A founder I know spent six months telling investors he had eighteen months of runway. He was right, technically. He was also wrong in every way that mattered. By the time he realized it, he had four months to close a round or shut down. He closed the round, barely, under terrible terms.

His mistake wasn’t arithmetic. It was using the wrong number entirely.

The standard calculation is a snapshot, not a forecast

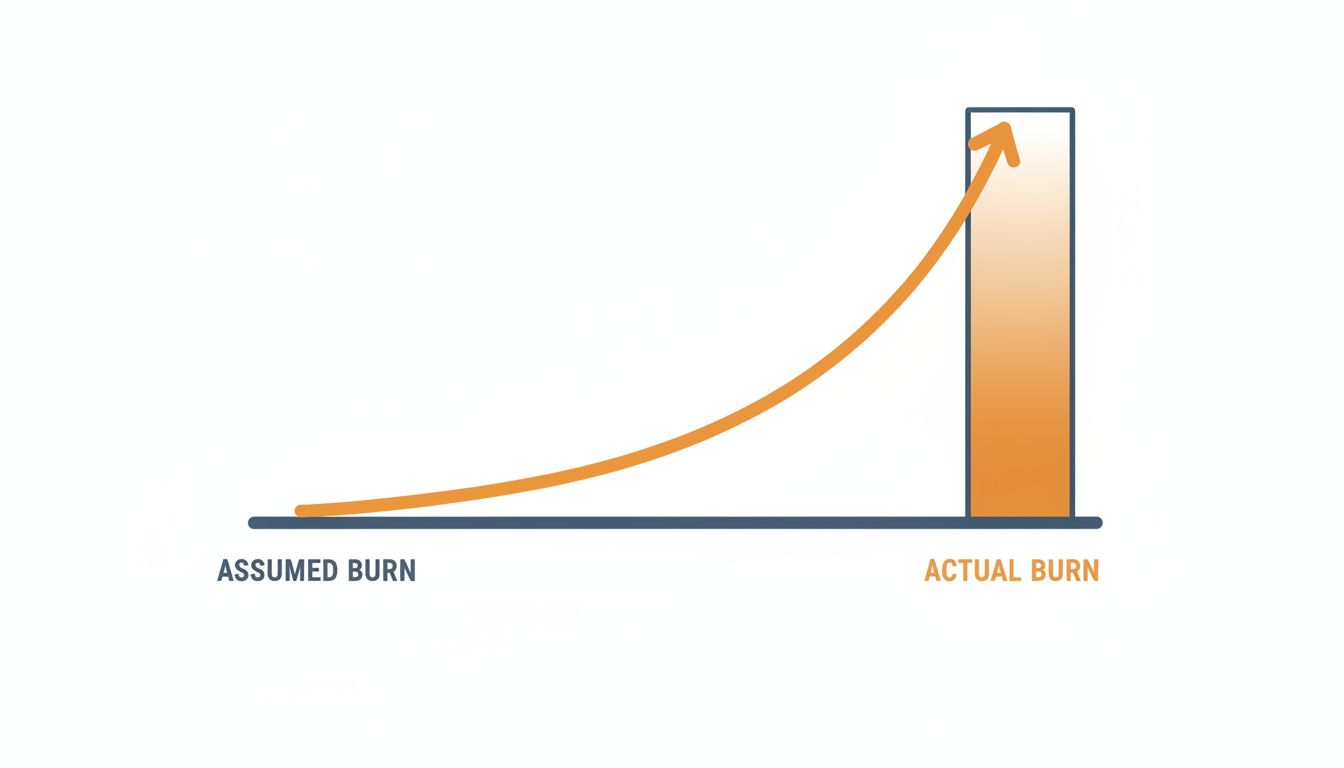

Most founders calculate runway like this: cash in bank divided by current monthly burn. If you have $1.2 million and you’re spending $100k a month, you have twelve months. Clean, simple, wrong.

The problem is that burn is not static. It’s a slope. Most early-stage companies are actively hiring, expanding sales, signing new software contracts, and generally spending more each month than they did the month before. A company with $100k monthly burn in January that’s growing headcount will often be at $140k or $160k burn by June. The simple division gives you twelve months. The actual runway, accounting for the burn curve, might be eight.

This is not an edge case. It’s the norm. And founders who present the static number to their boards aren’t lying exactly, but they are obscuring the one thing that matters most: when does the money run out under realistic operating assumptions?

The number you should be using

Runway should be calculated against your projected burn, not your current burn. That means building a bottoms-up model of headcount changes, planned software and infrastructure costs, and expected revenue changes, then drawing the actual cash balance curve over time.

When you do that, two things usually happen. First, your real runway shrinks, often significantly. Second, you can see exactly which decisions are driving it. That second part is the point. Runway as a single number is nearly useless. Runway as a curve tied to specific decisions is a management tool.

The other number most founders ignore is their fundraising timeline. A seed round can close in six to eight weeks if everything goes well. A Series A commonly takes four to six months from first meeting to wire. That time needs to come out of your runway before you treat it as available operating time. If you have ten months of runway and your raise will take five months to close, you have five months to start that process before you’re in genuine trouble. Most founders wait until they feel the pressure, which means they start too late.

Cash isn’t the only resource with a runway

There’s a version of this mistake that goes beyond cash. Founders run out of other things before they run out of money, and nobody tracks those curves.

Team capacity is one. You can have two years of cash and still destroy your company by burning out your first ten employees. Key hires who leave mid-product cycle can set you back further than a bad fundraising environment. Customer patience is another. An enterprise customer running a pilot will give you a defined evaluation window, and when it closes, the opportunity closes with it whether or not you have money in the bank. One key customer dependency can distort your understanding of both your business health and your real timeline.

Founders are usually good at tracking cash because investors make them. Nobody makes them build a model of founder energy or key-employee retention risk, so those runways run out without warning.

The counterargument

Some advisors argue that over-modeling early-stage companies is a waste of time. Plans change, forecasts are wrong, and a founder who spends a week perfecting a twelve-month burn model is a founder who isn’t talking to customers. There’s something to this. The graveyard of startups is full of companies with beautiful spreadsheets.

But that argument conflates precision with usefulness. Nobody is asking for a forecast accurate to the dollar. The goal is to understand the shape of your situation: is your real runway fourteen months or eight? That distinction is not a rounding error. It determines whether you run a process with leverage or a process in desperation. Rough but realistic projections, built from actual headcount plans and known contract commitments, take a few hours and are worth the time.

The argument against modeling also ignores who gets hurt by the mistake. It’s rarely the investors, who see enough deals to develop intuition about these things. It’s the founder who raises a round at a bad valuation, or the employees who get laid off in a cost-cutting scramble, or the customers who get left holding a product the company can no longer support.

What to do instead

Build a simple, updatable model that projects your cash balance monthly, based on your actual hiring plan and known expense commitments. Update it when something material changes. Present it to your board as a curve, not a number. Subtract your expected fundraising timeline before you treat any of it as free time.

None of this requires a finance degree. It requires honesty about the assumptions baked into the number you’ve been using. The founder with eighteen months of runway who actually had four was not bad at math. He was just comfortable with a number that felt good and didn’t look behind it.

The comfortable number is almost always the wrong one.