In 2011, a payments startup called Stripe was processing transactions for a few hundred developers. That was it. No enterprise sales team, no geographic expansion, no push to grab market share from PayPal. Patrick Collison was personally emailing developers to ask what was broken. The company had been incorporated for two years and had barely grown its customer base beyond a tight circle of technical founders who’d found the product through word of mouth.

Anybody watching from the outside would have said Stripe was moving too slowly. Anybody watching from the inside knew they were doing something rare: they were learning faster than they were growing.

The Setup

The conventional wisdom in startup circles is that speed wins. Move fast, capture market share, outrun your competitors, worry about efficiency later. This logic has some truth to it in winner-take-all markets. But it has produced a generation of founders who confuse motion with progress, and who scale their problems before they’ve solved them.

Stripe’s early restraint wasn’t timidity. It was deliberate. The Collisons understood that payments infrastructure is a trust product. If you get it wrong at scale, you don’t get a second chance. So they spent years getting it right at small scale first. They interviewed developers obsessively. They read every support ticket. They treated the customers who complained as their most valuable resource. By the time Stripe opened up broadly and started expanding internationally, they had something that almost no fast-scaling startup has: a product that actually worked the way users expected, and a support system that knew where the bodies were buried.

The result was a company that, once it did start scaling, scaled with unusual efficiency. Less churn, fewer catastrophic incidents, a reputation that compounded. Today Stripe processes hundreds of billions of dollars annually and is worth more than nearly every competitor that tried to outrun it in the early years.

What Actually Happened

The Stripe story is not unique. It’s a pattern.

Craigslist ran as a side project inside Craig Newmark’s company for years before it became its own entity. It stayed in San Francisco for a long time. It didn’t try to be everywhere at once. It got the San Francisco market right, and then it moved. That tight geographic focus was treated as a limitation at the time. It turned out to be a forcing function for figuring out what the product actually needed to be before multiplying it across cities.

Mailchimp refused venture capital for years and grew slowly inside its core market of small businesses. Founders Ben Chestnut and Dan Kurzius were running a web design shop when they built the email tool as a side product. They kept it small on purpose, kept prices low, and spent years figuring out what small business owners actually needed from email marketing before they tried to serve everyone. By the time they did scale, the product-market fit was load-bearing. They eventually sold to Intuit for $12 billion.

The counterexamples are just as instructive. Homejoy raised significant venture funding and expanded to 35 cities in under two years. The theory was that home cleaning was a massive market and first-mover advantage would matter. The practice was that they scaled before they’d figured out worker classification, quality control, or unit economics. They shut down in 2015. The speed didn’t save them. It finished them.

Why This Pattern Exists

There’s a mechanical reason why slow early growth often produces faster eventual scale. When you’re small, feedback is cheap and changes are cheap. A bug in your onboarding flow affects fifty users and you can fix it in a day. That same bug at fifty thousand users is a revenue problem and a brand problem and a support team nightmare.

Founders who scale too early are essentially betting that they’ve already found the right answers. They’re committing to a particular version of their product, their operations, and their go-to-market before they’ve stress-tested any of it. When the wrong answers get baked into a large organization, they become very hard to change. Deleting a feature is harder than building one. The same is true for processes, pricing structures, and sales motions.

There’s also a capital dynamics argument. Companies that grow slowly without burning cash are not dependent on continued fundraising to survive. That independence gives them time. Time to iterate, time to wait for the market to develop, time to hire without panicking. Mailchimp’s frugality wasn’t a limitation. It was the thing that gave them the runway to figure out what they were building.

What We Can Learn

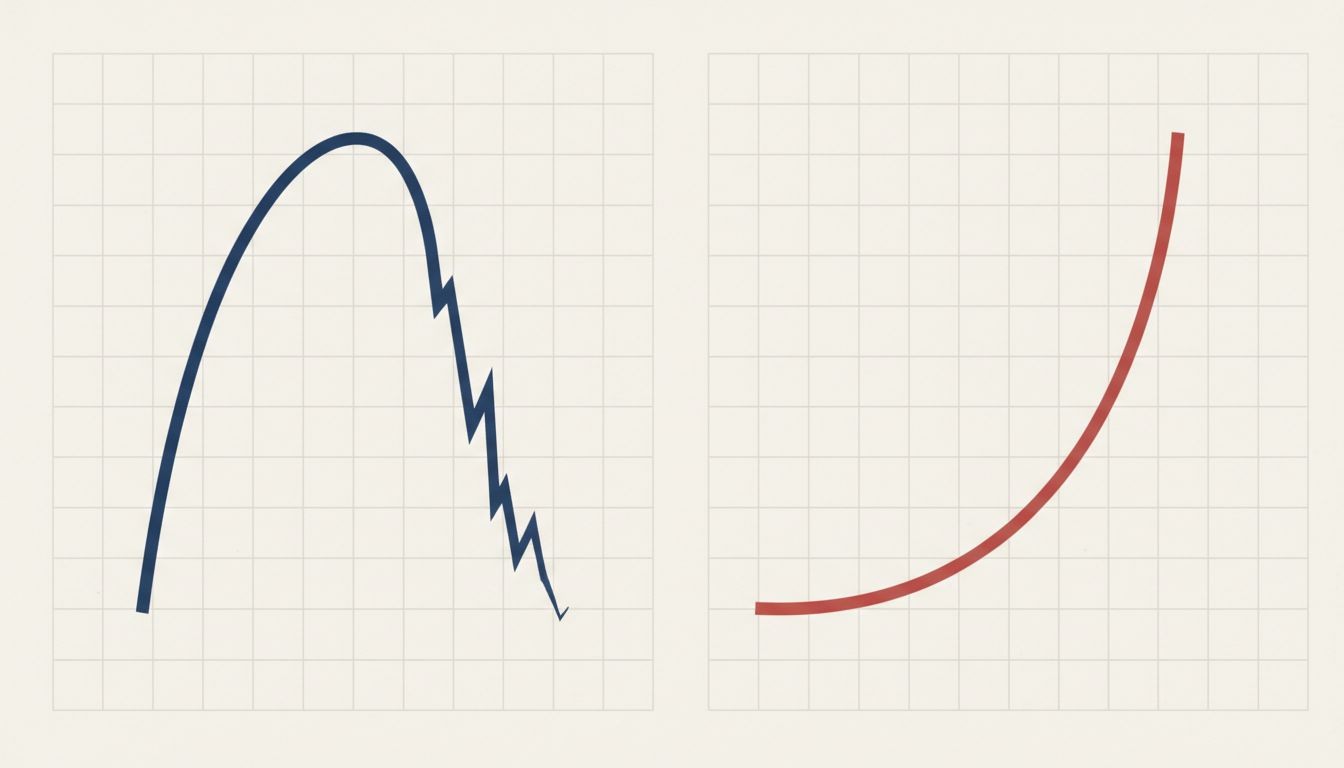

None of this is an argument for moving slowly forever. The companies in this pattern all eventually moved fast. Stripe’s expansion once it hit product-market fit was aggressive. The point is sequencing: get the foundation right before you multiply.

A few things that separate the deliberate restraint of a Stripe from the accidental stagnation of a company that just isn’t growing:

Intentionality about the constraint. The Collisons weren’t slow because they didn’t know how to grow. They were slow because they made a choice to prioritize learning over growth. If you can’t articulate why you’re staying small, you’re probably just stuck.

Obsessive depth in the early market. The benefit of not expanding is that you can go very deep with the customers you have. Stripe knew its early developer users better than those users knew themselves. That depth is what made the product defensible once it did scale.

Clear criteria for when to accelerate. At some point the Collisons decided they’d learned enough and the infrastructure was solid enough to push. That transition was a decision, not a drift. Companies that stay small indefinitely usually haven’t defined what “ready” looks like.

The startup mythology says that the bold bet, the aggressive expansion, the willingness to burn capital for market share, that’s what separates the winners from the also-rans. Sometimes that’s true. But for every Amazon that bet on scale early and won, there are dozens of companies that scaled their way into a hole.

The companies worth studying are the ones that were almost boring in their early years. Methodical, focused, a little difficult to get excited about. And then, once they understood what they were doing, nearly impossible to slow down.

Stripe is worth something like $65 billion today. It took them two years to get out of private beta. Most founders would have panicked by month six.

Patience, when it’s strategic rather than passive, is not the opposite of ambition. It’s how ambition actually compounds.