The press release writes itself. A promising startup raises $50 million in Series B funding, led by a marquee venture firm, with participation from strategic investors. The founder talks about acceleration. The investors talk about the market opportunity. Everyone talks about the future.

What nobody talks about is the arithmetic.

In 2021, Brex raised a $300 million Series D at a $7.4 billion valuation and promptly made a strategic decision that revealed something important about what large funding rounds actually purchase: not freedom, but obligation. Within a year, the company fired most of its small business customers and pivoted hard toward enterprise. The money didn’t buy optionality. It bought a specific trajectory, and that trajectory demanded a specific kind of customer.

The $50 million Series B sits at an interesting inflection point in that logic. It’s large enough to feel like arrival, small enough to run out faster than founders expect.

The Setup

Consider the modal Series B recipient in the current market. The company has between 30 and 80 employees. It has demonstrated product-market fit with a core customer segment but hasn’t cracked distribution. Revenue is real but the path to profitability requires either dramatic growth or dramatic efficiency, probably both. The founders have gone through the Series A, which bought time to find product-market fit. Now investors are paying for something different: proof that the business can scale.

The $50 million sounds large because it is large, relative to the Series A. It is not large relative to what it must accomplish.

Break it down honestly. A company with 60 employees, competitive salaries, benefits, and Bay Area office costs is spending somewhere north of $600,000 to $800,000 per month in operating expenses before you add the hiring the round is supposed to fund. Investors backing a $50 million round at this stage expect the company to double or triple headcount. Call it 120 to 150 employees at the end of the growth phase. Monthly burn climbs toward $1.5 to $2 million. At that rate, $50 million buys roughly two years of runway, which sounds comfortable until you account for the fact that raising the next round typically requires starting the process nine months before you need the money, and requires showing the kind of metrics that justify a valuation step-up, which requires the growth to have actually worked.

The actual window to prove the thesis is closer to 14 months.

What Happened to Convoy

Convoy, the freight-matching startup, is one of the cleaner case studies in what a heavily funded growth stage company can and cannot purchase with capital.

Convoy raised over $900 million total before shutting down in late 2023. The company was not obviously incompetent, and its core technology worked. What the capital could not buy was a structural margin advantage in a business where shippers and carriers both had significant negotiating power and where the incumbents, primarily large freight brokerages, competed aggressively on price when threatened.

The lesson from Convoy isn’t that they spent recklessly. It’s that the round sizes implied a path to dominance that the unit economics made structurally difficult. Each round purchased more volume, but volume in a thin-margin marketplace with sophisticated counterparties on both sides does not automatically become profit. The capital funded growth that looked like traction but was actually competition-subsidized market share.

Convoy’s problem was not unique to them. It’s endemic to a certain kind of Series B thesis where the implicit argument is: if we get big enough fast enough, the economics will follow. Sometimes they do. Often they don’t.

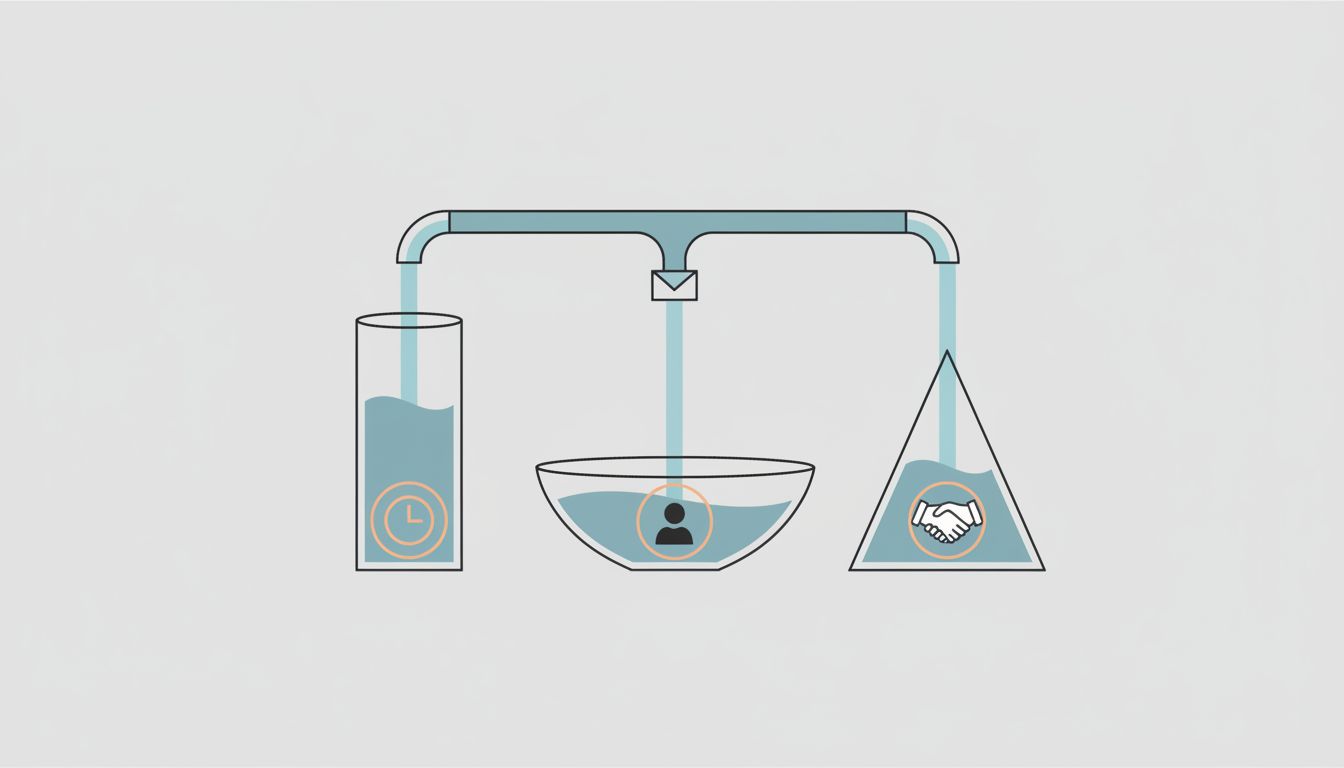

The Three Things Capital Actually Buys

Strip away the narrative, and a $50 million Series B purchases three things specifically.

First, it buys time to find out if your distribution model works. Series A proved the product. Series B proves whether you can repeatably acquire customers at a cost structure that leaves room for margin. Every dollar spent on sales and marketing at this stage is essentially a hypothesis test. Companies that use the round this way, instrumenting acquisition channels carefully and cutting what doesn’t perform, tend to come out the other end with something real. Companies that treat the capital as permission to hire aggressively across all functions simultaneously tend to discover the distribution problem later, with less money and more organizational complexity.

Second, it buys the right to recruit people who won’t join a seed-stage company. The talent unlocked by a credible Series B is real. Engineers, product leaders, and operators who want meaningful equity but also some signal that the company will survive long enough for that equity to matter will take meetings they wouldn’t have taken before. This is not trivial. The people you can hire at Series B are often the people who determine whether the product and organization can actually scale.

Third, and most underappreciated, it buys negotiating leverage with customers and partners. Enterprise procurement departments apply significant scrutiny to vendor financial health. A recently closed Series B from recognizable investors is a form of credibility that shortens sales cycles and opens doors that would otherwise require years of track record. The capital itself isn’t spent on these relationships, but its existence changes them.

Why the Number Is Almost Irrelevant

The headline figure matters less than the conditions attached to it. A $50 million round raised at a $400 million post-money valuation is a very different instrument than the same amount raised at $150 million. The first implies a liquidation preference stack and growth expectations that may require the company to sell for $800 million just for common shareholders to see meaningful returns. The second leaves room for a broader range of outcomes.

Founders who focus on the check size without modeling the cap table mechanics often build themselves into a corner. The pressure to justify an aggressive valuation drives decisions that optimize for the next fundraise rather than the underlying business. As we’ve written about elsewhere, excess capital can be as dangerous as insufficient capital, precisely because it changes behavior in ways that aren’t immediately visible.

The companies that deploy a $50 million Series B most effectively tend to share a counterintuitive trait: they don’t try to use all of it at once. They stage their own spending, treat the round as a series of smaller bets, and preserve optionality by not assuming the bull case from day one. They understand that the round bought them a runway, not a guarantee.

What We Can Learn

A $50 million Series B is a test of organizational discipline as much as market opportunity. The capital creates the conditions for scaling but does not create the scale itself. The companies that mistake the former for the latter tend to produce cautionary tales.

The most useful frame for any founding team staring at a large wire transfer is this: what specific question does this money answer? Not what does it enable in the abstract, but what concrete claim about customer acquisition, retention, or unit economics will be falsified or validated by the time this capital is gone?

If the team can answer that question precisely, the $50 million is a genuine asset. If the answer is some version of “we’ll grow and figure it out,” the money will mostly fund the figuring-out part, and the next round will be harder than expected.