The Separation Was Designed In

When Salesforce crossed $10 billion in annual revenue, the engineers who built its core CRM architecture had long since moved on, cashed out modest equity packages, or were still collecting salaries with no meaningful upside from the growth they made possible. This is not a Salesforce-specific story. It is the standard outcome for engineers across the industry, and it is not an accident.

The conventional explanation is that capital takes the risk and therefore deserves the reward. Investors write checks before revenue exists; engineers join after the risk is partially de-risked. There is something to this, but it does not hold up as a full explanation. Senior engineers hired into pre-product companies frequently work for below-market salaries precisely because they are accepting risk. The risk argument is selectively applied.

The more accurate explanation is structural. The tech industry has developed compensation systems that decouple the act of building from the act of owning, and those systems persist because the people who design them are not engineers.

Salary Is a Buy-Out, Not a Share

When a company pays an engineer $180,000 a year, it is not rewarding value created. It is purchasing the right to own the value created. The salary is a buy-out clause, not a participation agreement. The engineer receives a known, stable payment. The company receives an unknown, potentially enormous return on whatever gets built.

Equity is supposed to correct for this, and sometimes it does. Early engineers at Google, Facebook, and Stripe became wealthy because they joined early enough, received enough shares, and those companies grew large enough. But this specific combination is rare. Most engineers who receive equity get options with strike prices set near the current 409A valuation, four-year vesting schedules, and 90-day exercise windows that expire when they leave. The majority of options issued across the industry expire unexercised, either because the company fails, because the engineer cannot afford to exercise and hold, or because they leave before vesting is complete.

The structure favors people who can hold concentrated, illiquid positions for years without financial pressure. That describes investors and senior executives far more than it describes the median engineer.

The Leverage Question Nobody Asks

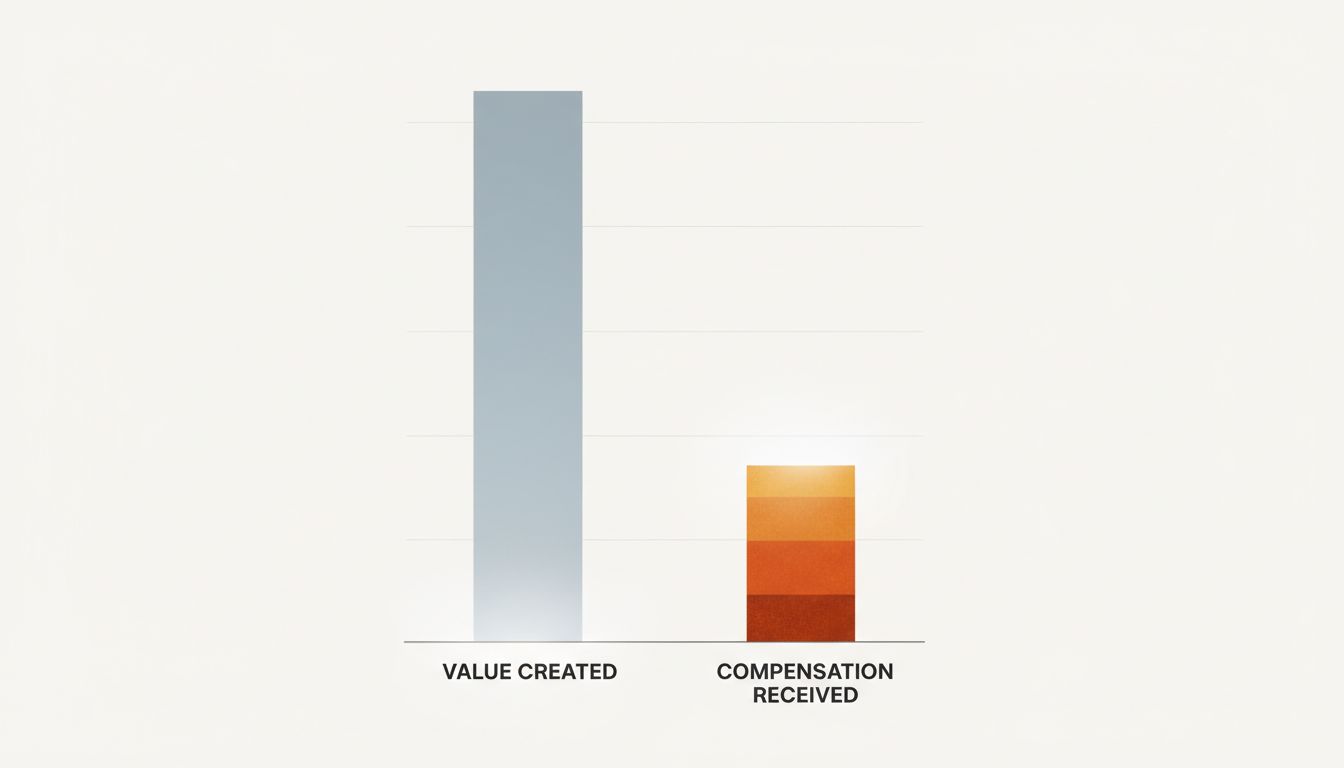

The economic question worth asking is not “how much does an engineer get paid?” but “what is the ratio between the value an engineer creates and the compensation they receive?”

In manufacturing, this ratio is constrained by physics. A machinist can produce only so many parts per hour. The leverage is linear. In software, the ratio has no natural ceiling. An engineer who writes a payment processing library used by ten thousand companies creates value that compounds indefinitely at zero marginal cost to them personally. The same engineer earns a salary that is uncorrelated with that compounding.

This is why tech compensation looks generous compared to other industries but conservative compared to the value being extracted. A $250,000 total compensation package sounds like a lot until you consider that the engineer might be maintaining infrastructure that processes $2 billion in transactions annually. The ratio is what matters, and the ratio is almost never discussed openly.

The executives who negotiate compensation packages understand this arithmetic very well. That is not cynicism; it is just accurate. Boards set compensation with explicit reference to the value employees could extract elsewhere, not the value they create internally. The external labor market sets a ceiling on what engineers must be paid to retain them. It says nothing about what they should receive given their actual contribution.

Why Profit-Sharing Stays Rare

Given this gap, why don’t more companies offer direct profit-sharing to engineers?

Some do, nominally. Bonuses tied to company performance exist at many firms. But these are typically a small percentage of salary, capped, and disconnected from the specific products an engineer built. A backend engineer who spent three years building a recommendation engine that now drives 30 percent of revenue gets the same bonus pool percentage as the engineer who maintained internal tooling.

The deeper reason profit-sharing stays rare is that it would require companies to expose their actual unit economics to employees. To pay engineers a genuine share of the value they create, companies would need to attribute revenue to specific systems and specific teams. Most companies do not have clean enough accounting to do this, and many that do prefer not to. If engineers at a SaaS company knew that their product generated $40,000 in gross profit per customer and the company had 50,000 customers, the salary conversation would look different. What a $50M Series B Actually Buys You is public knowledge compared to what it actually costs to build the product those dollars supposedly funded.

What Changes the Equation

Three things have meaningfully shifted the ratio for individual engineers, and none of them depend on companies becoming more generous.

The first is leverage through tools. A single engineer with modern infrastructure can build and operate software that reaches millions of users. When one person captures all the upside of a profitable product they built alone, the compensation structure becomes irrelevant. This is the actual promise of the indie developer model, not independence in some abstract sense but a direct line between creation and ownership.

The second is negotiating equity more aggressively at the point of hire. Most engineers accept standard option packages without understanding the terms. Strike price, cliff, acceleration on acquisition, and the 90-day exercise window are all negotiable at companies that want specific talent badly enough. The leverage exists; it is rarely used because most engineers are not trained to treat employment as a financial transaction.

The third is collective information. When engineers share salary and equity data, the information asymmetry that companies rely on to keep compensation below market erodes. This is why Levels.fyi changed the negotiating dynamic in ways that years of advice columns had not. Transparency is the only mechanism that exerts sustained pressure on the structural gap.

The gap between building profitable products and sharing in their profits is not a feature of capitalism broadly. It is a feature of specific compensation structures that serve specific interests. Understanding that is the precondition for changing it.