come with the position. Knowing that should change how you evaluate whether the position is worth having.