The Simple Version

When a startup raises far more money than it can usefully spend, it doesn’t get more runway. It gets a bigger bonfire. The extra capital accelerates spending on things that don’t work, inflates expectations that can’t be met, and boxes the company into a future it may not actually want.

Why Fundraising Feels Like Winning

There’s an obvious reason founders celebrate big rounds. Money solves the most visceral problem in early-stage startups: the possibility of running out. A large raise extends the horizon, buys time, signals credibility to customers and recruits. The press release goes out, the congratulations come in, and it genuinely feels like progress.

But fundraising is not progress. It’s a transaction. You’ve traded equity and future obligations for cash. Whether that trade was worth it depends entirely on what you do next, and large raises have a structural tendency to cause bad decisions.

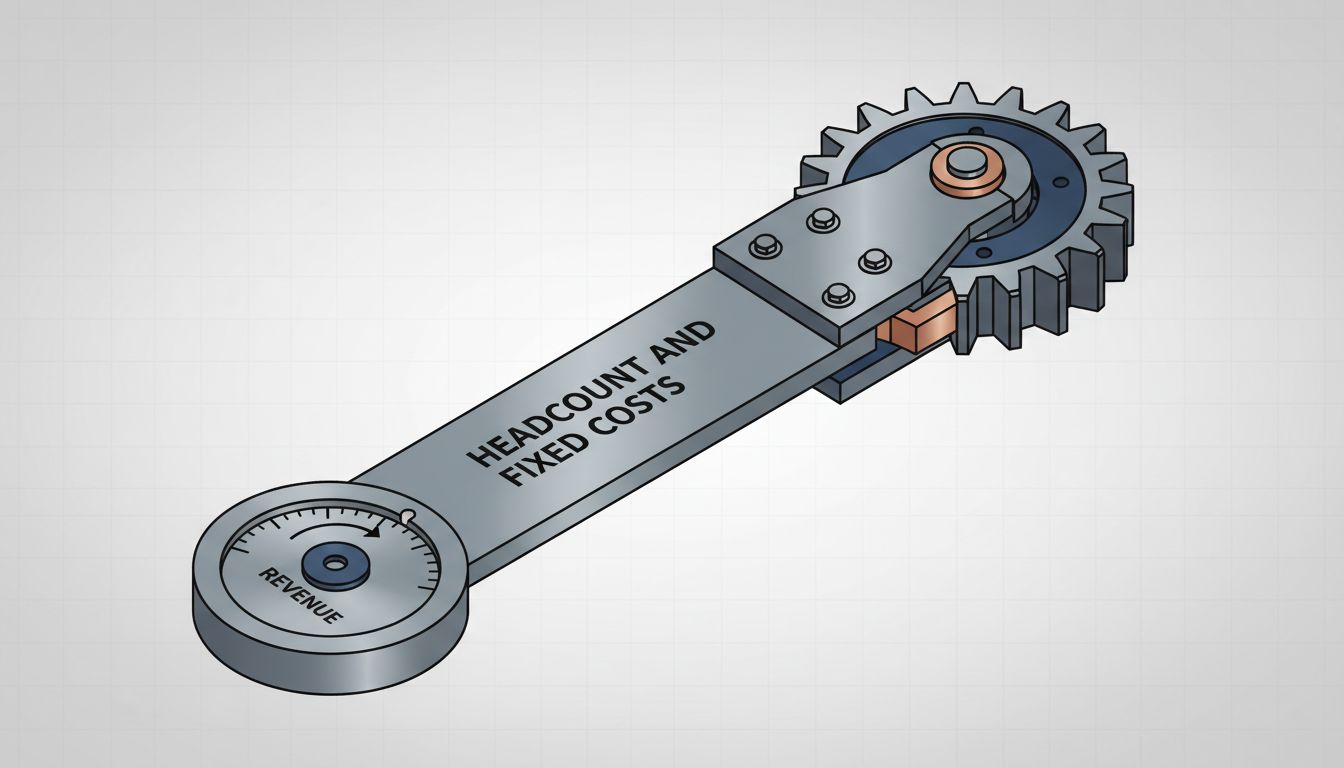

The Burn Rate Ratchet

Here’s the mechanism. You raise $30 million for a company that had been operating on $3 million a year. The new capital comes with implied expectations from investors, new obligations to a larger team, and a social pressure to act like a $30 million company. So you hire more people. You rent real office space. You build out functions you don’t yet need, like a formal HR department or an enterprise sales team, because that’s what companies your size are supposed to have.

None of this is irrational in isolation. But collectively, it locks in a burn rate that was never justified by actual business performance. You’ve turned a flexible, scrappy organization into one with fixed costs and fixed headcount, and those things are very hard to unwind without causing damage.

The companies that grow too fast and then collapse often aren’t failing because growth slowed. They’re failing because their cost structure was built for a growth rate that was never going to last.

The Valuation Trap

There’s a second problem, quieter but just as dangerous. When you raise a large round at a high valuation, you’ve set a floor on your future.

Your next round has to be at a higher valuation or you face a down round, which triggers anti-dilution provisions, signals distress to the market, and demoralizes employees whose options are now underwater. Acquisition interest is suppressed because any potential buyer now has to clear a number that reflects venture-scale ambitions rather than the realistic value of the business.

This is the trap that catches otherwise viable companies. A startup worth $150 million as an acquisition might have raised at a $400 million post-money valuation. The founders can’t sell. The investors won’t approve it. So the company keeps swinging for a valuation it may never reach, spending down capital trying to get there, until there’s nothing left. Your startup’s valuation mathematics become genuinely strange the moment you stop fitting the expected growth curve.

What Capital Abundance Actually Does to Decisions

This is the part that gets the least attention: money doesn’t just change what you spend. It changes how you think.

Scarcity forces prioritization. When a team has twelve months of runway and one product bet, they focus with extraordinary clarity. They talk to customers obsessively. They cut features ruthlessly. They say no to distractions because they have no choice.

Abundance removes that discipline. With four years of runway, there’s always time to try one more thing, hire one more specialist, explore one more market segment. The sense of urgency that makes early startups move fast and learn quickly gets replaced by the deliberateness of a larger organization. And a startup behaving like a large organization before it has earned that right is almost always slower, not safer.

This shows up in meeting culture, in hiring velocity, in how long it takes to kill a bad idea. The cognitive overhead compounds. Resources that could go toward the core problem get redistributed across too many bets, none of which get the concentration they need.

When Big Raises Do Make Sense

Large rounds are not always mistakes. They make clear sense when capital is itself the product’s moat: infrastructure companies, semiconductor fabs, biotech firms burning cash on clinical trials. They make sense when a market is genuinely winner-take-most and speed of distribution is the entire game. They made sense for Airbnb in 2020 when the company needed to survive a catastrophic revenue collapse and the capital markets were briefly generous.

The pattern to watch for is fit between capital and strategy. A B2B SaaS company selling to mid-market buyers does not need to raise like OpenAI. A marketplace connecting freelancers to small businesses does not need a war chest built for global logistics. When the round size is out of proportion to the actual competitive dynamics of the business, that misalignment will eventually surface as misallocated spending or a valuation that can’t be sustained.

The Number That Actually Matters

The question founders should ask isn’t how much they can raise. It’s how much capital they can productively deploy in the next 18 to 24 months, specifically on things that will meaningfully de-risk the business.

If the honest answer is $4 million and the market will give them $20 million, raising $20 million is not a conservative choice. It’s an aggressive bet that they’ll figure out how to spend the rest usefully, under pressure, while also running the business. That bet fails more often than it succeeds.

The best fundraising outcome is rarely the largest check. It’s the right amount from the right investors at a valuation the company can grow into. That’s a harder sell to make, both to investors and to a founder’s own ambitions. But the startups that survive long enough to matter tend to be the ones that treated capital as a tool rather than a scoreboard.