Helion Energy raised a large Series E in 2021. Color Health, a genomics startup that had been a pandemic darling, watched its valuation crater when the public health urgency faded. Neither of these is the story I want to tell. The story I want to tell is about what happens to the companies that don’t make the news, the ones sitting in the portfolios of funds that have quietly gone dark.

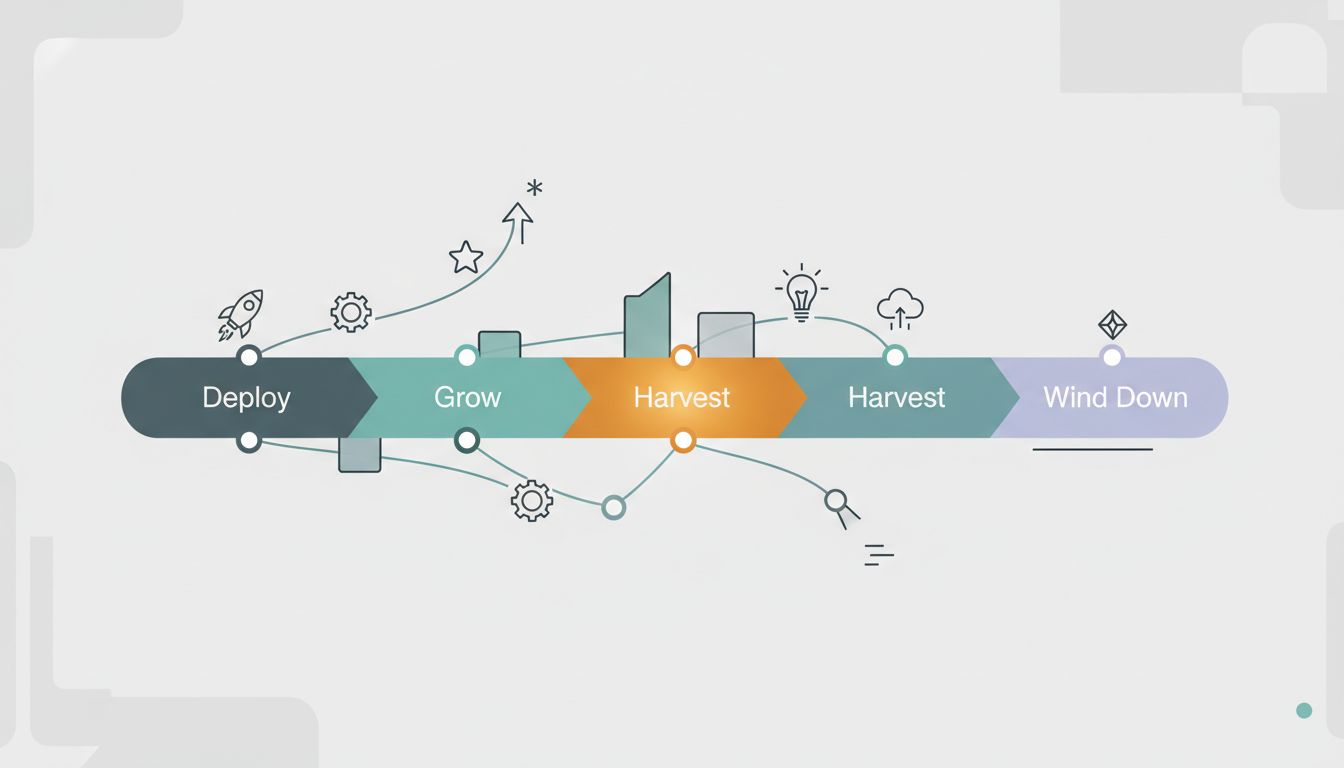

In 2022 and 2023, as interest rates climbed and the IPO window closed, a meaningful number of venture funds stopped writing new checks. Not officially. There were no press releases. Partners continued to take meetings, kept their Twitter presences active, maintained the appearance of normalcy. But inside the funds, the math had changed. Their limited partners were overallocated to private assets after public markets fell and private valuations hadn’t caught up. The so-called denominator effect meant LPs couldn’t commit new capital to follow-on rounds even when they wanted to. Many funds quietly entered what the industry calls “harvest mode,” trying to nurse existing bets toward whatever exit was still possible rather than chasing new deals.

For the companies inside those portfolios, this created a problem that has no clean name and almost no public documentation.

The Setup

Consider a B2B software company, a composite drawn from several real situations that became public through court filings, founder interviews, and secondary market disclosures. Call it a Series B company, two years post-raise, burning through the last eighteen months of runway it thought it had. The lead investor is a mid-sized fund, vintage 2018, that has been sitting on a string of unrealized positions as the market turned. The fund’s tenth year, the year most partnerships begin winding down, is approaching.

The company needs a bridge. Under normal conditions, its lead investor would either write the check or help source a new lead. But the fund is in harvest mode. Writing a new check burns management fee reserves. Finding a new lead means admitting, at least implicitly, that this deal needs rescuing. Both options carry reputational costs inside a partnership already under stress.

So the fund does what funds in this position often do: it delays. Board meetings get shorter. Partners send associates to quarterly reviews. The response time to founder emails stretches from days to weeks. The fund is not abandoning the company, technically. It just isn’t helping.

What Happened

This is where the mechanics get specific and ugly. A venture fund that has stopped deploying capital still controls board seats. It still holds preferred shares with full liquidation preferences. It still has pro-rata rights that can complicate new investor conversations, because any serious new investor wants to know whether the existing lead will participate, and a lead that won’t participate sends a signal no term sheet wants to carry.

The company in question spent eight months trying to raise a Series C in this environment. Every conversation with new investors eventually hit the same wall: what is your existing lead doing? When the answer was “evaluating options,” sophisticated investors translated that immediately. They walked.

The company ultimately had two choices. It could raise a down round on terms that would devastate the cap table (for a clear accounting of what that actually does to founders and employees, see our breakdown of down round mechanics). Or it could find a strategic acquirer willing to buy the company at a price that made the fund whole while leaving common shareholders with little or nothing.

It chose the acquisition. The fund recovered its capital. The founders received a small earnout tied to a two-year retention clause. The employees’ options were underwater. The acquirer got the team and the technology at a significant discount to what the company would have fetched two years earlier.

From the outside, this looked like an acqui-hire. From the inside, it was a controlled liquidation.

Why It Matters

This pattern is not rare. It is the quiet background hum of the current vintage correction, playing out in hundreds of companies that will never generate a press release or a postmortem. The founders often don’t fully understand what happened. They know the fundraise was hard. They know the fund wasn’t helpful. They rarely understand that the fund’s structural situation made helpfulness economically irrational.

Venture funds have a specific incentive structure that most founders only half-understand at the time of the deal. The fund’s general partners make money in two ways: management fees (typically two percent of committed capital annually) and carried interest (typically twenty percent of profits above a hurdle). When a fund is in harvest mode, management fees are declining or fixed. The only way to generate carry is through exits. A struggling portfolio company that needs more capital is not generating carry. It is consuming time and, potentially, more money that could lower the fund’s overall return.

The rational move, from a pure fund economics perspective, is to minimize additional capital deployment into companies that look like they’re heading toward a mediocre outcome, and preserve dry powder (if any remains) for companies that might still be breakouts. The company you’re holding that needs a bridge is not competing against other opportunities in the market. It’s competing against all the other positions in that fund’s portfolio.

This is why the timing of your funding round relative to your investor’s fund lifecycle matters more than most pitch deck advice acknowledges. A fund in year eight or nine has fundamentally different incentives than a fund in year two or three.

What We Can Learn

The lessons here operate at two levels.

For founders currently in or approaching a fundraise, the fund’s vintage year deserves the same diligence as the partner’s track record. A fund raised in 2016 or 2017 is, in most cases, past its active investment period. A fund raised in 2021 is sitting on a portfolio marked at peak valuations and may be in no position to lead follow-ons. Neither is a death sentence, but both change the nature of the relationship you’re entering. Ask directly: what is your reserve strategy for this fund? How many follow-on rounds do you expect to lead this year? A specific, confident answer is a good sign. Vagueness is informative in a different direction.

For the broader industry, the silent-fund problem reveals a structural gap in how venture relationships are documented and governed. Founders sign term sheets and shareholder agreements that give investors significant control rights. Those agreements rarely include provisions for what happens when an investor becomes passive. The board seat remains. The blocking rights remain. The preferential economics remain. The active support, the introductions, the follow-on capital, the partner who champions you in the partnership meeting, all of that is purely discretionary, and nothing in the legal structure protects you when it disappears.

The company in this story survived, in the narrow sense that it didn’t file for bankruptcy. Its technology is being used inside a larger organization. Its team is still employed. By some measures, this is a fine outcome.

But the founders built something worth more than what they received for it, and the gap between those two numbers wasn’t created by the market or by their product decisions or by bad timing. It was created by a misalignment that was baked into the deal structure years earlier, invisible until the fund went quiet and there was nothing left to do but negotiate the terms of the exit.