The Paradox of the Throne

The company at the top of a tech market gets the press coverage, the keynote stages, and the analyst attention. It also tends to absorb the worst economics in the industry. This is not an accident. It is a structural feature of how technology markets work, and once you see it, you start noticing it everywhere.

AMD and Intel make a useful starting point. For most of the 2000s and early 2010s, Intel owned the x86 processor market with shares that sometimes exceeded 80 percent. AMD hovered in the mid-teens. Conventional wisdom said Intel was winning. But look at what Intel spent to maintain that lead: massive capital expenditures on fabrication plants, relentless R&D cycles to stay ahead, aggressive pricing to punish customers who considered switching. When Intel stumbled on its 10-nanometer process in 2018, the cost of that stumble was enormous precisely because it was defending a position that required perfection. AMD, unburdened by the need to be first everywhere, picked its battles and built chips that competed selectively. By 2020 and 2021, AMD’s operating margins had climbed significantly while Intel was issuing profit warnings.

How Market Leadership Becomes a Cost Center

Being the clear market leader in technology is not just a reward. It is an obligation with a running tab.

Leaders have to support the broadest customer base, which means maintaining legacy compatibility that no rational new entrant would bother with. Microsoft’s Windows team has carried decades of backward-compatibility requirements specifically because Windows owns the desktop market. Abandoning that compatibility would hand an opening to competitors. Maintaining it costs engineering time and slows down the pace at which the product can evolve. This is a tax that comes with dominance.

Leaders also face the most intense regulatory attention. The EU’s Digital Markets Act was written with a handful of dominant platforms in mind. Google, Apple, and Meta face enforcement actions and compliance costs that their smaller competitors don’t. Antitrust litigation is expensive, distracting, and, more importantly, constraining: a market leader often cannot make acquisitions or pricing moves that a number-two player could execute without scrutiny. The competitive cost of that constraint is real.

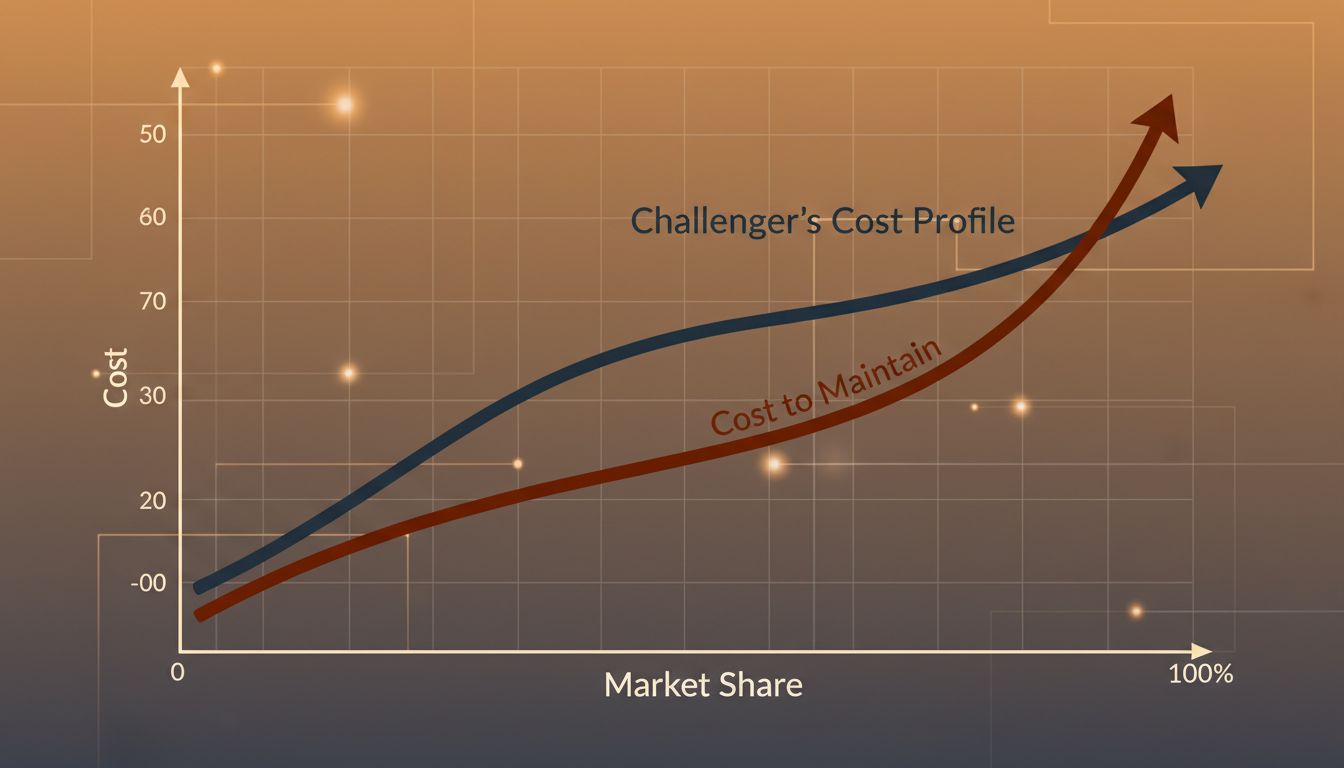

And then there is the marketing problem. When you are number one, customers stop comparing you favorably to the competition. They compare your current product to your last product. Every shortcoming becomes a headline because expectations are set to a different standard. The number-two player gets credit for progress. The leader gets blamed for imperfection.

The Challenger’s Structural Advantages

The second-largest player operates under a different set of constraints, and most of those constraints are quietly favorable.

First, challengers can be selective. They don’t have to serve every customer segment, every geography, or every use case. Salesforce built its early success partly by ignoring the enterprise customers that Siebel Systems was exhausting itself trying to retain. ServiceNow took a narrow slice of IT service management before expanding outward. Selectivity means better gross margins, because you are serving the customers where your product fits well, not the ones you win by discounting to defend share.

Second, challengers get to learn from the leader’s spending. When the number-one company runs an expensive marketing campaign to explain why a new category matters, it is partly educating the market for everyone. When Amazon built out AWS and spent years convincing skeptical enterprise IT departments that cloud infrastructure was safe, it was clearing a path that Microsoft Azure and Google Cloud walked through with considerably less customer education required. Azure’s early growth benefited from market-creation work that Amazon had already paid for.

Third, the challenger’s talent strategy is often more efficient. Top engineers and product managers want to work on hard problems. The market leader’s hardest problems are often defensive, political, or legacy-related. The challenger’s hardest problems are usually offensive: how do we build something better? That asymmetry matters for recruiting, and recruiting is a significant cost driver in technology businesses.

The Numbers Behind the Pattern

The profitability gap shows up clearly in operating margins over time, though the exact figures shift with each earnings cycle.

Take the search advertising market. Google controls roughly 90 percent of global search queries. Microsoft’s Bing has a fraction of that. Yet Microsoft’s search and news advertising segment has been growing operating income steadily, partly because the unit economics of Bing traffic are favorable: Bing’s users skew toward higher-income, older demographics who convert well on commercial searches, and Microsoft doesn’t have to serve billions of queries from users who will never buy anything. Google has to serve all of them, because ceding any segment creates an opening.

Or consider cloud infrastructure. AWS held the dominant share for years, and still does in many measures. But Azure’s operating margins in Microsoft’s Intelligent Cloud segment have been competitive with or, in some periods, superior to what Amazon’s AWS segment reports, despite AWS having the longer track record and larger installed base. Microsoft could price cloud services to its existing enterprise relationships, essentially bundling deals rather than competing for new logos from scratch. AWS had to continue buying market presence.

This is not a universal law. There are markets where the number-two player is a money-losing basket case kept alive by investor optimism. But when both companies are well-managed and genuinely competing, the profitability advantage tends to sit with the challenger.

Why Leaders Don’t Just Retreat

If defending the top position is so expensive, the obvious question is why market leaders don’t deliberately shrink their market share to improve margins.

The short answer is that this is much harder to execute than it sounds. Investors and analysts price technology companies on growth and market share. A deliberate decision to serve fewer customers reads as retreat, not strategy. The stock price reaction tends to be punishing, which makes acquisitions more expensive, stock-based compensation less attractive, and executive tenure shorter. The incentive structure makes rational margin-focused retreats nearly impossible to execute publicly.

There is also a network effects problem in many tech markets. A platform that loses users loses value for the remaining users, which accelerates further departures. Deliberately ceding share in a networked market is not the same as ceding share in, say, a hardware market. You can’t decide to have fewer users on a two-sided marketplace without risking a spiral.

So leaders are largely trapped. They have to spend to defend, and the spending erodes margins, and they can’t explain to shareholders why a voluntary retreat would be in their interest. The challenger has no such trap. It can add share without facing the same defensive spending, and it can stop adding share when the marginal cost of the next point of market penetration exceeds the benefit.

When the Second Position Becomes Unsustainable

This advantage is not permanent. The second-place player’s economics tend to degrade as it approaches market parity with the leader. At that point, the challenger faces the same defensive dynamics it once exploited. This is partly why so many number-two companies make acquisitions or product pivots when they get close to the top: they are buying their way into new markets where they can be a challenger again.

Microsoft is the clearest example. Having been the dominant platform company in personal computing, it found itself defending expensive legacy positions while Google and others ate into its relevance. Satya Nadella’s pivot to cloud was, among other things, a strategic move to become a challenger in a new market (cloud infrastructure) rather than continuing to defend an expensive leadership position in one that was flattening (packaged software). Microsoft effectively traded margin-eroding market leadership in one segment for challenger economics in another.

The same logic applies in smaller markets. A company that achieves dominant share in a specific SaaS category faces the choice of either defending that position at increasing cost or finding adjacent markets where it can start the challenger cycle again. The ones that keep growing profitably tend to be the ones that understand when to stop fighting for the top spot and where to look for the next second-place opportunity.

What This Means

For anyone analyzing tech businesses, the market-share rankings deserve more scrutiny than they usually get. First place is not obviously better than second place when you account for the full cost of maintaining it. The profitability advantage often sits with the well-positioned challenger, not the entrenched leader.

For companies, the implication is counterintuitive: the goal of total market dominance is often a trap. Winning 35 percent of a market with 65 percent gross margins tends to be worth more than winning 70 percent with 50 percent gross margins. The second number is what you’re building toward when you push for leadership at any cost.

For investors, the lesson is to be skeptical of market-share growth as a standalone metric. A company buying share through aggressive pricing or heavy spending is not necessarily building a more valuable business. It may be building a more expensive defensive position that will require constant capital to maintain. Burn rate is the wrong number to watch, but so is market rank when it comes without a view into what that rank actually costs to hold.