A founder I know closed a seed round at a $6M post-money valuation, burned through the cash faster than projected, and took a $500K bridge note to buy time for a Series A. The bridge converted at a 20% discount. The Series A priced at $12M pre-money. Felt like a win. Then his lawyer walked him through the actual dilution math, and he went quiet for a long time.

Bridge rounds are sold as a tactical pause, a way to extend runway without the friction of a full priced round. And sometimes that’s exactly what they are. But “bridge” is a marketing term. What you’re actually doing is issuing debt that converts into equity under terms you’re negotiating while your leverage is at its lowest. Understanding the mechanics isn’t optional.

The Instrument Determines Everything

Most bridge rounds use one of two instruments: a convertible note or a SAFE (Simple Agreement for Future Equity). The distinction matters more than founders typically appreciate.

A convertible note is actual debt. It accrues interest, has a maturity date, and if you don’t raise a qualifying financing round before that date, the noteholder can demand repayment or, depending on your documents, force a conversion at terms they negotiate from a position of power. SAFEs don’t accrue interest and have no maturity date, which removes some of that pressure, but they’re not magic. Both instruments defer the valuation question to your next priced round, and that deferral has a cost.

The cost is the discount rate and the valuation cap, often both applied simultaneously. A 20% discount means your bridge investors convert their debt into equity at 80 cents on the dollar relative to your next-round price. A valuation cap means they convert at whatever is lower: the cap or the discounted price. If your Series A prices significantly above the cap, bridge investors get a very good deal. Your new investors, who see the dilution their dollars are creating, will price accordingly.

How the Math Actually Works Against You

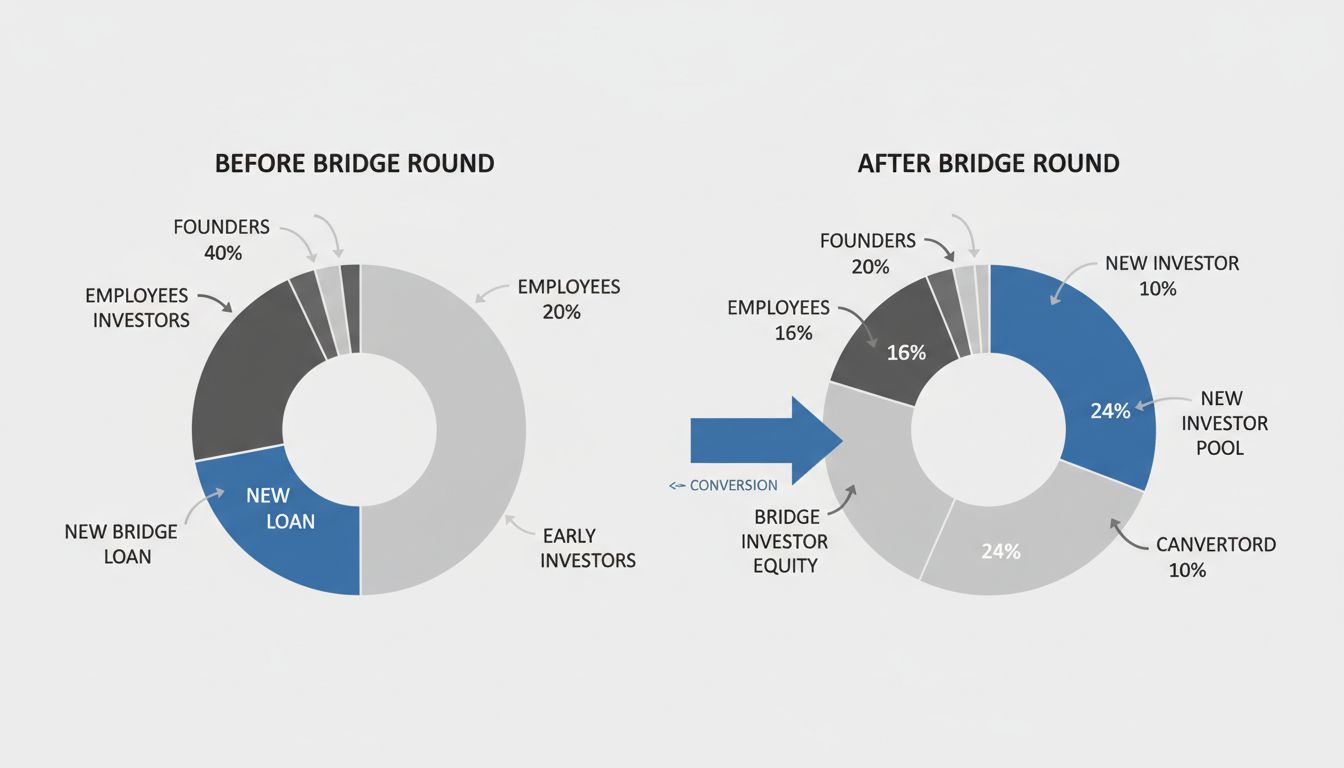

Here’s what gets founders. The dilution from a bridge round doesn’t hit when you sign the note. It hits at the next priced round, and it hits in a way that compounds.

Say you raise $1M on a convertible note with a $5M cap and 20% discount, and your Series A prices at $10M pre-money. Your bridge investors convert at $5M (the cap is lower than the discounted price), meaning they get twice the equity their dollar amount would have purchased at Series A pricing. New investors see the fully-diluted cap table including those converted shares and price their ownership percentage against that larger total. Everyone’s slice just got thinner, including yours.

Multiple bridge rounds make this dramatically worse. Each note stacks. The cap table going into a Series A with two or three uncapped or high-cap bridge rounds sitting on it can look so messy that institutional investors walk, or they use it as leverage to reprice the whole thing. Your runway number being wrong from the start is often what creates the conditions that make multiple bridges feel necessary in the first place.

The Terms That Bite Hardest

Few things in a bridge round are more punishing than MFN (most favored nation) clauses combined with uncapped notes. MFN means that if you issue another note on better terms, earlier noteholders get those terms retroactively. Uncapped means there’s no ceiling on their ownership percentage at conversion. If you take an uncapped bridge at a moment when you think your valuation will be modest, then execute and raise at a much higher price, the note converts at a discount to that high number. That’s actually fine. Where uncapped notes become genuinely dangerous is when you end up doing a down round or a flat round, and investors are converting at a discount to an already-low price, concentrating their ownership at your expense.

Pay attention to what happens at maturity if no qualifying financing occurs. Some notes automatically convert at a default valuation (often punishingly low). Others give noteholders the option to convert or demand repayment. The latter can put you in a legally awkward position even if you have cash, because “demand repayment” in a startup context often means “negotiate under duress.”

Pro-rata rights on bridge notes deserve scrutiny too. If your bridge investors have the right to participate in your next round to maintain their percentage, and that next round is oversubscribed, you’re now managing allocation politics with investors whose primary leverage was lending you money when you were desperate.

What Experienced Founders Do Differently

Founders who’ve been through this before treat bridge terms as seriously as priced round terms, because they are. A few things they do consistently:

They push for valuation caps that reflect honest future expectations, not optimistic ones. A cap that feels generous in a difficult moment becomes a very expensive promise if the company performs. The goal is fair, not founder-favorable.

They negotiate conversion mechanics explicitly, particularly what happens at maturity and whether interest counts toward the conversion amount. Accrued interest converting to equity is additional dilution that’s easy to forget about until the cap table update.

They keep the bridge investor group small and tightly controlled. Every additional party on a bridge note is another set of rights, another signature required for future waivers, another relationship to manage during a period when your attention is already stretched. The dynamics of how VCs evaluate unconventional bets are relevant here too: investors who joined at your most vulnerable moment often have a different relationship to the company than those who came in during a position of strength.

They also model the post-conversion cap table before signing anything. Not a rough sketch, an actual spreadsheet showing founder ownership, employee option pool, existing investors, and bridge conversion at multiple scenarios for the next round’s price. If that spreadsheet makes you uncomfortable at the low-end scenario, the terms need to change.

The Bridge Round Is Not the Problem

Taking a bridge round is not inherently a bad decision. Companies need capital to operate, and sometimes the timing of a priced round doesn’t align with operational reality. Bridges built many companies that wouldn’t exist otherwise.

The problem is treating the instrument as administratively simple because the dollar amounts feel small relative to what you’ll raise next. A $500K bridge at bad terms can cost you more founder equity than a $3M priced round at fair terms. The people who understand this aren’t founders who read more. They’re founders who’ve been surprised by a cap table once and decided never to be surprised again.

Get a good startup attorney, not a generalist, to review the note before you sign. Model the dilution yourself. Understand every scenario in the conversion language. The bridge might be necessary. The terms don’t have to be painful.