In 2004, Firefox had maybe 5% of the browser market. Internet Explorer had close to 90%. Microsoft was winning by every conventional measure. A decade later, Firefox had generated hundreds of millions of dollars in revenue through its Google search deal, while Microsoft was actively paying to keep people from abandoning IE. The market leader was spending money to defend market share. The challenger was collecting rent.

This isn’t a quirk. It’s a pattern that shows up across software, hardware, and platforms, and it has a logic to it that most startup founders either don’t know or choose to ignore.

The Pioneer Bears the Cost, the Challenger Collects the Lesson

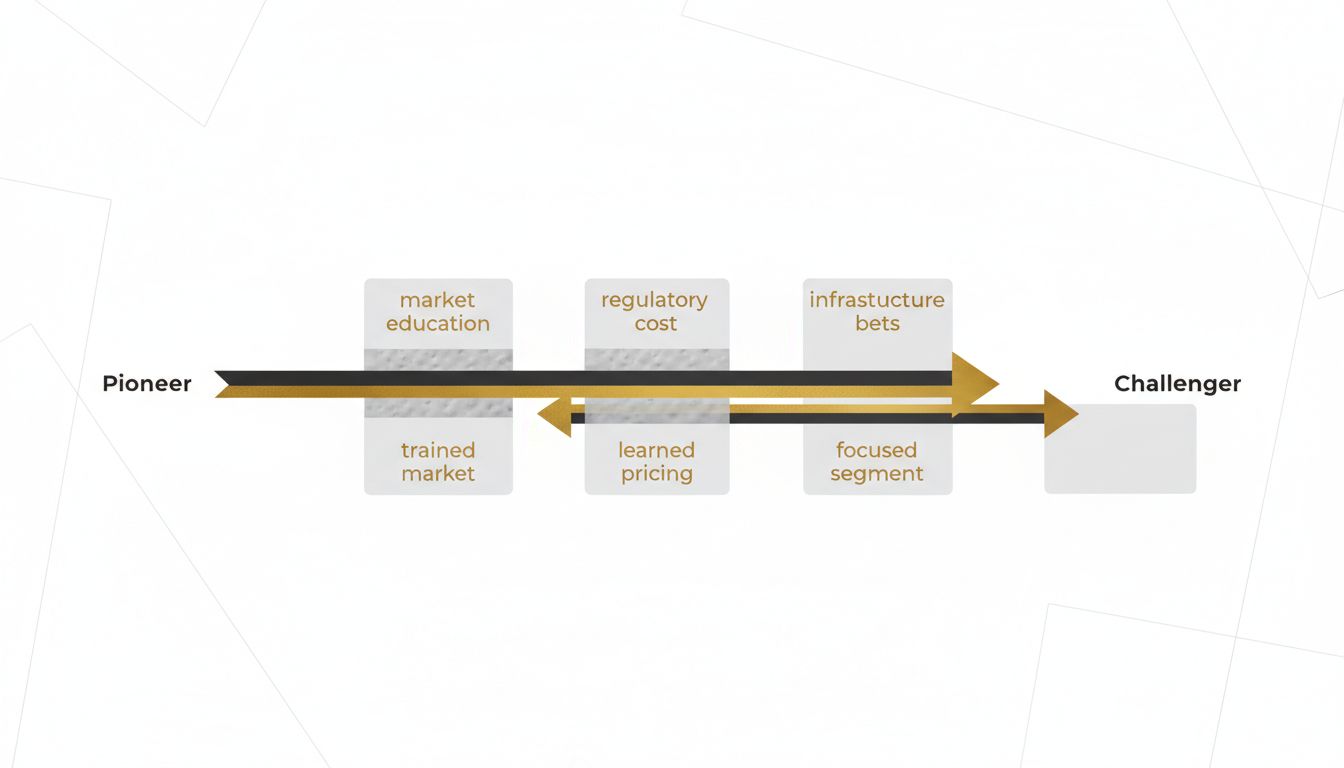

Building a market from scratch is expensive in ways that don’t show up cleanly on a balance sheet. The first entrant has to educate customers, absorb early product failures, make infrastructure bets before anyone knows which infrastructure will win, and staff up for a category that doesn’t have an established talent pool yet. These costs are real even when they’re invisible.

The second-place company gets to watch. They see which customer segments actually pay, which features drive retention, which distribution channels convert. They inherit a trained market. By the time they arrive, customers know what the product category is, have opinions about what’s missing, and are often actively looking for an alternative. That’s not a hard sales environment. That’s a gift.

This is why challengers so frequently have better unit economics than leaders. They skipped the expensive curriculum.

The Burden of Being Number One

Market leadership comes with obligations that erode margins. The leader has to maintain the broadest possible product to serve the broadest possible customer base. They carry legacy customers who can’t be moved off old versions. They’re the ones who get hauled in front of regulators when the category attracts scrutiny. Their engineers get poached by anyone who wants to credibly claim category expertise.

The challenger gets to be focused. They can serve one customer profile extremely well instead of five customer profiles adequately. They can make pricing decisions based on their own economics instead of having to signal dominance. They can move faster precisely because they have less to protect.

Salesforce didn’t invent CRM. Siebel built that market, built the enterprise relationships, and trained a generation of sales teams on why CRM mattered. Salesforce arrived when the case was already made and sold a better-priced, easier-to-deploy version to companies that were already sold on the category. Oracle and SAP’s investments in building enterprise software credibility did as much for Salesforce’s sales cycle as anything Salesforce itself did.

Profitability vs. Revenue Is the Wrong Frame

Here’s where people usually get confused: being second doesn’t mean having less revenue. It means having different revenue with better margins and fewer structural obligations.

Visa processes more transaction volume than Mastercard. But for long stretches, Mastercard has run higher margins. The reason is straightforward: Visa, as the larger network, absorbs more of the cost of maintaining the network’s credibility, handling disputes with large issuers, and managing regulatory relationships globally. Mastercard free-rides on some of that infrastructure while staying nimble enough to win in specific verticals and geographies.

The same dynamic plays out in cloud. AWS built the market. Azure arrived late and immediately had a sales advantage because enterprise IT departments already had Microsoft contracts and the Microsoft relationship to leverage. Amazon did the hard work of convincing Fortune 500 companies that putting workloads in the cloud wasn’t insane. Microsoft collected the benefit when those same companies went looking for a second vendor.

This has direct implications for how you think about pricing strategy. Challengers often price at or slightly above the market leader and still win on value perception, because they can afford to invest in the experience in ways the leader, spread across more customers and more product surface area, cannot.

When Second Place Becomes a Sustainable Position

The obvious risk is that second place is a waystation, not a destination. For many companies it is. But the ones that make it a sustainable position share a few characteristics.

They’re second place in the overall category but first place in a specific segment. Bing will never beat Google on search volume, but there are specific contexts (older demographic, Windows-integrated workflows, certain enterprise search applications) where Microsoft’s position is genuinely defensible. Being second globally while being first somewhere specific is a coherent business.

They accept the ceiling. This is the counterintuitive part. The companies that make second place profitable are often the ones that have explicitly decided not to try to become first. That decision eliminates an enormous amount of expensive behavior: the unnecessary product expansion, the land-grab acquisitions, the marketing spend designed to shift category perception rather than convert known buyers. When you stop trying to win the category, you can focus on making money in it.

They build switching costs that don’t depend on being the biggest. Interoperability with the leader’s format, better customer service, lower implementation costs, stronger vertical-specific features. These create stickiness that’s independent of overall market share.

What This Means If You’re Building Something

If you’re three years into building a product in an established category and someone is ahead of you, the instinct is to treat that as a problem to be solved. Sprint harder, raise more, hire faster, try to flip the standings.

Sometimes that’s right. But often it isn’t, and the companies that figure that out early are the ones that stop burning cash on category dominance and start building the kind of focused, high-margin business that the market leader can’t easily replicate. The leader has constituencies to serve. You don’t.

The startup mythology says you have to be the biggest to matter. The actual economics of software businesses say something more complicated: the company that arrives second, learns from the leader’s mistakes, and builds for profitability rather than dominance often ends up being the better business to own. It just makes for a less compelling origin story.

That’s probably why you don’t hear it talked about more.