I watched a founder walk into a Series B pitch with a slide deck full of healthy-looking numbers and walk out without a term sheet. The MoM growth was solid. The logo count was impressive. The NPS scores were high. And none of it mattered, because every metric on that deck was measuring the wrong thing for the stage the company was actually in.

This is the trap. The metrics that get you to Series A are survival metrics. They prove you have something real, that people want it, and that you can acquire customers without setting money on fire. They are necessary. They are also, if you’re not careful, the thing that blinds you to whether you have a scalable business.

Series B is a different question entirely. It’s not “does this work?” It’s “can this get very large, very efficiently?” Those questions require completely different measurement.

Growth Rate Hides the Shape of Growth

At Series A, 15% month-over-month growth is a signal that something is working. At Series B, that same number tells investors almost nothing without knowing where the growth is coming from. Growth fueled by founder relationships, word of mouth, and a couple of anchor customers is not the same as growth with a repeatable, measurable acquisition engine.

The founders who get caught here are the ones who never decomposed their growth. They know the aggregate number. They don’t know what percentage came from organic search versus direct outbound versus partner referrals versus their own LinkedIn posts. When a Series B investor asks “how do you get from $5M to $25M ARR?”, the honest answer is often “we’re not sure, things have just been working.” That answer doesn’t close rounds.

Retention Looks Fine Until You Cohort It

This one is sneaky. Overall retention can look healthy while cohort retention is quietly deteriorating. If you’re adding customers fast enough, new cohorts mask the churn in older ones. Your aggregate retention rate stays in the acceptable range. Your gross revenue churn looks fine. But slice the data by acquisition quarter, or by customer segment, or by use case, and you might find that customers who signed up in year one are sticking around while the customers you landed more recently are churning at alarming rates.

Series A investors often don’t push hard enough on cohort analysis. Series B investors do. And when they find a deteriorating retention curve hidden under aggregate numbers, the deal dies. Not because the business is unfixable, but because the founder didn’t know it was there.

Unit Economics That “Work” Don’t Mean Unit Economics That Scale

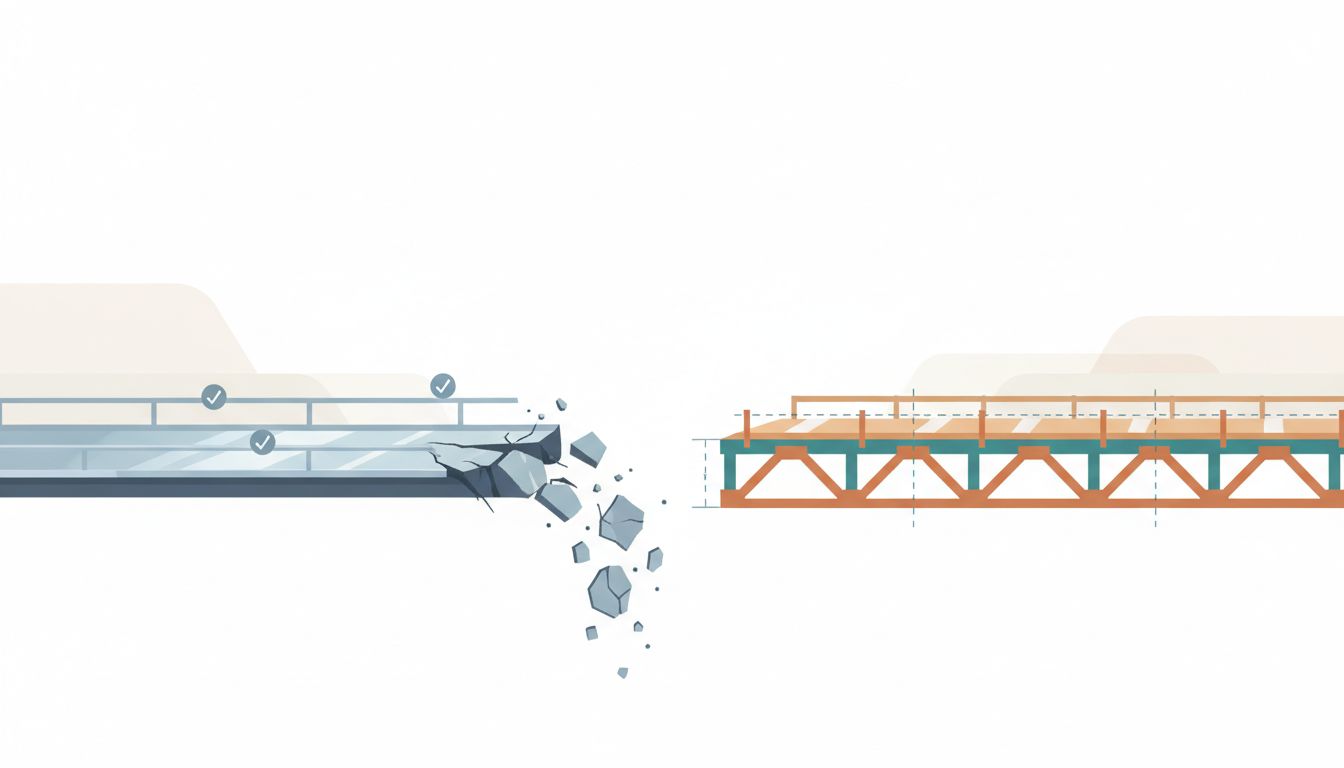

At Series A, you need to show that you can acquire a customer for less than they’re worth. CAC payback under 18 months, LTV:CAC above 3:1, whatever your benchmarks are. Clearing this bar is table stakes. The problem is that these numbers were generated in a market where you were selling to early adopters who sought you out, where your sales cycles were short because early customers make faster decisions, and where your CAC was artificially low because founders were closing deals themselves.

When you scale, all of that changes. You move from inbound enthusiasm to outbound effort. Sales cycles lengthen. You’re selling to buyers who need more convincing. Your true CAC, across a real and repeatable go-to-market motion, might be two or three times what it was in the early days. Investors who have seen this pattern before will haircut your unit economics assumptions on instinct. If you haven’t stress-tested them yourself first, you’re going to get caught flat-footed.

This also connects directly to how your pricing is shaping your roadmap. Founders who priced low to win early customers often find their unit economics structurally broken at scale, and repricing an installed base is brutal.

The Counterargument

Some founders push back on this and argue that obsessing over Series B metrics too early is a form of premature optimization. Focus on the product, focus on customers, focus on growth, and the metrics will take care of themselves. There’s real truth in that. Startups that spend too much time on investor-facing reporting and not enough time on the actual business are a real failure mode.

But there’s a difference between obsessing over metrics and understanding them. You don’t need a CFO and a full BI stack at Series A. You do need to know the shape of your growth, the cohort behavior of your customers, and what your unit economics look like when you remove founder-specific advantages from the equation. That knowledge isn’t for investors. It’s for you.

The Actual Problem

The metrics that got you to Series A were measuring whether your idea had merit. The metrics you need for Series B measure whether your business has structure. Those are different instruments for different questions, and confusing them is one of the more common and preventable ways founders stall out between rounds.

The founders who navigate this well aren’t the ones who had better numbers. They’re the ones who stayed genuinely curious about what their numbers actually meant, not just whether they were going in the right direction. They decomposed their growth before they had to. They ran cohort analysis before an investor asked. They stress-tested their unit economics against a world where they couldn’t personally close every deal.

Your Series A dashboard got you to the next level. It is not a map of where you’re going.