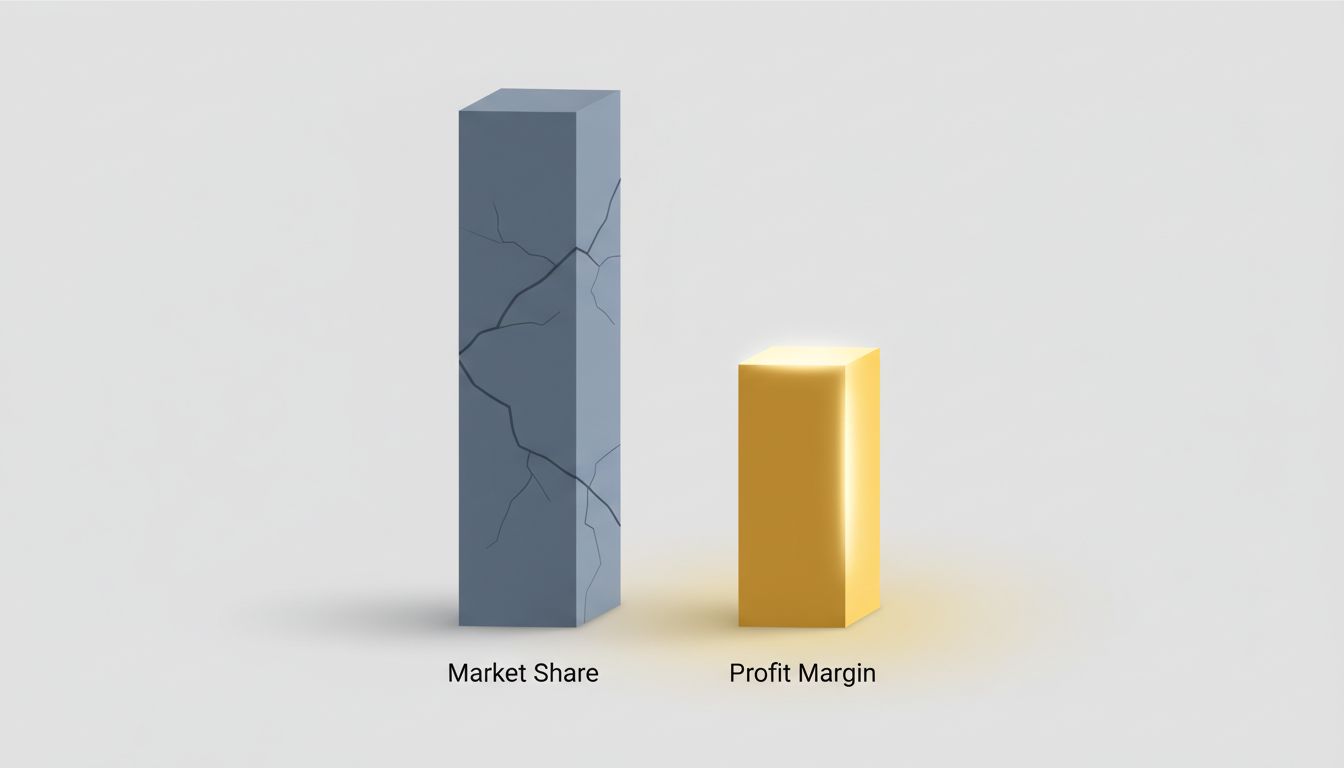

The company with the largest market share is usually the least interesting investment in the room. That sounds wrong until you look at the numbers, and then it’s obvious.

Market leadership is a trap dressed up as a trophy. The product that sits just behind the leader — close enough to credibly compete, far enough from the top to avoid the obligations of dominance — almost always generates better margins, more focused customers, and a more defensible long-run position. This is not an accident. It follows directly from the structural economics of competitive markets.

The cost of the crown

Being number one in a market carries real, underappreciated costs. The leader must defend every segment, serve every customer type, and respond to every competitive threat, because losing any piece of the market looks like decline. That obligation is expensive. It means maintaining broader product lines, larger support organizations, more enterprise sales capacity, and more aggressive pricing in contested segments to protect volume.

Intel spent years subsidizing loss-leader chip lines to hold market share against AMD. The result was that AMD spent a decade losing, then became more profitable than Intel — not by winning the crown outright, but by optimizing ruthlessly for the customers and segments where it had genuine structural advantage.

The leader’s cost structure balloons to match its ambitions. The number two player gets to be selective.

The pricing paradox

Customers use the market leader as a reference point. That sounds like an advantage for the leader, until you think about what it actually means: the leader sets the ceiling on what customers expect to pay.

The runner-up, by contrast, can price just below the leader to win price-sensitive customers, or price at parity and win on differentiation, or in some markets price above the leader by successfully positioning as a premium alternative for a specific use case. Pepsi has run all three strategies at various points. So has AMD versus Intel. So has Bing versus Google, where Microsoft has quietly offered more attractive revenue-share terms to distribution partners precisely because it has less to protect.

The leader cannot easily do any of this without signaling weakness or cannibalizing itself. The number two player has strategic optionality the leader gave up the day it got to the top.

Customers who choose you actually want you

This is underrated. When someone buys the market leader, they often do so by default: it’s what the IT department approved, it’s what their last employer used, it’s the safe choice when no one gets fired for it. The customer relationship is built on inertia, not preference.

The customer who deliberately chose the second product made an active decision. They evaluated both options and picked yours. That customer is less price-sensitive, more engaged with your roadmap, and more likely to advocate internally for expansion. Churn rates for deliberate choosers are structurally lower than churn rates for default buyers.

This is one reason Salesforce grew faster in CRM than the incumbents it displaced: the customers who switched to it genuinely wanted it. The same pattern repeated when Slack took enterprise messaging share from older collaboration tools. The companies that almost ran Slack off the rails were often the wrong customers acquired too fast, not the deliberate early adopters who made the product.

R&D leverage works differently at number two

The market leader has to invest in R&D to defend the entire frontier. The runner-up gets to study what the leader builds, watch what customers actually adopt, and focus its own R&D on the narrower set of capabilities that move the needle. That’s not copying. It’s intelligent resource allocation.

Google watched Microsoft build Windows and Office for years before entering adjacent markets with focused products. Apple watched the MP3 player market develop before entering with a product designed around a specific user experience rather than a feature checklist. In each case, the challenger entered with sharper focus and, at least initially, better unit economics than the incumbent defended with.

The counterargument

The obvious objection is that this breaks down in winner-take-all markets, where network effects are strong enough that number two eventually collapses into irrelevance. Search advertising, social networking, and certain platform markets look like this. Google’s share in search isn’t just large; it’s structurally self-reinforcing in ways that make meaningful competition nearly impossible.

This is real. The argument for runner-up profitability applies most cleanly to markets with genuine product differentiation, where the leader’s advantage is execution rather than network lock-in. In markets where the network is the product, the structural dynamics are different enough that the framework doesn’t hold.

But those markets are fewer than they appear. Most tech markets, including cloud infrastructure, enterprise software, hardware, and developer tools, are competitive on product merit in ways that make number two a legitimately attractive position.

The strategic takeaway

If you’re building a company, the goal should not be to become the market leader as fast as possible. The goal should be to find the customer segment where you have genuine advantage and generate strong economics from that position. Sometimes that leads to market leadership. Often the smarter outcome is a durable, profitable number two position with better margins than the company above you.

The obsession with market share as a proxy for success is a legacy of industrial-era thinking, where scale advantages were so large that share really did translate to profit. In markets with lower marginal costs and faster product cycles, that relationship is much weaker. The runner-up who knows exactly who their customer is and why that customer chose them is in a stronger position than a leader defending a share number that looks good in press releases and terrible in the operating income line.