Tech Economics

The Startup That Beats You Will Charge Less and Profit More

Lower prices, higher margins. It sounds like a contradiction until you understand the structural moves that make it possible.

The business models, market forces, and financial dynamics driving the tech industry.

Lower prices, higher margins. It sounds like a contradiction until you understand the structural moves that make it possible.

Open source software powers most of the internet and costs its users nothing. That's not a charity story. It's a strange economic arrangement worth understanding.

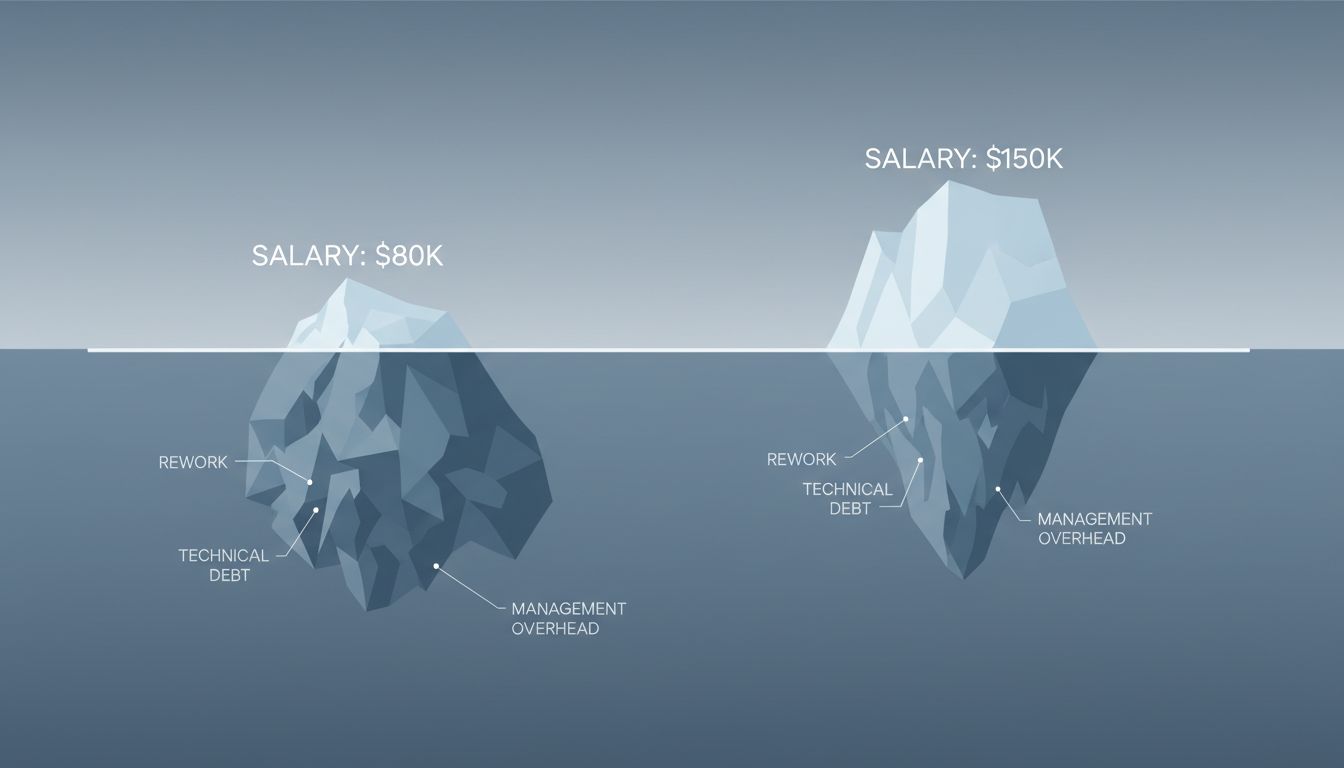

Salary is a cost. Output is a return. Confusing the two is one of the most expensive mistakes a company can make.

Salary is what you pay. Cost is what you get. Most engineering hiring decisions confuse the two, and the math is rarely close.

The products most likely to get axed aren't the failing ones. They're the ones making money but consuming resources a parent company has decided to allocate elsewhere.

Being first sounds like an advantage. Ask Friendster, Myspace, or AltaVista how that worked out.

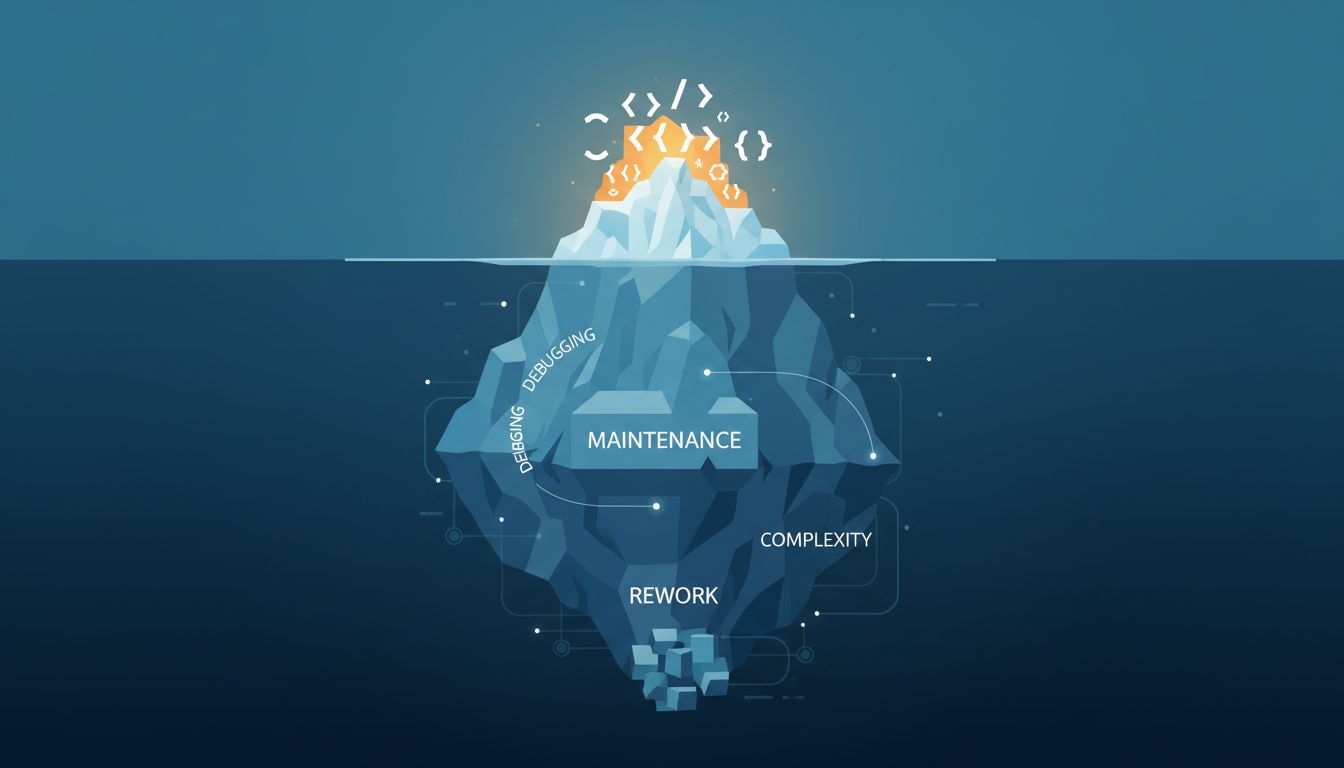

The highest-paid engineers often have the thinnest commit histories. That's not a paradox. It's a signal about what companies actually pay for.

Some SaaS vendors charge higher per-seat rates as headcount rises. It's not a bug in their pricing model. It's the whole point.

Hiring cheap engineers feels financially responsible. It usually isn't. Here's the math most engineering managers refuse to do.

First-mover advantage is one of the most persistent myths in tech. The data and the history both point the other way.

Lines of code is a seductive metric. It's also almost completely backwards as a measure of engineering value.

Winning a tech market sounds great until you see the cost structure. The company in second place is often running a much better business.

Market leadership costs more than it pays. The economics of tech competition reward the company just behind the leader more than the leader itself.

The people who build the products that generate billions rarely capture much of that value. The structure is intentional, not accidental.

The number sounds transformative. The reality is more specific, and more instructive.

Being first is expensive, uncertain, and frequently fatal. The companies that dominate markets are often the ones that watched someone else make all the mistakes.

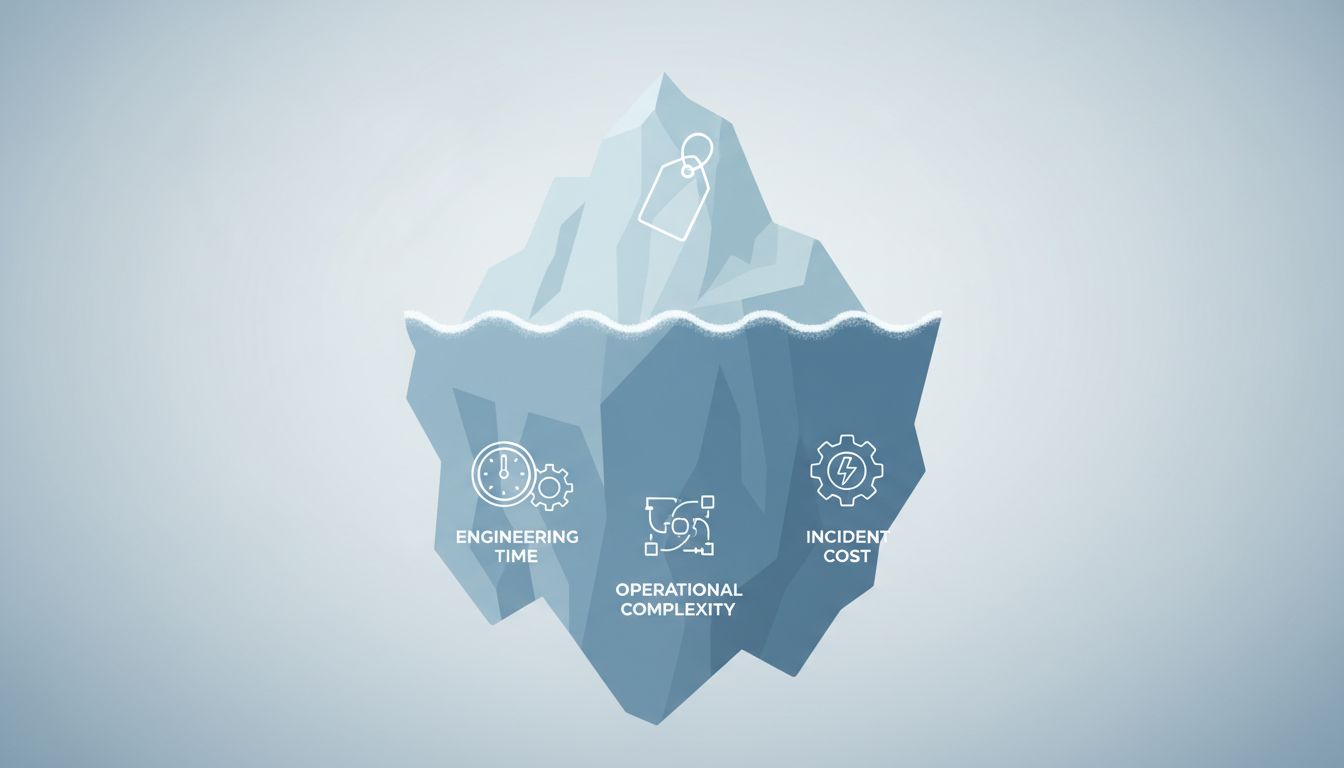

Picking a mid-tier cloud plan to save money often triggers hidden costs that exceed what the premium option would have charged you. Here's why.

The decision process inside venture capital firms looks nothing like founders imagine. Here's what actually happens to your deck.

Join thousands of readers who get our weekly breakdown of the most important stories in technology.

Free forever. Unsubscribe anytime.