The acqui-hire is Silicon Valley’s most elegant misdirection. Engineers celebrate landing at a prestigious company, founders announce a “partnership” on LinkedIn, and everyone moves on. What rarely gets discussed is that the transaction was almost certainly structured to make your equity disappear.

The core truth about acqui-hires: they are not acquisitions. They are recruiting transactions dressed up in acquisition paperwork. The acquirer wants the team. The price is set accordingly, and in most cases, that price does not cover the liquidation preferences sitting above common stockholders.

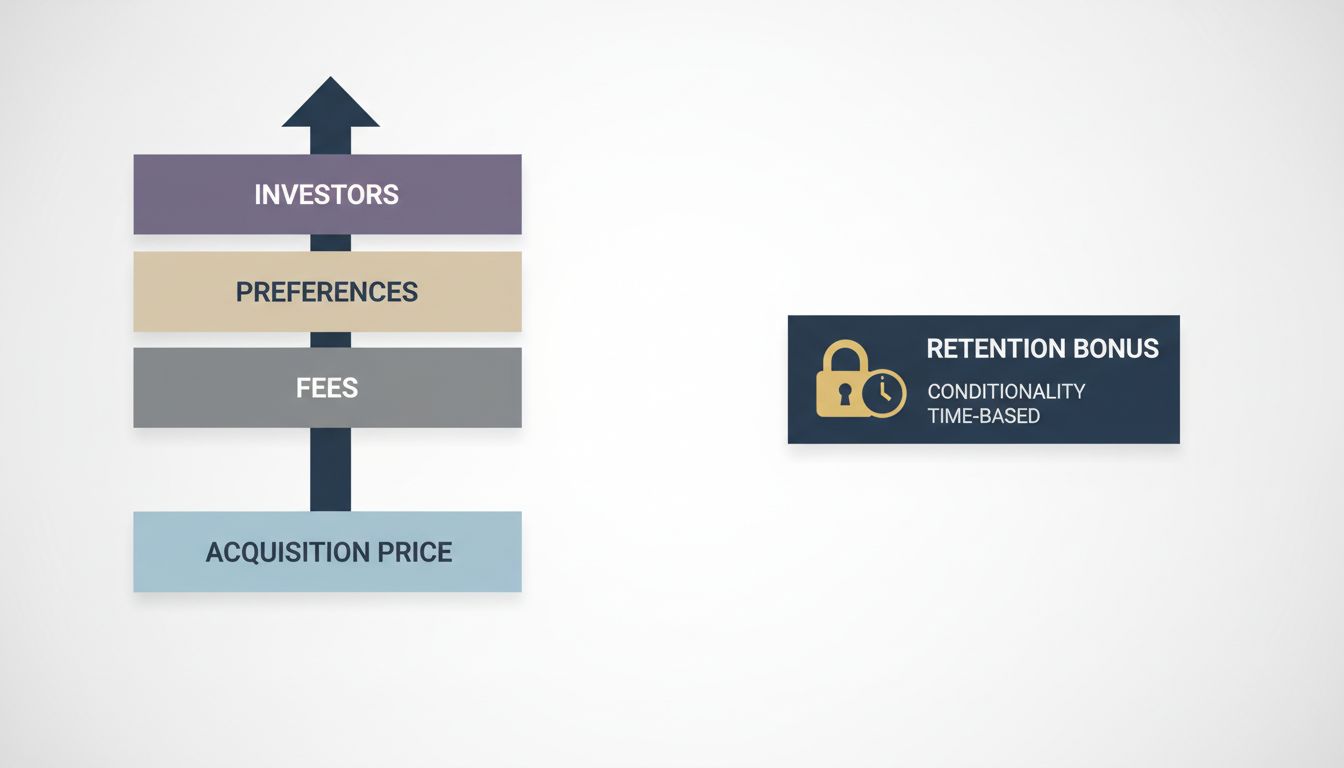

Liquidation Preferences Come First, Always

Most venture-backed startups have investors holding preferred stock with liquidation preferences, sometimes at 1x, sometimes at 2x or more. This means investors get paid before common shareholders see a dollar. In an acqui-hire, the total consideration is typically modest, often in the range of $1 million to $5 million per retained engineer, structured as a retention package rather than purchase price. That structure matters enormously.

When the deal is split between a nominal acquisition price (say, a few million dollars for the company’s IP and goodwill) and separate employment agreements covering retention bonuses and new equity grants, the acquisition price is often just enough to satisfy preferred investors at par, with nothing left for common shareholders. Founders who hold common stock, and employees with options, frequently receive zero from the company sale itself. Their compensation comes from the new employer, contingent on staying.

Options Are Often Underwater Anyway

Even before liquidation preferences enter the picture, employee stock options carry their own trap. Options have a strike price, and if the company’s 409A valuation has increased significantly while performance stalled, employees may hold options worth less than their exercise cost. In an acqui-hire scenario, where the per-share acquisition price is low, those options expire worthless. The employees walk away with a retention bonus from the acquirer and new unvested equity, which is exactly what the acquirer wanted to give them in the first place, minus the acquisition paperwork.

The situation is particularly acute for employees who joined early, paid for early exercise, and held actual shares rather than options. They have real exposure to the acquisition price. But early exercise requires cash upfront and a tax bet on future value, so most employees never do it.

Retention Agreements Create Handcuffs, Not Windfalls

The retention bonuses and new equity grants that replace your old equity are not the same thing. They come with new vesting cliffs, typically one year, and they are contingent on continued employment. Leave within 18 months and you often forfeit a significant portion. This is intentional: the acquirer is buying talent retention, not rewarding past contribution.

From the acquirer’s perspective, this structure is rational. They are paying for future output. From the employee’s perspective, it is a substitution of uncertain but potentially large upside (your startup equity) for a more certain but much smaller package (a signing bonus plus market-rate comp). The psychological framing as an acquisition obscures that this is essentially a lateral hire with a transitional payment.

The Founder’s Math Is Worse Than It Looks

Founders are sometimes surprised to discover they also hold common stock, not preferred, or that their preferred shares converted long ago. A founder who raised three rounds at increasing valuations may find that investors are owed multiples of the acqui-hire consideration before any proceeds reach the cap table. In some cases, the acquirer negotiates directly with lead investors to waive their preferences in exchange for a faster close, but this requires investor goodwill that is not guaranteed.

What founders typically do receive is credit toward their reputation and a decent title at the acquiring company. These have real value in the long run. But they are not equity returns, and confusing the two is how founders end up endorsing deals their employees should scrutinize more carefully.

The Counterargument

Reasonable people argue that acqui-hires serve a legitimate function. A startup that cannot find product-market fit or has run out of runway would otherwise simply shut down, and employees would receive nothing at all. An acqui-hire at least provides a soft landing, continued income, and a brand-name employer on the resume. Investors who accept reduced returns are making a rational choice to preserve a relationship and recover some capital rather than zero.

This is true. The acqui-hire is not a scam. It is a structured outcome for companies that have run out of better options. The problem is the framing, not the mechanism. When the transaction is announced as an acquisition, employees parse it through an acquisition frame and expect acquisition economics. The mismatch between that expectation and the reality of what lands in their accounts is where genuine harm occurs.

What You Should Actually Do

If your company is in acqui-hire discussions, push for a full cap table breakdown before you sign anything. Understand exactly how the consideration is split between the purchase price and your employment agreement, because those are governed by completely different rules. The employment portion is negotiable in ways the acquisition price often is not.

Also clarify your unvested options. Some acqui-hires include single or double trigger acceleration clauses that vest unvested shares upon acquisition or termination. If yours does not, you may be walking away from options that would have vested over the next two years with nothing but the acquirer’s new grant to replace them.

The acqui-hire will be dressed up as good news. Sometimes it genuinely is. But the equity math deserves honest scrutiny, and the people best positioned to give you that scrutiny are not the founders or the acquirer. They are a lawyer who has read your option agreement and the term sheets from every round you ever signed.